Simon Mills, Principal MRO Research Specialist, Cirium

If you fail to plan, you plan to fail. Or so the adage goes.

Yet not everything can be planned for, and in an increasingly volatile world even the best-laid plans are being tested. A squall may be visible on the horizon, but forecasting rain does not guarantee you will stay dry.

Planning has changed. Aerospace decisions are now made under volatility, not certainty. Production, maintenance capacity and aftermarket positioning must be aligned before demand fully materialises.

Internal data explains what has already happened. In moments of crisis, when instinct and emotion can easily take over, independent data shows where utilization, demand and operational pressure are building – early enough to act.

Case Study: Ryanair’s pandemic resilience

The COVID-19 pandemic was a true black-swan event, sending shockwaves across the aviation industry. Few carriers were prepared, yet some responded faster than others and recovered more quickly. With the benefit of hindsight, it is possible to see more clearly how the industry’s most resilient airlines behaved.

Ryanair stands out. Its response was more agile than the broader global trend, and a series of decisive moves helped position the airline for a faster recovery.

Source: Cirium Ascend Ground Events

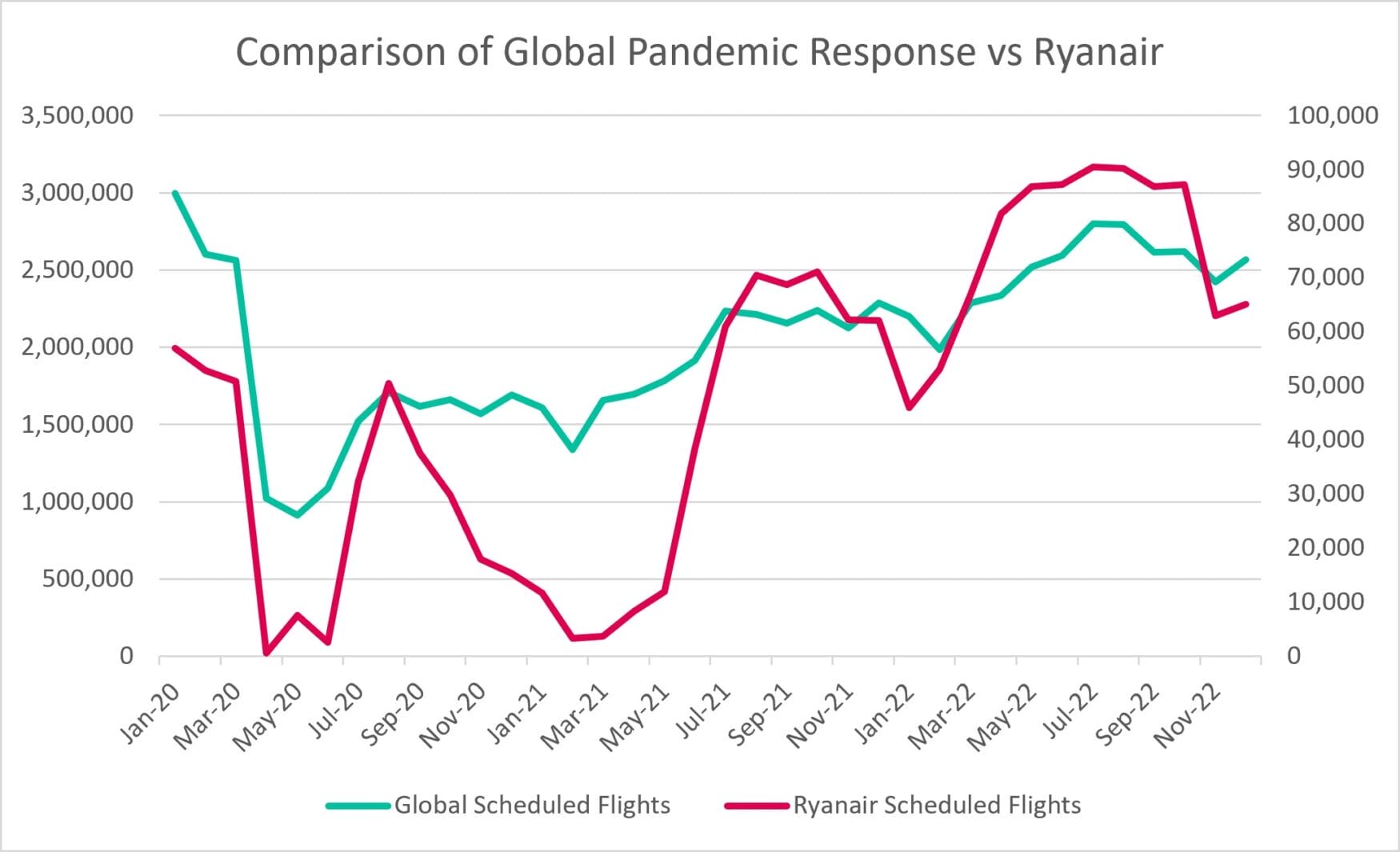

Examining scheduled flights data and comparing Ryanair with the wider global trend reveals the scale of the pandemic shock and the airline’s speed of recovery.

The above chart captures the sharp global collapse in flights from March 2020, a downturn that lasted through the summer and marked the first wave of the pandemic. Europe then experienced a second wave in the winter, with repercussions lasting well into 2021. This pattern was not universal, but it is visible in the global numbers as a second trough around the first quarter of 2021.

