After a period of significant disruption, global travel demand has not only returned but is also setting a new trajectory. Growth is now driven by resilient structural demand, evolving passenger expectations, and ongoing supply-side pressures. For operators, the imperative is clear: data-driven strategies are essential to achieve operational efficiency, enhance future readiness, and improve the passenger journey in a rapidly shifting market.

The Cirium webinar, Future Flight: Shaping Traveler Experiences with Aviation Analytics, explored forces shaping commercial aviation as the industry approaches 2026. Drawing on insights from panelists representing various aviation sectors and the latest aviation data, the session covered the global demand outlook, operational responses to emerging pressures, and the expanding role of aviation analytics in strengthening airport resilience and enhancing the passenger experience.

The global travel outlook: a new trajectory

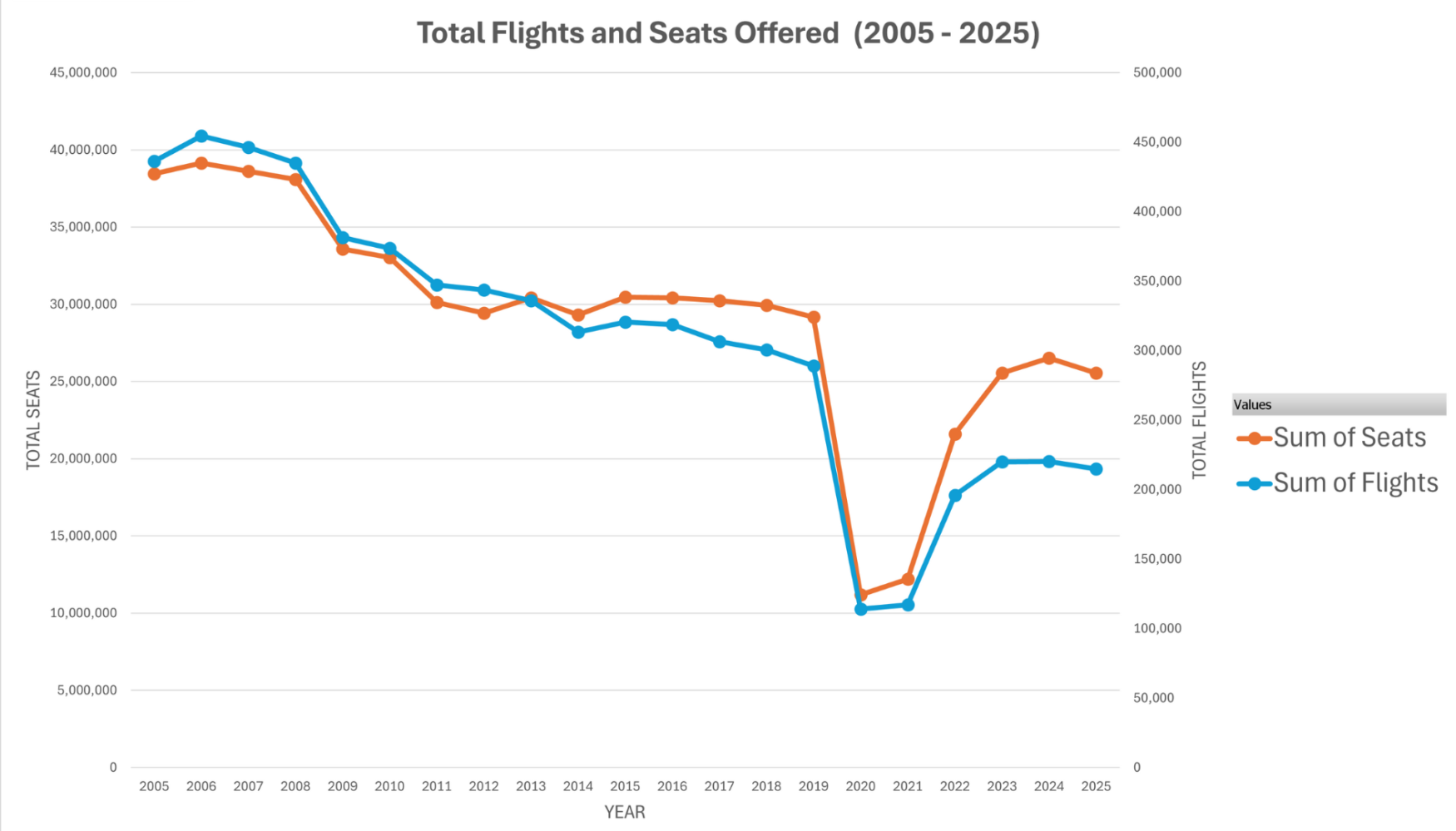

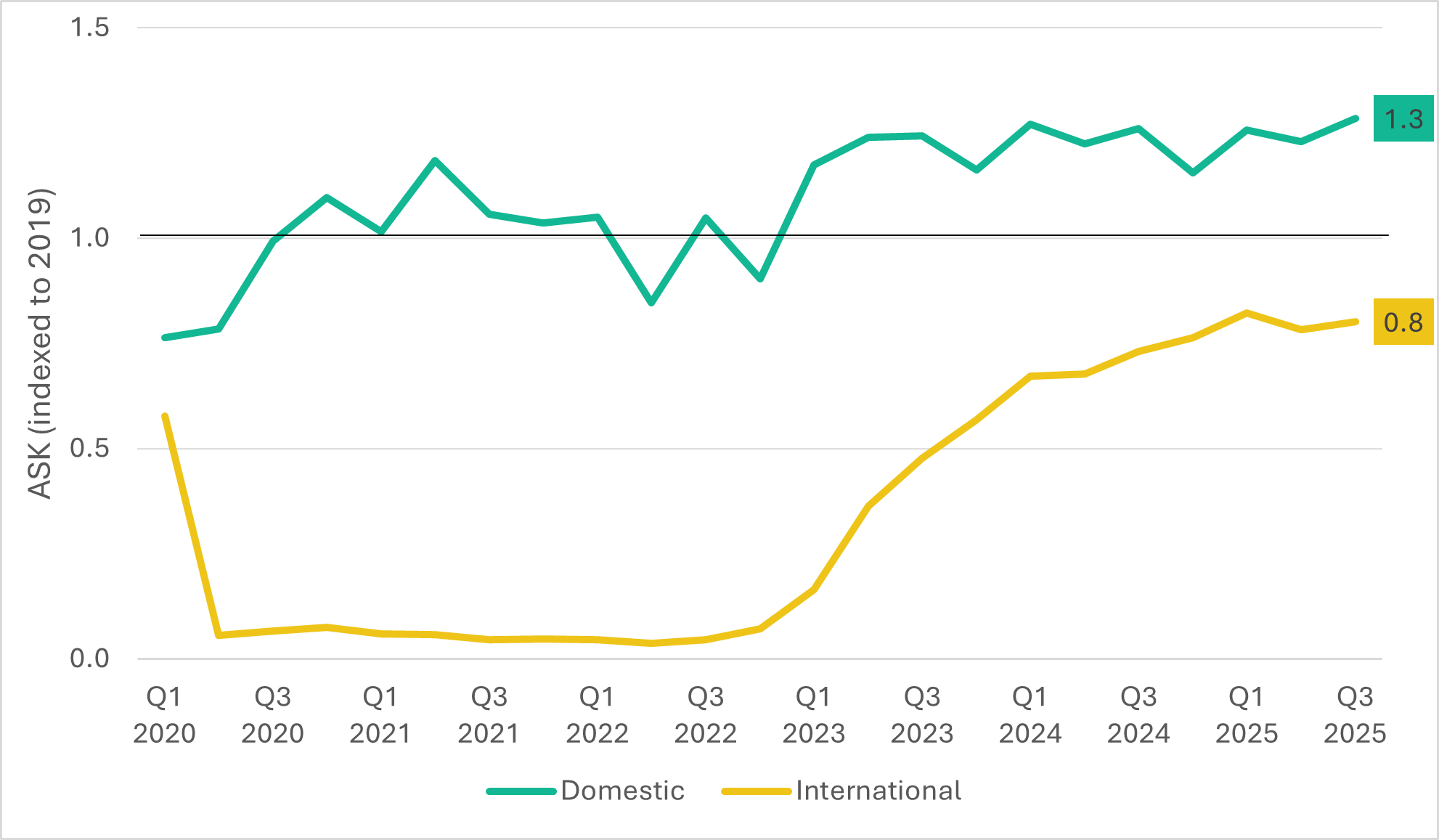

The outlook for global air travel has shifted as the industry moves beyond pandemic recovery. Global revenue passenger-kilometers (RPKs) have surpassed 2019 levels, reflecting strong demand. However, the industry still trails its pre-covid growth trajectory, representing about four years of lost progress.

