Eleni Maragkou, Valuations Analyst, Cirium Ascend Consultancy

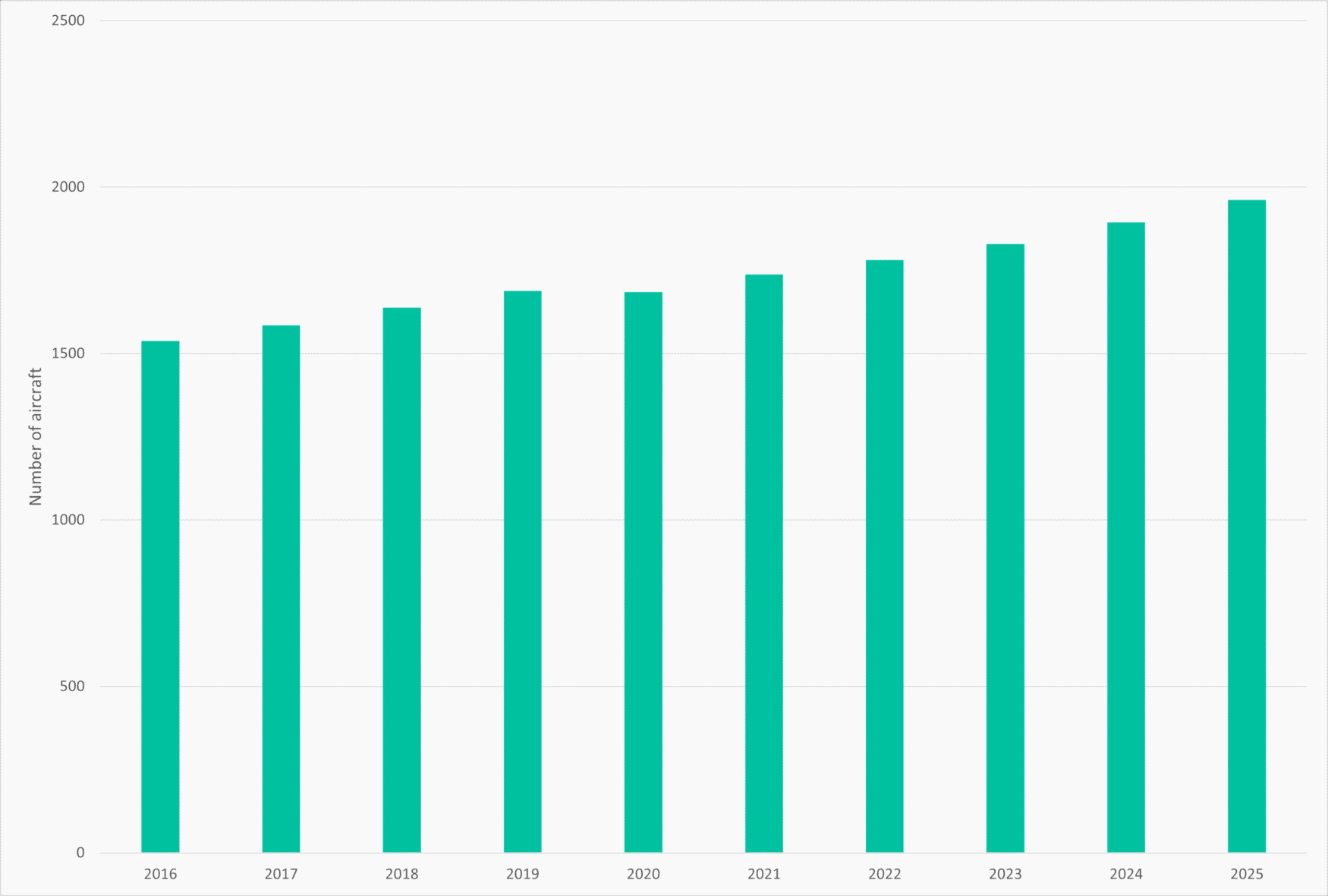

Between 2015 and 2025, the intermediate twin-engine helicopters have recorded consistent growth in fleet size, resulting in an increase in their share of the overall fleet. This reflects a sustained expansion of the segment alongside broader market growth. Historical fleet data is based on year-end positions, while forecast data reflects the 2025-2034 outlook.