Ryanair was not immune to either wave, and the impact is clear in the data. What distinguishes the airline is its recovery trajectory, particularly after the initial shock. By the summer of 2020, it had already climbed back towards near pre-pandemic flight volumes. By contrast, the global market did not return to comparable pre-COVID levels until early 2022.

After the second setback that affected Europe, Ryanair again rebounded quickly towards its usual flight volumes. The modest dip during the winter of 2021/22 appears more consistent with normal seasonality than with lingering pandemic disruption.

What this reveals for aerospace

Airline behaviour shapes upstream demand. When aircraft return to service faster, maintenance cycles compress, parts demand accelerates, and capacity constraints surface earlier than expected. Without visibility into real-world utilisation, these signals are missed – leaving MRO capacity misaligned and aftermarket sales reactive rather than planned.

What enabled this rapid recovery?

Ryanair’s unique response

Source: Cirium Ascend Ground Events

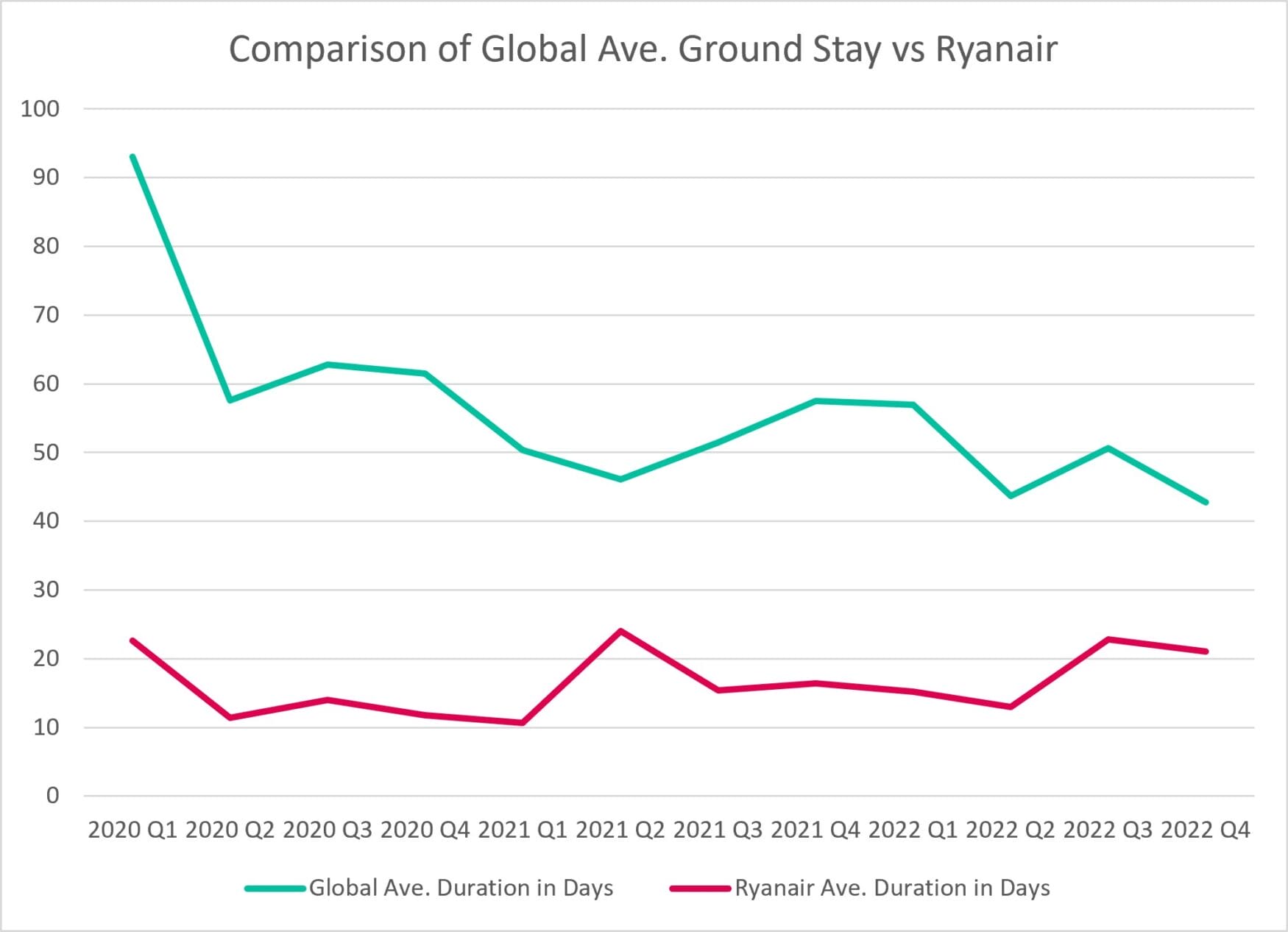

The ground-time data offers insight into that recovery. Ryanair’s approach to the crisis was distinct, and the airline separated itself from the wider pack.