The rapid growth seen after borders reopened has eased, and demand is being driven by fundamental market forces than by deferred travel. In this climate, commercial aviation is forging a distinctly new path.

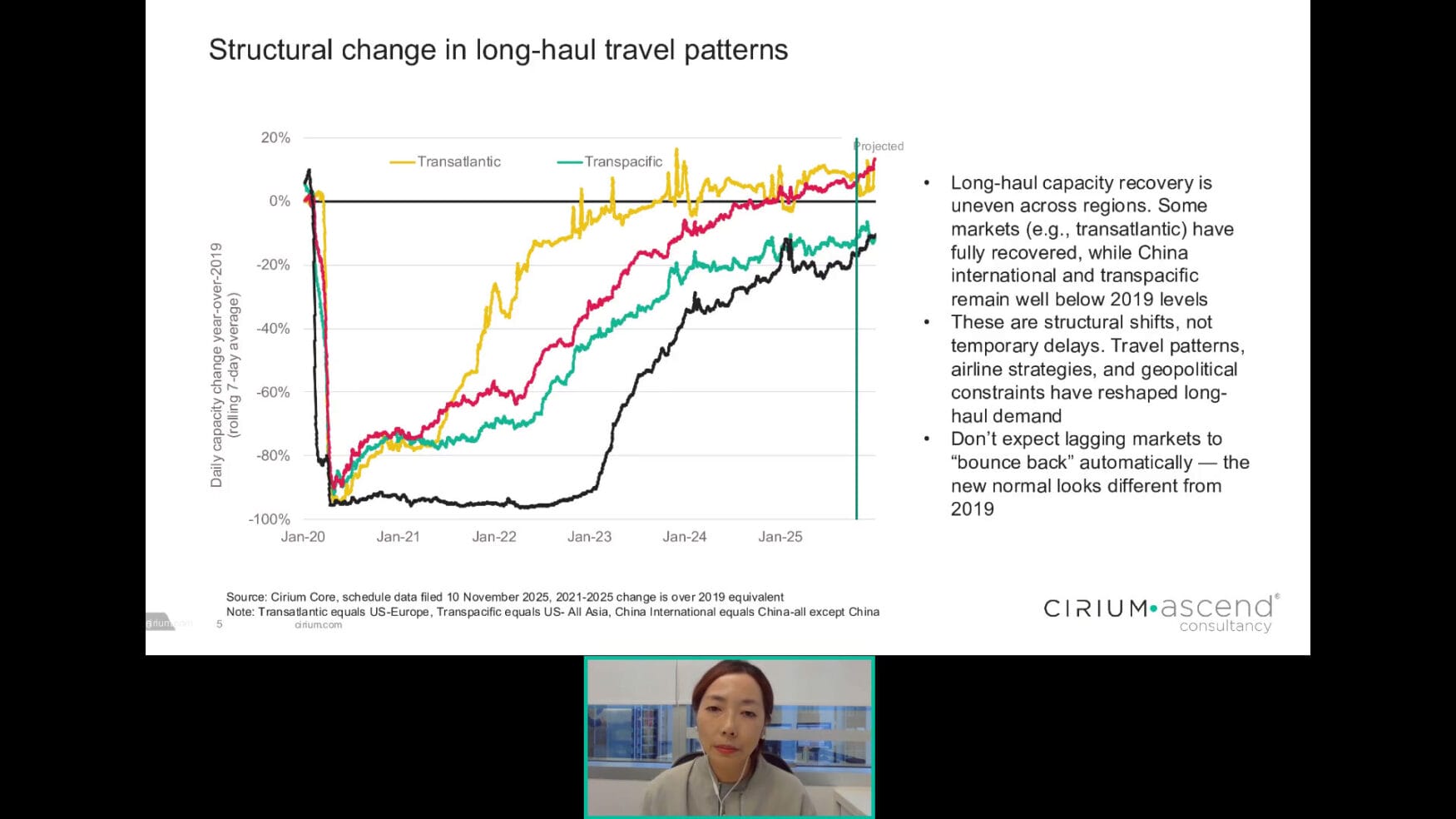

An uneven recovery landscape

Joanna Lu from Cirium Ascend Consultancy presented 2026 Travel Market: Robust demand in a constrained operating environment

