With the Omicron variant driving an unprecedented number of new COVID-19 cases in recent weeks, our consultancy team, Ascend by Cirium, has reviewed the industry’s recovery progress so far, and shared its outlook for the year ahead.

Despite the uncertainty around Omicron and its visible effect on European air traffic, Cirium data shows the variant has had little impact on the number of flights scheduled or flown globally.

Recovery on track despite Omicron, but Asia lags behind

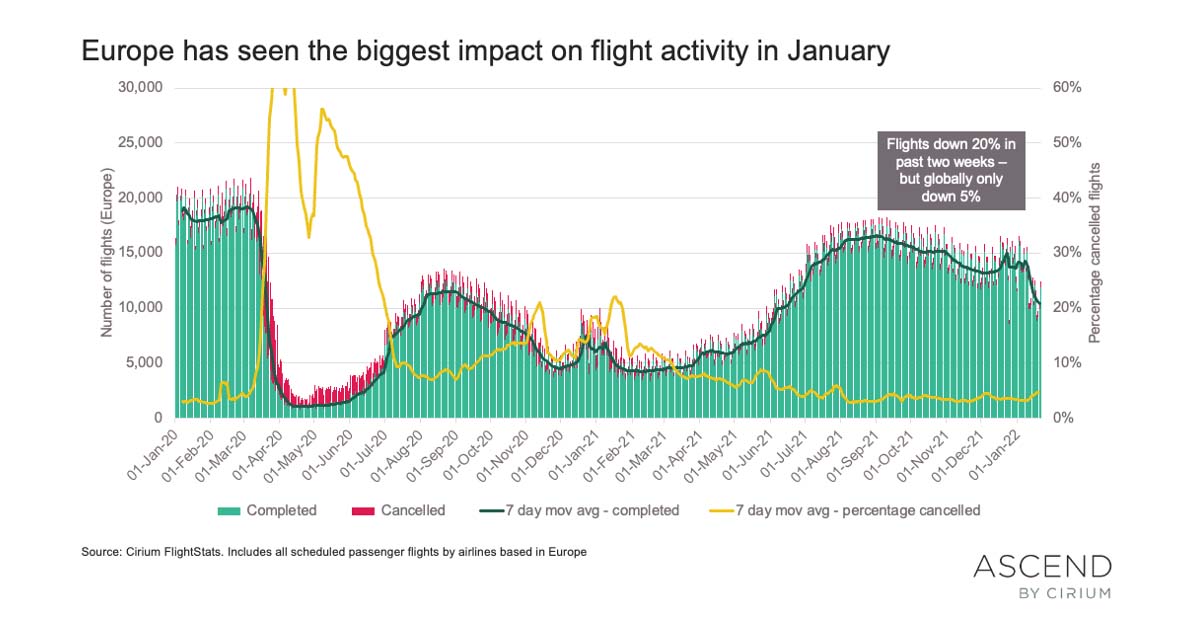

During the recent Cirium Live webinar, What to look out for in 2022, Richard Evans, Senior Consultant at Ascend by Cirium, asserted, ‘European flight activity declined significantly in the second half of January, with flights down by about 20% – but globally, they were only down by 5%.’

As Evans explained, global air traffic is expected to recover to around 15% below pre-pandemic levels by the end of this year, with domestic markets likely to fully recover in 2022.

In fact, some domestic markets have already reached 2019 levels in terms of capacity – and even some of the long-haul markets are less than 25% below their pre-Covid equivalents.

According to Cirium Schedules data, we are expected to see further green shoots in the short term, with total capacity in March 2022 scheduled to be just 24% down on March 2019 figures. However, while most markets are on track for recovery, the Asia-Pacific region remains an outlier.

‘There was a slight uptick in Asian international traffic over the last two months of 2021, as some countries reopened their borders,’ explained Evans. ‘But the Association of Asia Pacific Airlines (AAPA) reports international traffic in 2021 was down 96% overall – so recovery for Asia is still a long way off.’

Most narrowbodies back in the skies

Since September 2021, when Ascend by Cirium revised its baseline recovery scenario, the total in-service narrow-body and wide-body fleet has surpassed the numbers predicted. However, the average utilization of these aircraft is much lower than in pre-pandemic years.

‘Airlines are returning more aircraft to service than we hypothesized, as they are using them less efficiently,’ explained Rob Morris, Ascend by Cirium’s Global Head of Consultancy. ‘This illustrates that airlines are preparing for a very quick return to service. While their fleets might be inefficient right now, this approach will enable them to leverage the demand in the longer term.’

As expected, younger aircraft were among the first to return – with only 5% of the global Airbus A320neo fleet still in storage. Throughout 2021, wide-bodies (particularly the Boeing 777) took the biggest fall, while some previous generation aircraft including the A320ceo also saw further reductions.

‘Newer aircraft are coming back into service more quickly, as they burn less fuel and have lower maintenance costs,’ added Richard Evans. ‘While late-built narrow-bodies are coming back as quickly as possible, a lot of Airbus A330-200s, older Boeing 777-200s, 777-300ERs and other wide-body aircraft types are still parked.’

The panelists also touched on the importance of the cargo market, which has seen significant growth in demand throughout the pandemic.

According to guest speaker Shane Matthews, Head of Strategic and Market Analysis at SMBC Aviation Capital, cargo traffic remains very strong and the demand for dedicated freighter aircraft is through the roof – with many conversions taking place.