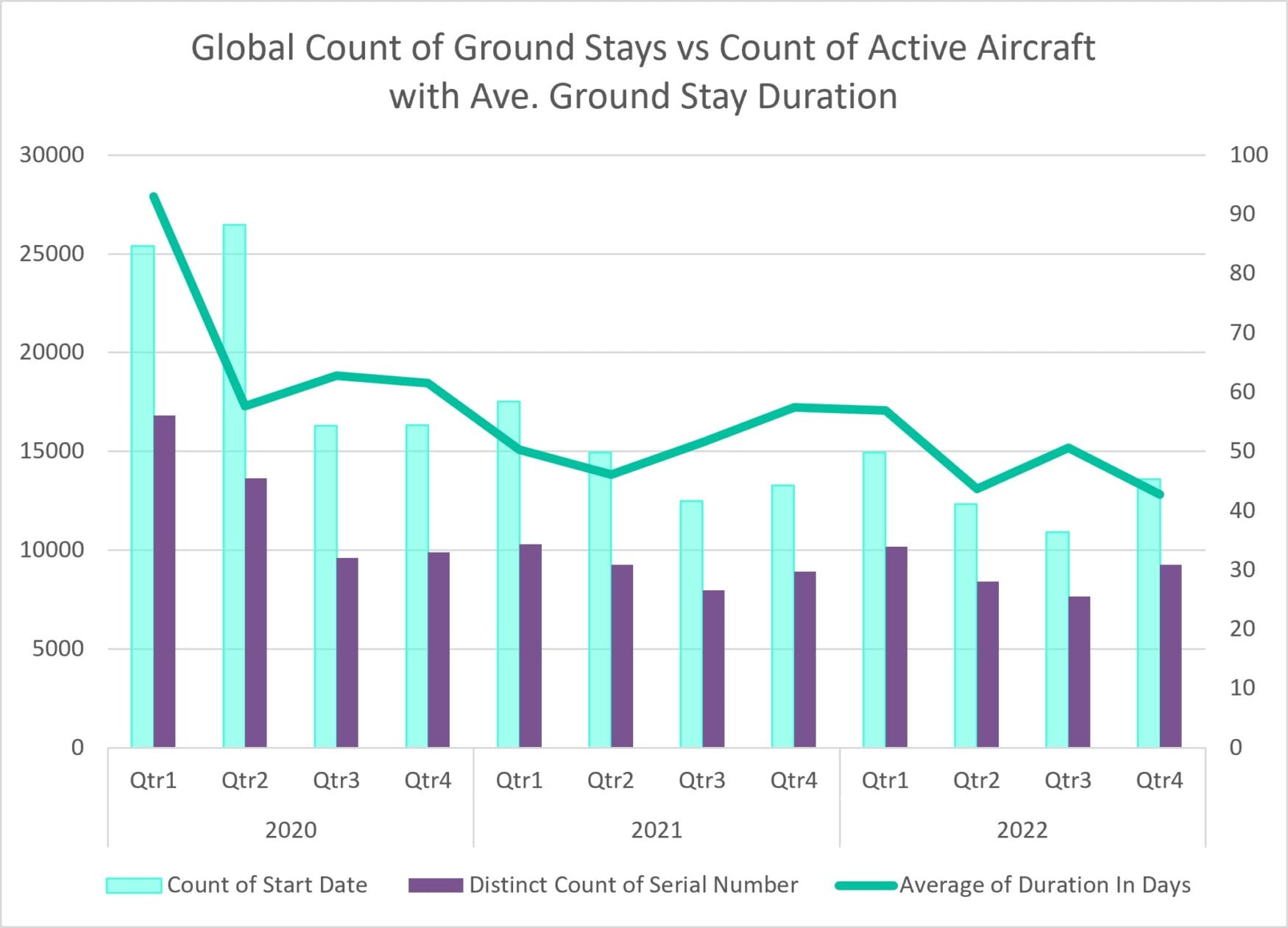

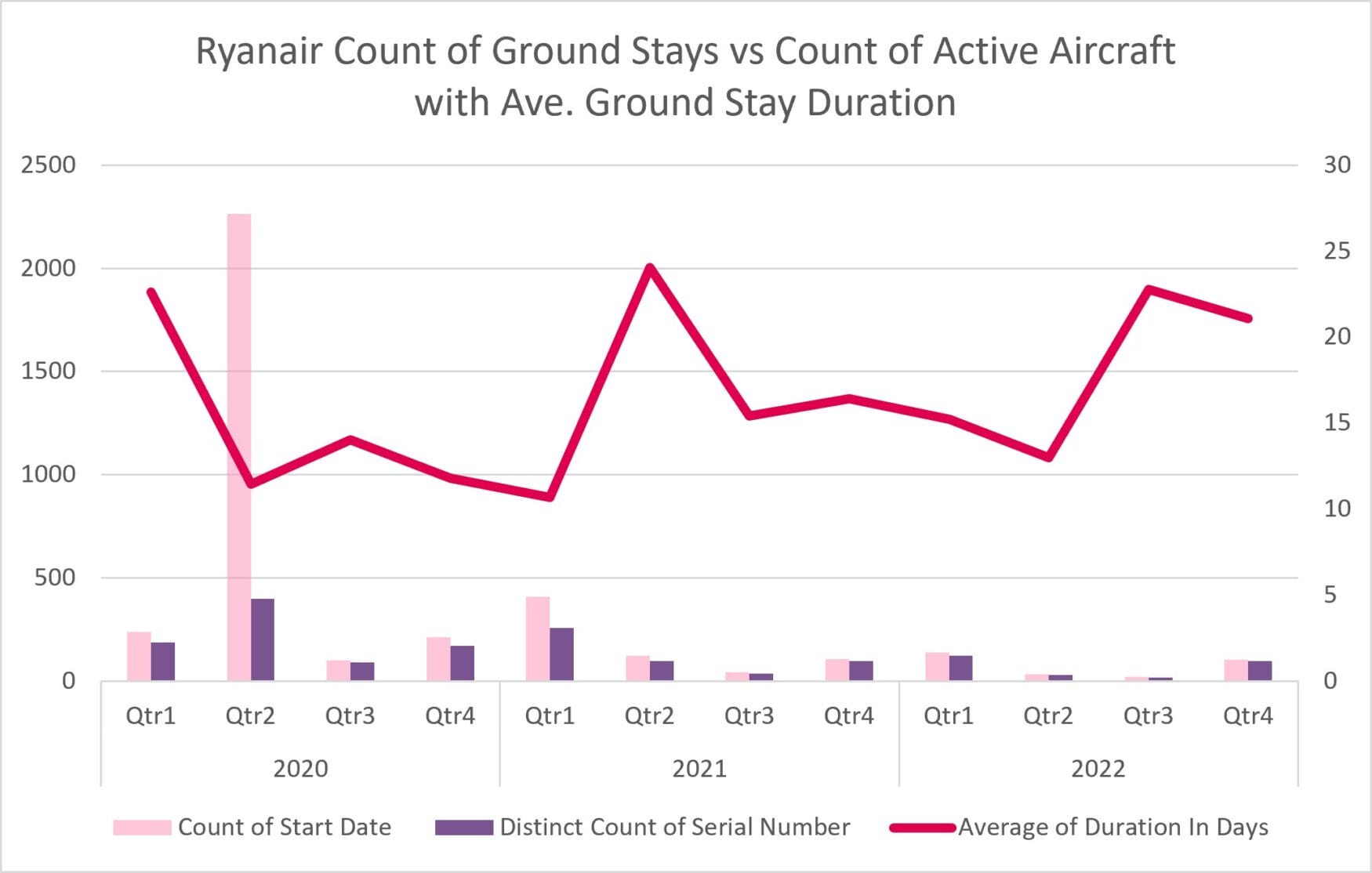

The average duration of each ground stay was significantly lower than the global average. That alone does not show the full picture, however. The ratio of ground stays to fleet size helps show what Ryanair was doing differently.

Source: Cirium Ascend Ground Events

What these charts suggest is that Ryanair’s lower average ground-stay duration sat alongside an unusually high number of ground stays per aircraft, averaging nearly six compared with a normal of around 1.2.

Globally, the ratio rose to almost two ground stays per aircraft in the second quarter of 2020, up from a more typical level of around 1.5. Combined with an average duration of nearly 60 days, that points to aircraft remaining grounded for long stretches.

Ryanair’s data is markedly different. In the same quarter, its average ground-stay duration was only around 11 days, yet each aircraft recorded roughly five separate ground stays. The airline also appeared to disperse aircraft widely across its network. Under normal operating conditions, Ryanair tends to record ground stays of more than a week at only 10 to 20 airports. During the worst of the pandemic-induced grounding, that figure expanded to 45 locations. This was a major departure from the norm. By comparison, the global pattern showed little variation, with most airlines either bringing aircraft back to base or sending them to storage sites.