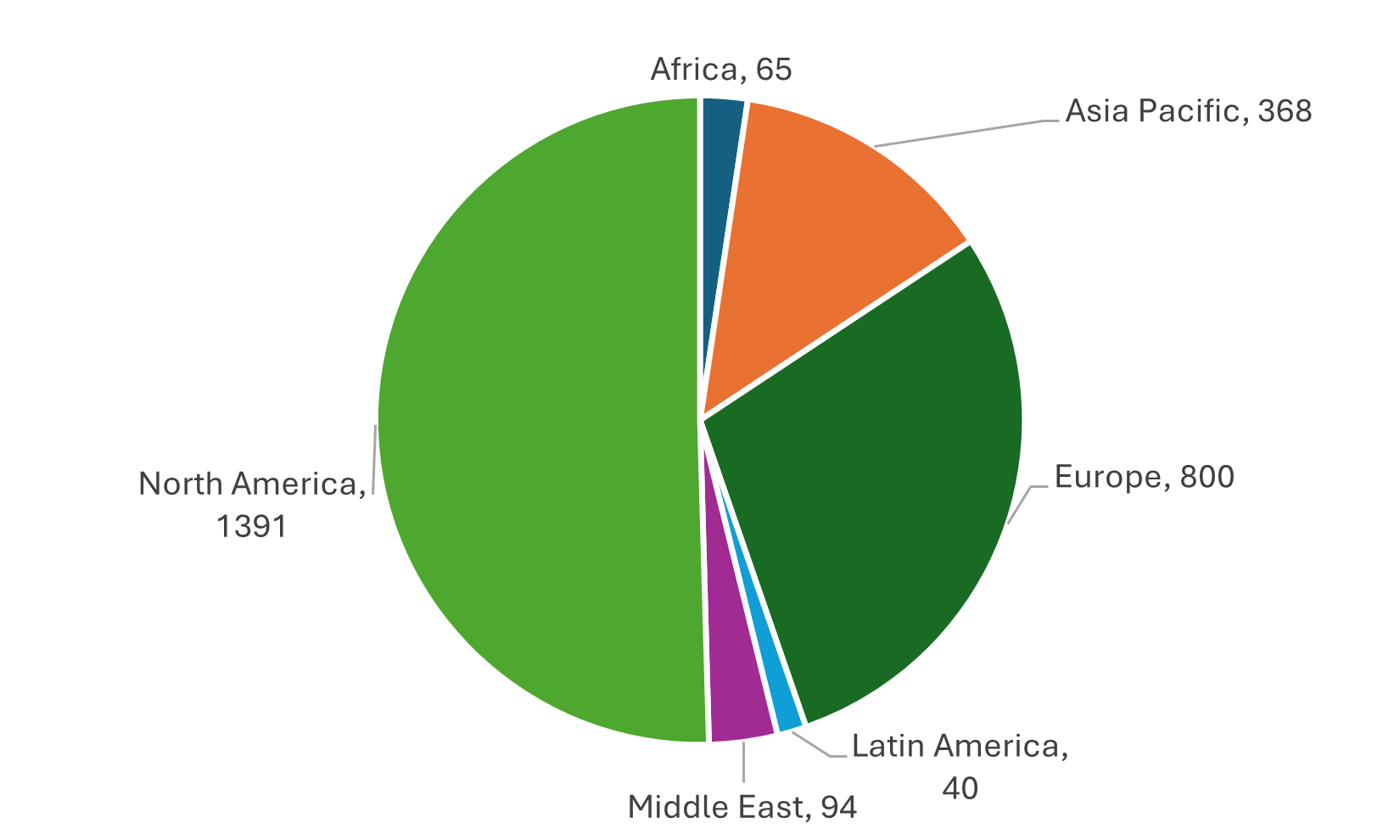

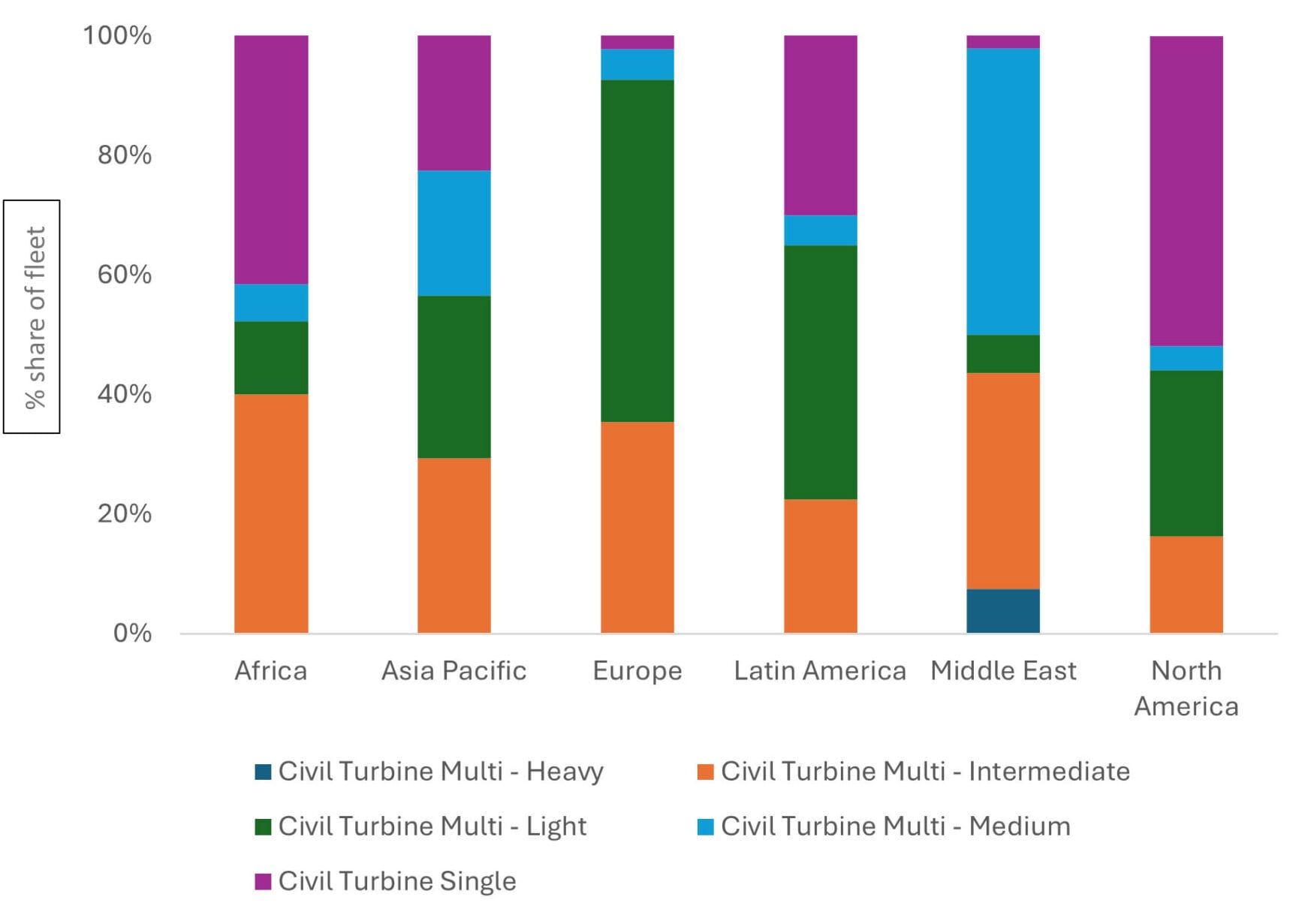

While there is a macro picture of strong growth, the patterns remain uneven between markets.

Capacity on transatlantic and Europe–Asia routes has surpassed pre-pandemic benchmarks, while in contrast, transpacific traffic and China’s international network still lag compared to 2019 levels. This divergence highlights the impact of persistent structural factors, such as strategic fleet deployment, changing traveler behavior, and ongoing geopolitical challenges.

The evolving traveler: new demands and behaviors

Demand drivers are shifting. Surveys consistently highlight a growing emphasis on unique travel experiences, even as inflation acts as a headwind for some travelers. Moreover, flexible and hybrid work patterns continue to blur the line between leisure and business trips, creating more diverse travel profiles and shifting travel seasonality.