‘For cargo, a lot depends on how the long-haul passenger market returns – as there is quite a lot of cargo capacity in the belly-holds of 777s, A350s, etc. Long-haul capacity has only recovered to about 50% of pre-Covid levels, but we do expect to see a big increase this year.’

Boeing to match Airbus on deliveries

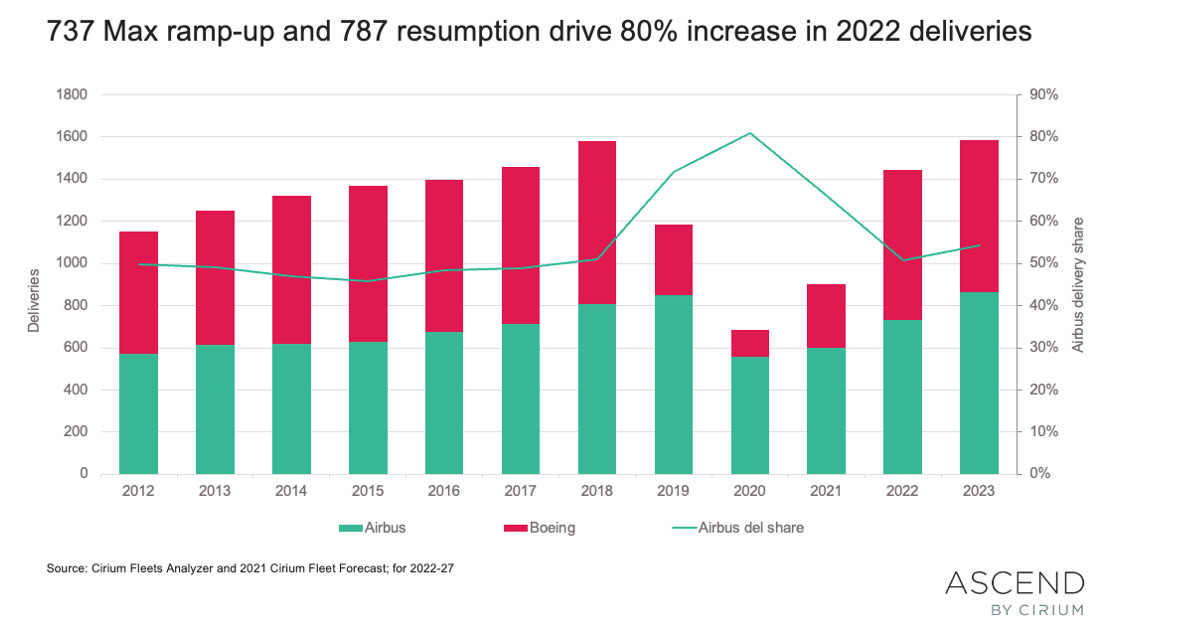

Reflecting on last year’s deliveries, the panelists agreed that 2022 will be the year when Boeing regains the share of aircraft deliveries it has lost to rival, Airbus.

‘Overall, we have seen 2021 improve a little on 2020 numbers. This was mostly driven by Boeing delivering over two hundred 737 MAX aircraft,’ explained Evans. ‘Boeing’s delivery share was significantly down – compared to the 50-50 split with Airbus in pre-Covid years – but we do think we’ll get back to that in 2022.’

This largely depends on whether Boeing is able to hit its targets for the 737 MAX ramp-up and deliver its pre-built inventory. So far, the Boeing 737 MAXs – along with the 787’s resumption – have driven an 80% increase in deliveries in 2022.

Leisure to gain ground over business travel

On the topic of business travel, the panel agreed there is cause for optimism – but airlines must react to the ongoing structural change in international business travel demand.

‘The absolute number of business travellers will return to 2019 levels, but the split between business and leisure will continue to shift towards the latter,’ said George Dimitroff, Ascend by Cirium’s Head of Valuations.

According to Shane Matthews, airlines will react in time to the changing nature of business travel. ‘During the last downturn, First Class essentially ceased to exist, as business travellers could no longer justify it – this led to the rise of Premium Economy. I think airlines will soon start to reposition themselves to better fit where the demand is.’

However, as Dimitroff explained, dedicating a higher share of the cabin to leisure travellers further exposes airlines to seasonality – particularly in Europe, where the intra-European market is heavily characterized by seasonal demand.

Part-outs on hold for lessors

Throughout the pandemic, retirement volumes have been much lower than in previous years. In 2021, only around 300 aircraft retirements were tracked – compared to 480 commercial jets permanently retired in 2019.

‘We can expect to see around 400 single-aisle aircraft parting out annually for the next few years,’ said Rob Morris. ‘These will come from both the parked inventory and from aircraft that are still in service, but are getting to their natural retirement age.’

According to Morris, lessors have been slow to part aircraft out because the demand for engines and used serviceable material (USM) has been relatively low. As utilization increases and more aircraft return to service, Cirium expects to see more demand for USM – and thus more aircraft parted out.

Echoing Morris’ thoughts, Dimitroff added, ‘At the moment, there is not enough money in retiring an aircraft – with the exception of some types which share parts with the cargo version of themselves. We have seen Boeing 747, 757 and 767 product values increase for this reason.’

As Dimitroff explained, for part-outs to become attractive to lessors, the in-service fleet needs to be high, aircraft utilization must increase, and sufficient MRO capacity will need to be ensured.

‘We need to recognize both the real retirements, i.e. the aircraft which are actually dismantled, and the additional “zombie fleet” of aircraft that aren’t being retired because they cannot be monetized – but which are effectively in storage and unserviceable, as lessors don’t want to invest in returning them to service.’