The effect of Ryanair’s strategy was that its aircraft rarely entered into a fully stored state avoiding the lengthy maintenance burden associated with a full return to operation. This matters upstream. Shorter ground periods reduce the lag between operations and maintenance demand, bringing forward heavy checks and increasing pressure on parts availability. Distributing aircraft across so many locations was strategically astute as well, positioning the airline to restore a range of routes quickly once restrictions eased. Together, those choices meant Ryanair was able to respond almost immediately, while many competitors were still trying to reactivate their fleets.

Aerospace implication

- Bring forward maintenance demand signals

- Compress decision windows for MRO capacity

- Reduce margin error in inventory planning

That strategy was not without risk. With no certainty over when demand would return, Ryanair continued to incur operating costs including fuel and crew expenses without the support of matching revenue. It was a costly call but ultimately paid off. Crucially, it also appears to have been a data-led decision.

With its long-standing focus on operational efficiency, Ryanair has invested in the infrastructure and decision-making discipline needed to use data effectively. That helps explain both its resilience and the strength of its response amid crisis.

CASE STUDY

Qatar Airways and regional uncertainty

Cirium recognised Qatar Airways for its operational excellence by awarding it the 2025 Platinum Airline Award. That achievement was especially notable given the scale of disruption the carrier had faced because of political volatility in the region.