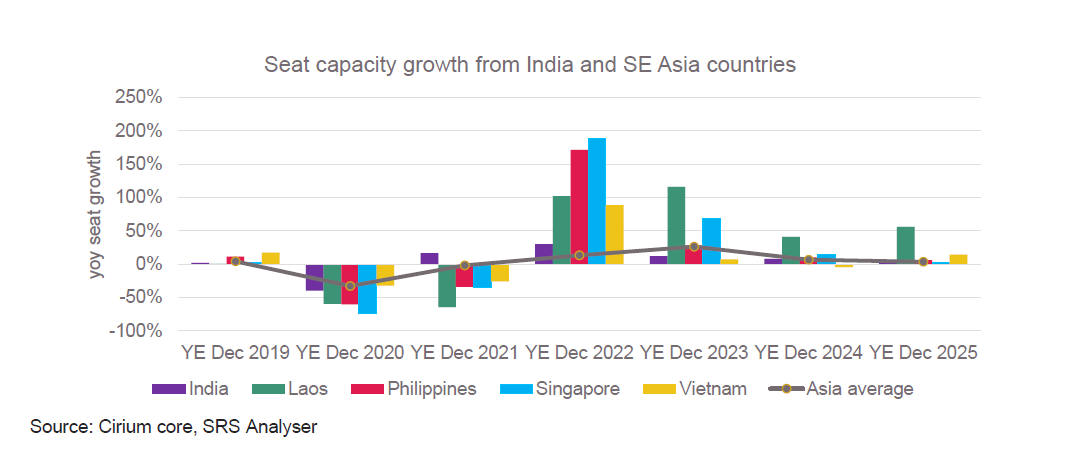

Alongside these behavioral shifts, the rise of Asia’s expanding middle class—particularly in India and Southeast Asia—is fueling demand growth. Visiting Friends and Relatives (VFR) travel remains a key driver, offering a resilient source of underlying traffic as other segments fluctuate. Combined with the ongoing trend toward short-haul regional journeys, these factors are prompting airlines and airports to revisit network structures and tailor their offerings to better match these evolving passenger expectations.