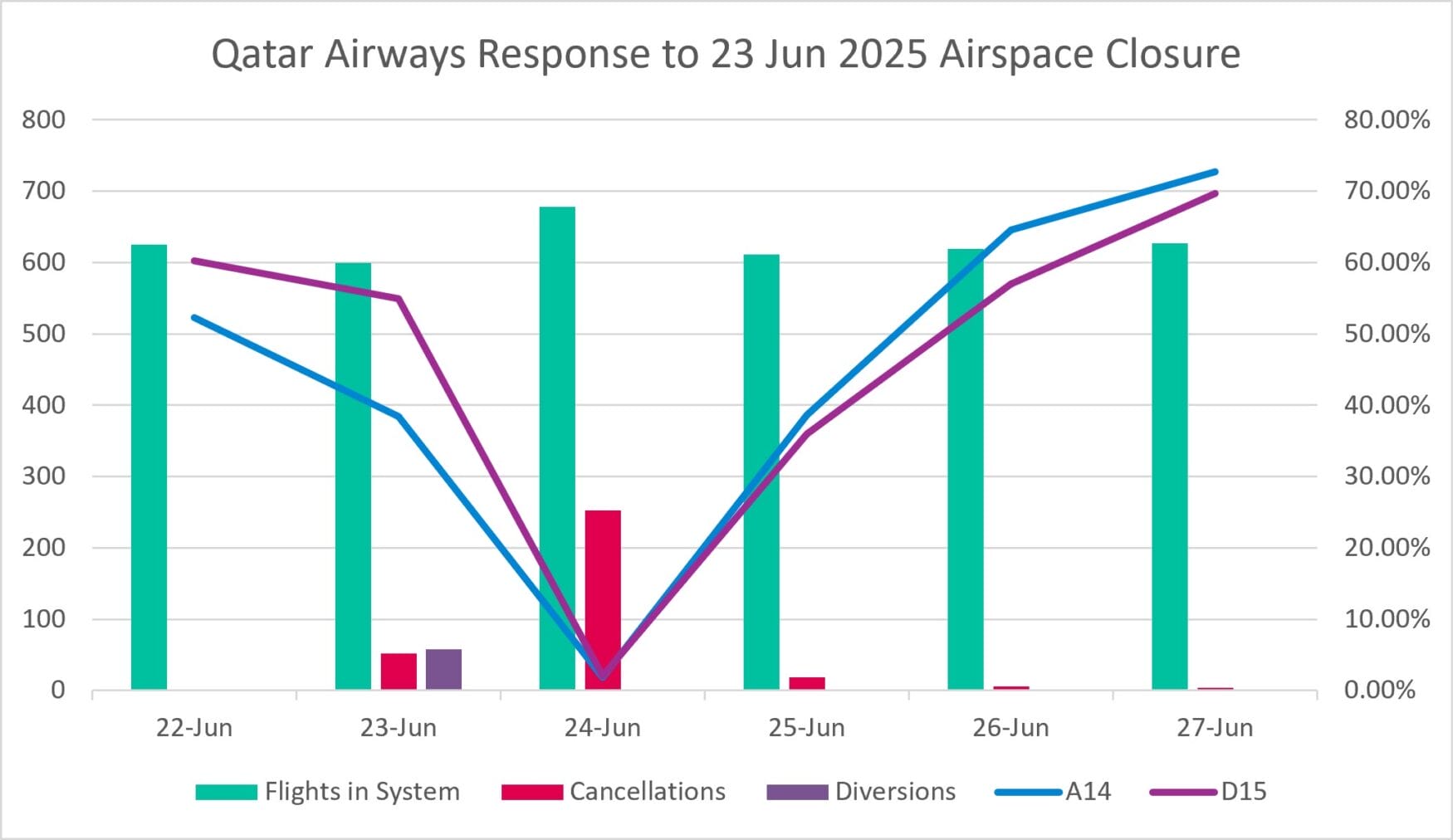

On June 23, 2025, Qatari airspace closed after missiles were launched at Al Udeid air base in Qatar. It was an unforeseeable event, and the consequences of shutting the airspace around Doha, the airline’s central hub, were significant.

For aerospace organisations, airspace closures reshape demand signals across the value chain. Maintenance requirements shift, fleet positioning changes and aftermarket demand redistributes geographically.

Source: Cirium Journey

Looking at flights across the six days surrounding the closure, both the scale of the disruption and the speed of the response become visible. Sunday June 22, reflects normal operations before the closure. Because the airspace shut in the evening on June 23, the operational effects are seen most clearly the following day.

For an airline built on a hub-and-spoke model, losing access to Doha should have been deeply damaging. Yet by Friday, June 27, operations had returned to almost normal levels.

Real-time operational data allowed Qatar Airways to act before conditions stabilized. The airline uses data to maintain operational discipline and make proactive decisions under pressure, which in turn, helps contain disruption and accelerate recovery. For aerospace, the same principle applies, decisions need to be made before certainty emerges – not after. The important point is that the exercise of this capability is repeatable under pressure, not dependent on circumstance.

Repeatability under pressure

The advantage is not speed alone. It is consistency.

Data-led organisations do not respond well once. They respond the same way every time conditions change. For aerospace, this is critical:

- Forecast maintenance demand before heavy checks are triggered

- Align MRO capacity ahead of utilization and ground event changes

- Position inventory ahead of emerging aftermarket demand signals

Repeatability reduces exposure to timing risk – across capacity, inventory and capital decisions.

Recovery speed shows what happened. Repeatability shows what can be relied on. Across multiple disruptions, the pattern is consistent – data enables earlier, more confident decisions under pressure.

Qatar Airways repeatable recoveries

Source: Cirium Journey

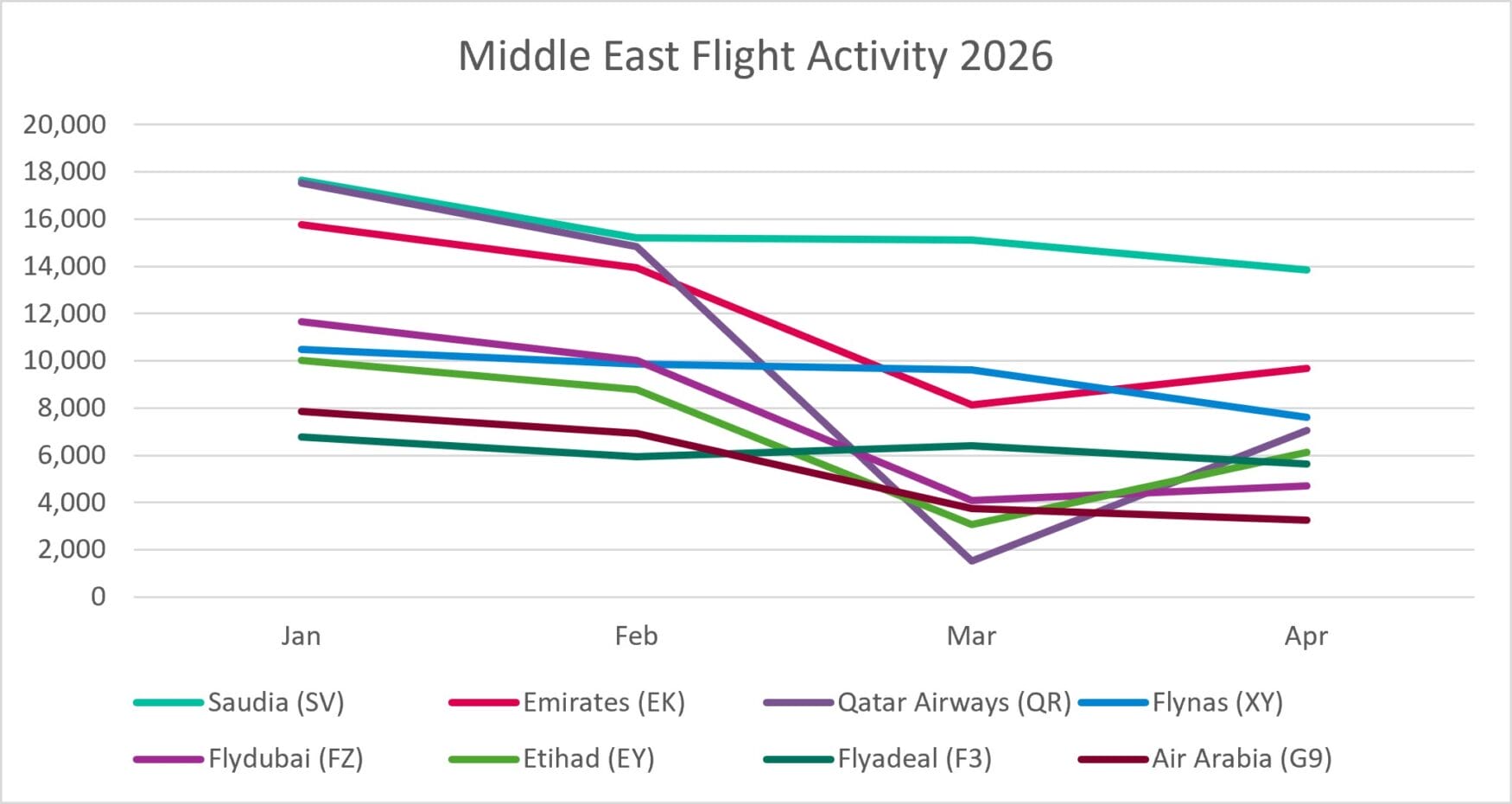

Political instability did not ease in 2026, and Qatar Airways again found itself directly exposed to events in the region as Qatari airspace was closed from February 28. It was not meaningfully reopened for commercial operations until April 20, and even then, restrictions remained in place.

Once again, the speed of the rebound stands out. Qatar Airways was among the carriers most heavily affected by the closure of Qatari airspace, yet its recovery trajectory appears steeper than that of other operators in the region.