The operational imperative: reliability in an era of growth

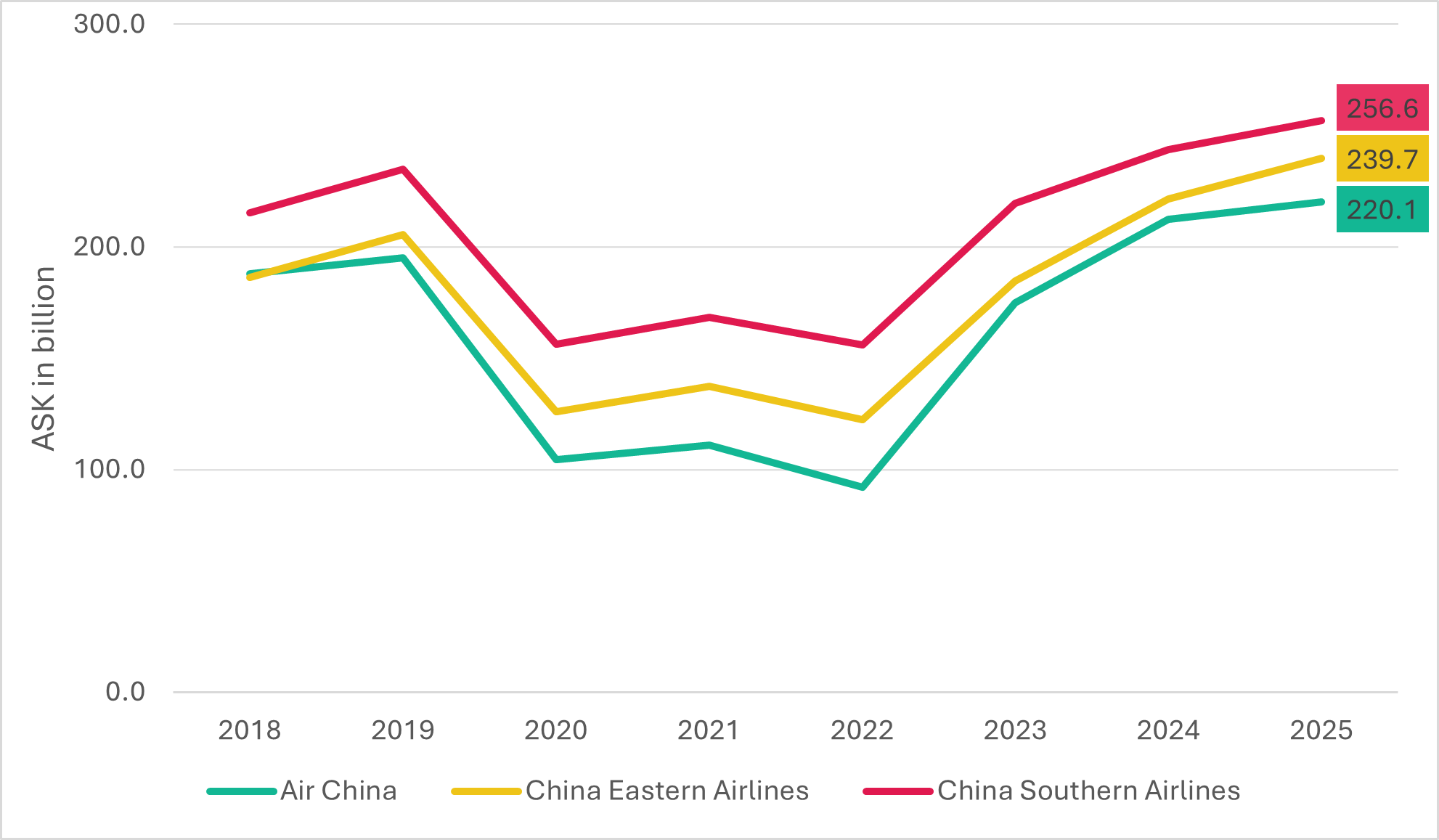

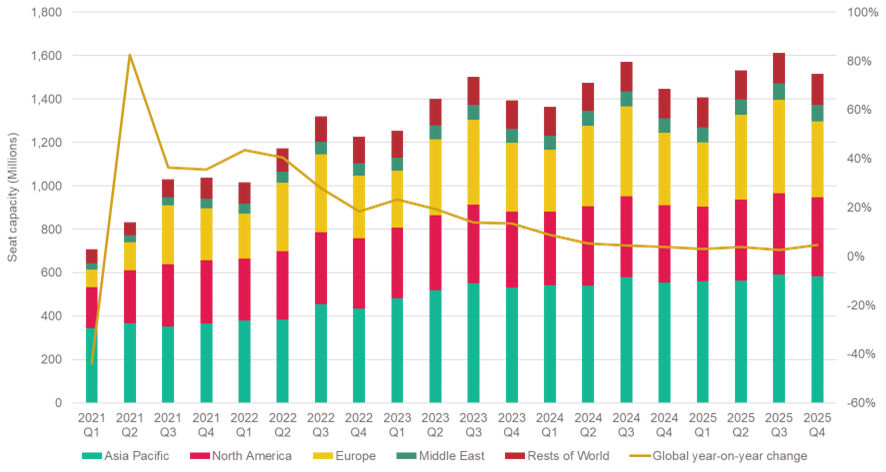

As network capacity expands to meet renewed demand, maintaining operational reliability continues to be a key challenge. Forecasts for the first quarter of 2026 indicate a 5% increase in capacity across Asia, equating to about 31 million additional passengers.

While this demonstrates strong market momentum, it places more pressure on infrastructure, processes, and resources that are already under strain.

Leading the panel discussion was Ellis Taylor of Cirium joined by colleague Hamsin Nashrudin, and guest speakers Anthony Cicuttini from Brisbane Airport and Nate Srinath from Inxee.