Source: Cirium Journey

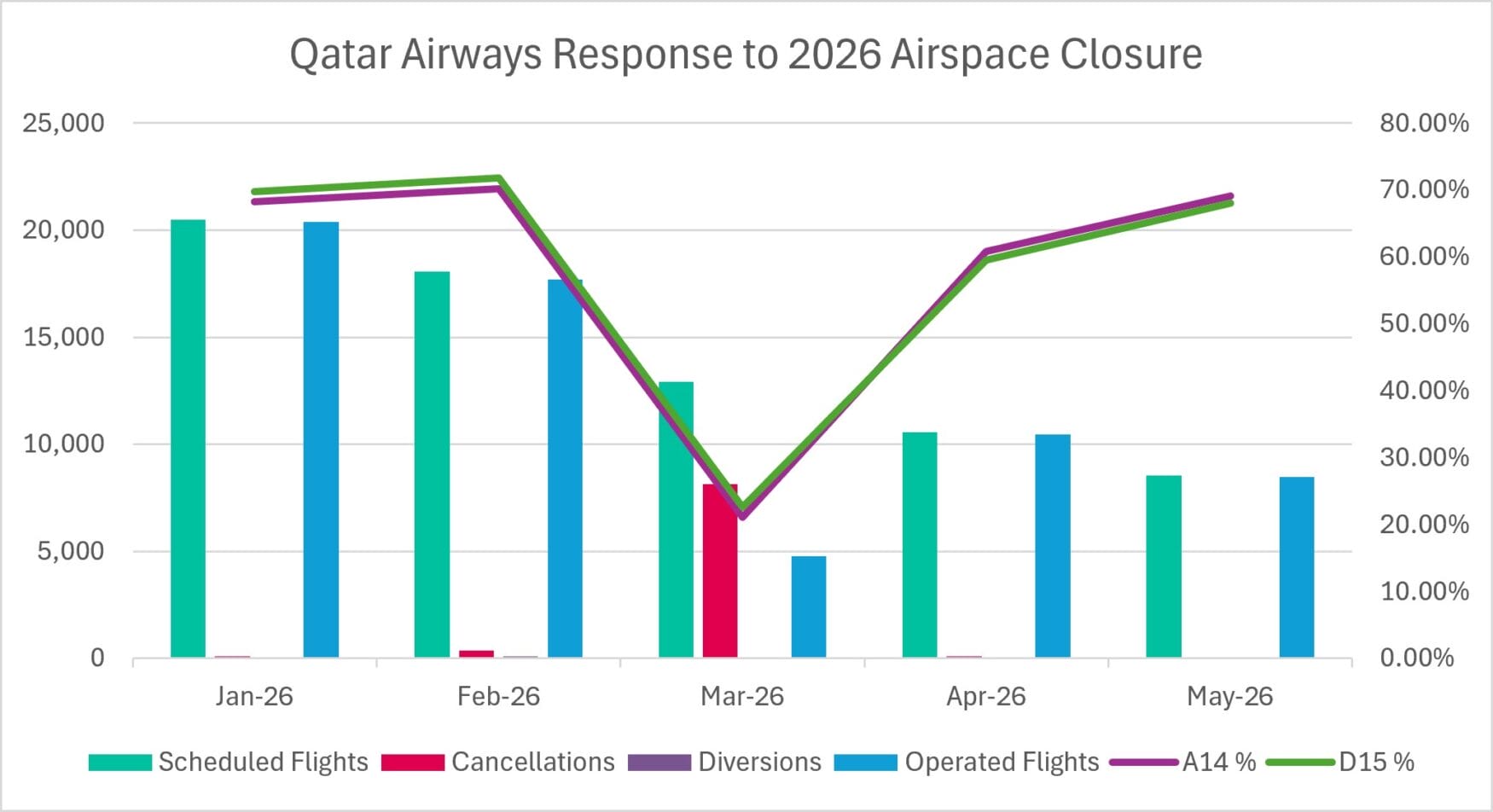

Analysis of 2026 flights data highlights the same pattern of operational efficiency and decisive action under unpredictable conditions. March appears to have been the peak period of instability, with high cancellation volumes and a sharp drop in both A14 and D15 performance. Although airspace restrictions remain, Qatar Airways has largely recovered, operating 99% of scheduled flights, up from 36% at the height of the disruption.

Learning Curve

Source: Cirium Ascend Ground Events

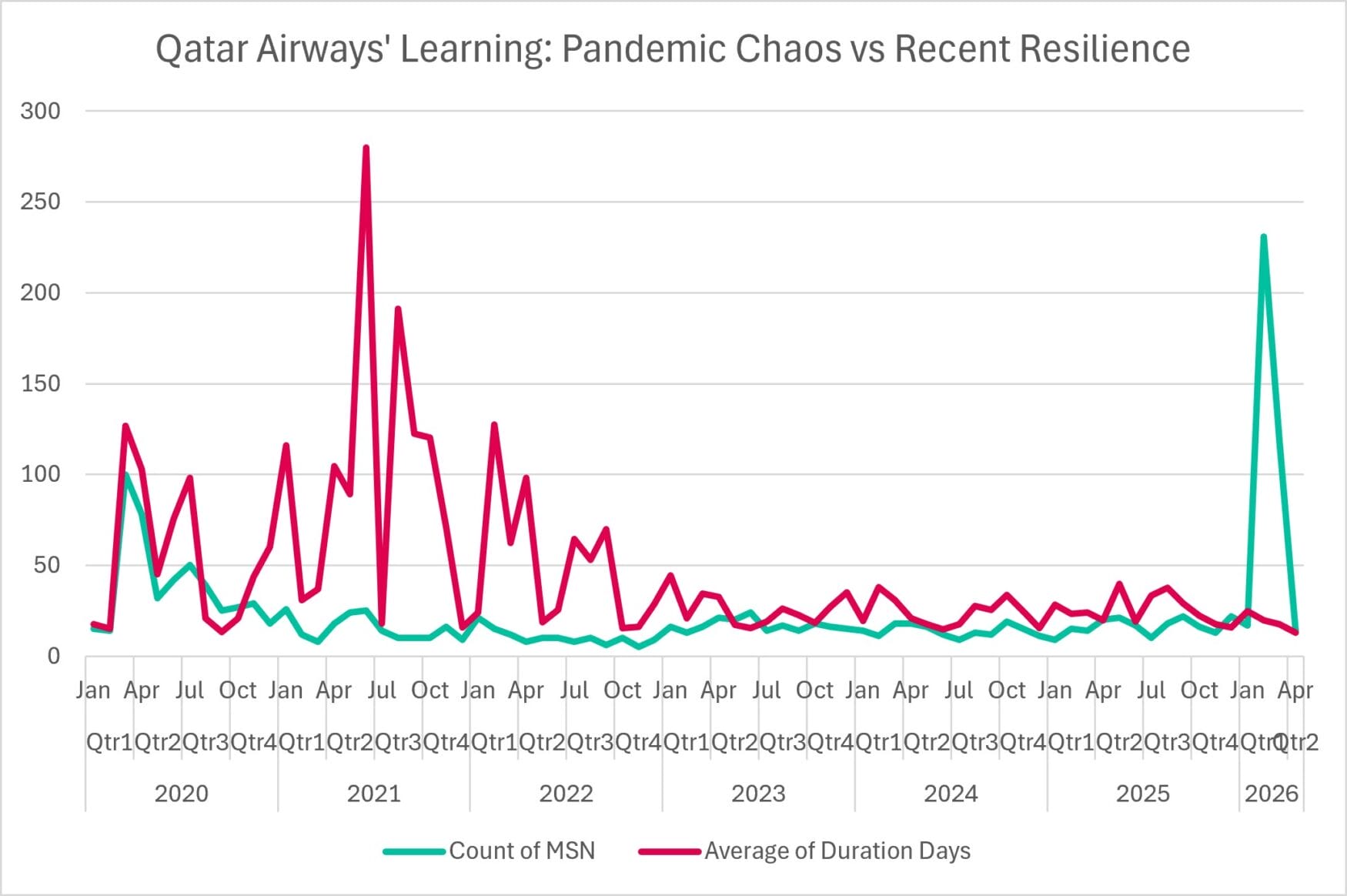

Qatar Airways’ investment in data appears to have been partly shaped by earlier periods of disruption. If we return to the comparison between Ryanair and global pandemic activity, Qatar Airways broadly followed the wider industry pattern in 2020, with aircraft grounded for extended periods.

The airline was then hit by the A350 paint issues that emerged at the end of 2020 and continued through 2021, grounding aircraft for substantial periods. In response, Qatar Airways had to reshape its longer-term fleet plan, bringing A380s back into service and retaining A330s that had been due to leave the fleet in favour of A350s, 787s, and eventually 777X aircraft.

Normal operations resumed from 2023 with relatively few disruptions. The airline’s response to the latest turmoil, however, looks far more proactive and data-driven than its earlier crisis posture. The contrast between its 2026 response to airspace closures and its 2020 pandemic response is striking, and in some respects echoes the agility Ryanair demonstrated: shorter ground stays, faster repositioning, and a stronger focus on maintaining operational flexibility.

Of course, the two scenarios were very different. Qatar Airways could not bring aircraft back to Doha with the airspace closed, nor could they move aircraft to Doha. In some senses, Ryanair had a lot more agency around decision making, in terms of aircraft positioning.

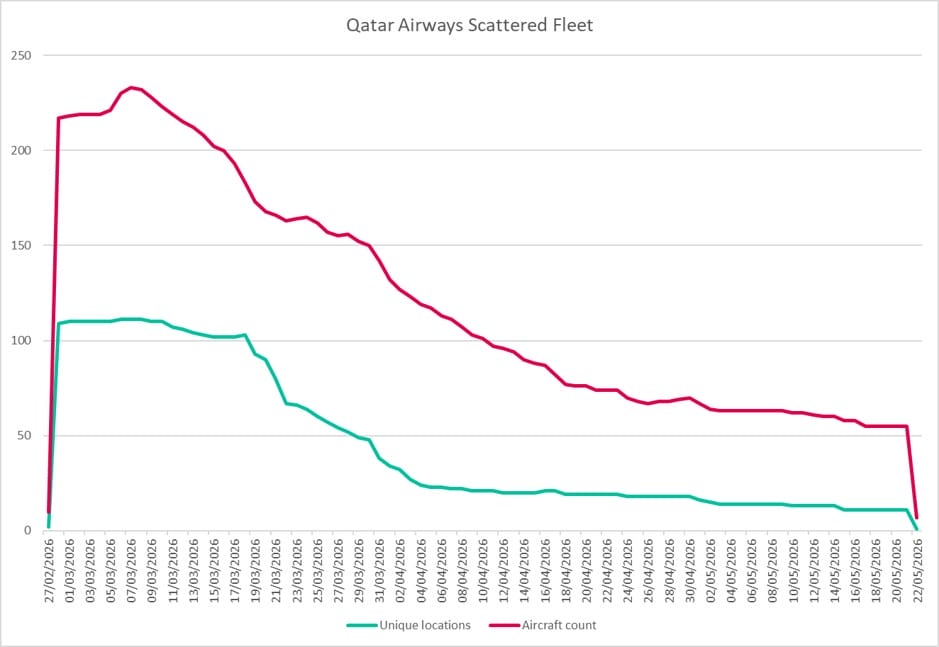

On February 28, the day of the airspace closure, Qatar Airways had its fleet spread across 109 different airports around the world. With the uncertainty as to when the airspace might reopen and the complexities around crew hours and placement, Qatar Airways was faced with significant challenges.

However, with airspace still closed over Doha, it managed to effectively reposition the fleet so that by the start of April its aircraft were concentrated at 34 airports. This shift from global dispersion to consolidation is the product of strategic planning. Some aircraft were brought back to Doha as part of the limited reopening of the airspace, some were held at key regional nodes, and a few were moved to specific parking/storage locations. This is evidence of the airline exerting control and resuming robust service, albeit at depleted levels of flights. Aircraft were stationed at anchor locations for long-haul services, with others positioned at key staging points to preserve operational flexibility.

The shift is not just faster response. It is a repeatable decision model built on independent data. For aerospace organisations, this enables consistent planning across cycles – not isolated success during disruption.

These examples show how data can support planning in a market that no longer behaves predictably – it changes when, and how early you act. For aerospace organisations, the difference is critical. Those who wait for certainty align too late – capacity, capital and inventory follow the market instead of leading it. Those with independent, external visibility act earlier, aligning maintenance and capacity before demand peaks, positioning inventory ahead of aftermarket cycles, and making defensible decisions under pressure.