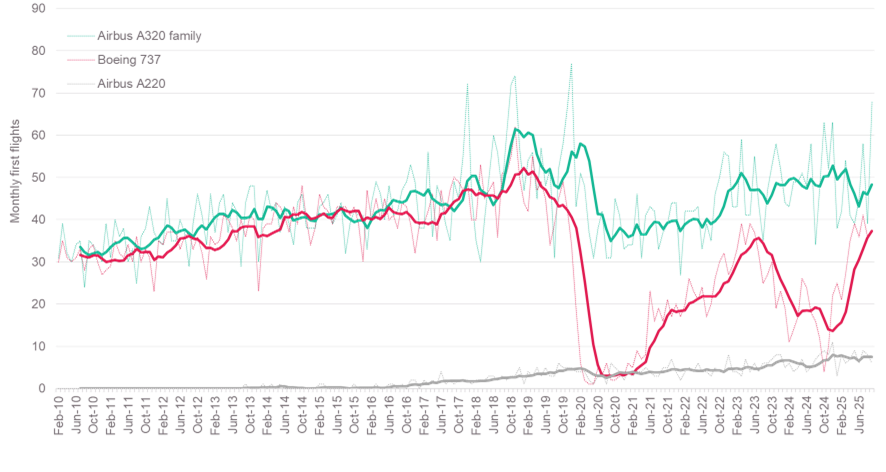

Despite network expansion continuing reliability remains a central concern. Cirium data shows that flight cancellation rates in 2025 remain above the pre-pandemic baseline of roughly 1–1.5%. Even a small uptick results in tens of thousands of additional monthly cancellations, directly affecting passenger experience and operational stability. As the sector scales up, reinforcing reliability shifts from operational concern to a strategic priority – and a key competitive advantage.

Ongoing supply chain challenges and aircraft delivery delays are set to further constrain available fleet growth, despite infrastructure investments. The recent addition of airports in markets such as Navi Mumbai and Noida adds needed capacity, but these projects must be matched with adequate aircraft resources and integrated networks to realize their full benefits.

Driving operational efficiency in aviation

Airports are responding to capacity and reliability pressures by leveraging advanced analytics and artificial intelligence (AI) to streamline operations, alongside strategic infrastructure enhancements.

The emphasis is on maximizing efficiency from existing assets, while new facilities like Navi Mumbai and Noida expand capacity. However, technology and infrastructure must advance together to achieve measurable improvements in performance.

From docking systems to intelligent hubs

A clear example of this transition is the evolution of Visual Docking Guidance Systems (VDGS). Once limited to basic stand guidance, next-generation VDGS platforms now serve as intelligent operational nodes. AI enables these systems to go beyond traditional roles by automating billing with precise arrival timestamps and reducing revenue discrepancies from manual reporting. This digital transformation helps resolve longstanding operational inefficiencies and lays a foundation for broader process innovation.

Critically, these intelligent platforms are transforming airport turnaround performance by capturing granular timestamps for each step of the process, creating robust datasets for targeted operational analysis—from chocks-on and aerobridge placement to passenger transfer, refueling, and baggage movement. Ready access to these detailed metrics empowers teams to identify bottlenecks and inefficiencies, supporting continuous improvement in processes and asset utilization.

Enhancing safety and efficiency

AI-enabled systems also play a crucial role in enhancing airside safety. The latest smart VDGS platforms can automatically identify aircraft types and verify wingtip clearance during docking, reducing collision risk and protecting operational integrity. By streamlining processes and improving reliability, these technologies strengthen the resilience of the airport environment.

Brisbane Airport: a case study in data-driven strategy

With traffic projected to reach 35 million passengers over the next decade, Brisbane Airport (BNE) uses Cirium’s FM Traffic and SRS Analyzer to conduct data-driven assessments that allow it to proactively manage its relationships with airlines, and make infrastructure investment decisions.

Using Cirium’s FM Traffic and SRS Analyser, BNE compares individual routes across an airline’s portfolio and identify opportunities for new services or increased frequency by combining real-time passenger flow with detailed schedules.

This analytical approach reshapes how BNE develops airline partnerships. Rather than relying on anecdotal feedback, the airport enables collaborative, evidence-based discussions on network performance and shared opportunities. They effectively identify key drivers and co-develop actionable strategies—whether refining capacity allocation or launching targeted joint marketing campaigns.

Building the Future of Air Travel

Successfully navigating this landscape requires adopting integrated, intelligence-led operational models. Aviation analytics now underpin decision-making across key areas—demand forecasting, network optimization, turnaround management, and safety protocols. Embedding data-driven insights into strategy and execution enables stakeholders to respond proactively to changing conditions, mitigate disruptions, and chart a path toward resilient, efficient, and effective operations.

In the evolving landscape of commercial aviation, organizations that put analytics at the core of their operations are best positioned for long-term success. The future of air travel will be defined not just by volume, but by how intelligently and efficiently each journey is enabled.

Airports and airlines that leverage real-time intelligence and predictive analytics drive operational excellence, strengthen network resilience, and consistently deliver a reliable, seamless passenger experience.