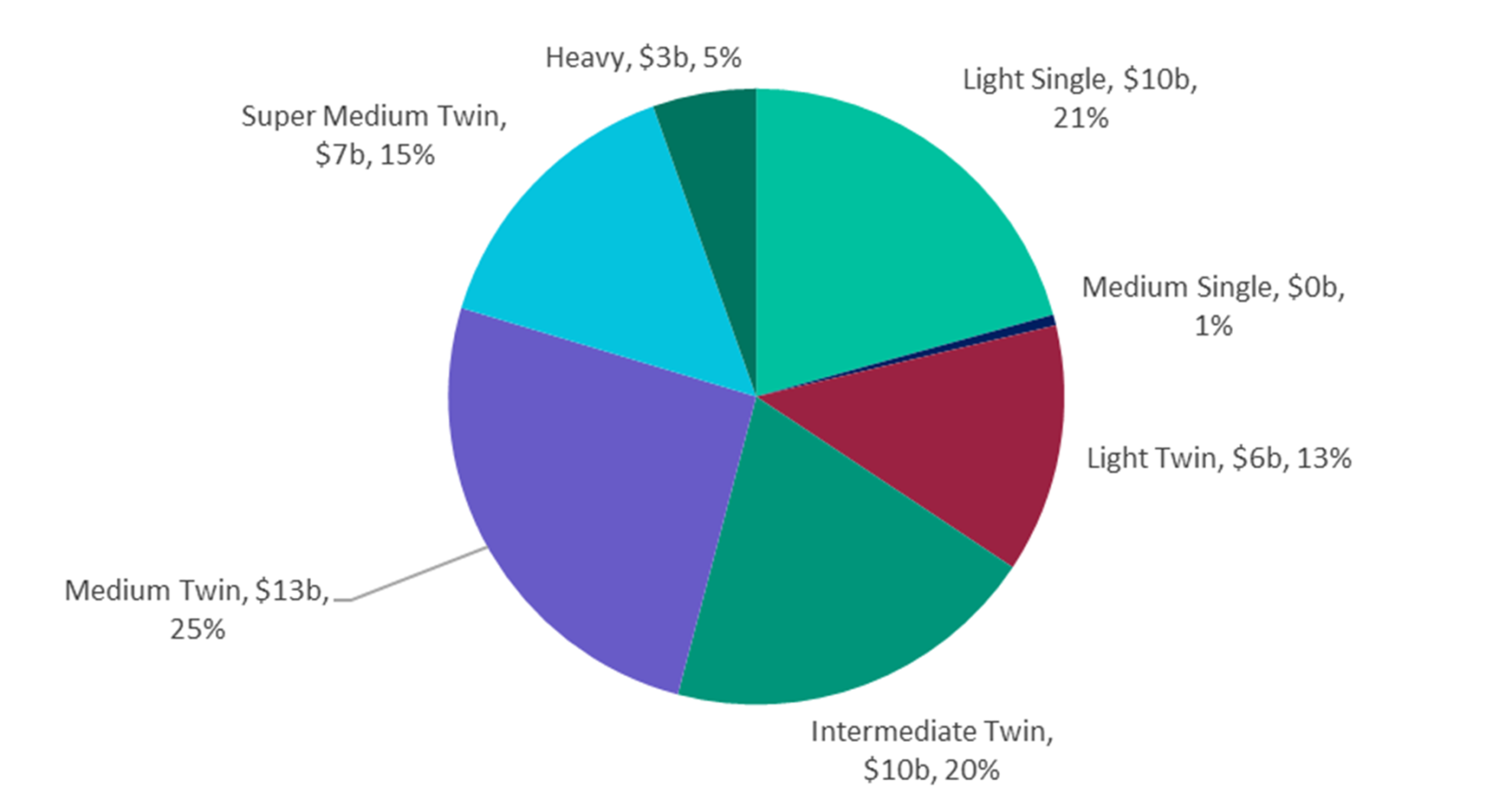

The Cirium Helicopter Fleet Forecast (2025) indicates that intermediate twins accounted for approximately 10% of total deliveries over the past decade and are expected to increase to around 14% over the next ten years, representing a rise of approximately four percentage points. In value terms, the segment is forecast to represent approximately 20% of total market value, equivalent to around $10 billion between 2025 and 2034. This positions the intermediate twins as the third largest segment by value, supporting their growing importance within the overall market.

Chart 1 shows that intermediate twins have experienced consistent growth in fleet size over the past ten years, broadly tracking their share within the fleet mix.

Chart 1: Intermediate-twin in-service fleet trend – past 10 years

Source: 2025 Helicopter Fleet Forecast

The 2025 Helicopter Fleet Forecast highlights the forward outlook for the segment, with intermediate twins expected to account for approximately 20% of total market value over the 2025 to 2034 period. This reflects continued demand for aircraft that provide a balance between capability and cost, supporting their position as a core segment within future market activity.

Chart 2: Fleet forecast of civil helicopter deliveries by value 2025-2034

Source: 2025 Helicopter Fleet Forecast

Fleet development data, further illustrate how these trends translate at an asset level. The Airbus Helicopters H145/EC145 fleet has grown from fewer than 100 aircraft in service in the early 2000s to approximately 900 aircraft by end of Q4 2025. Over the same period, storage levels have remained below 5% of the fleet, indicating that the majority of aircraft are actively deployed. This is relevant from a value perspective, as low storage levels typically indicate that supply is closely aligned with demand, supporting liquidity and reducing the risk of downward pressure on values. At the end of Q4 2025, 486 H145/EC145 aircraft were in service in the Emergency Medical Services (EMS) sector across 74 operators worldwide. This concentration within a single mission profile demonstrates the aircraft’s established role in core segment and supports consistent demand.

The Leonardo AW169 shows a consistent growth profile, with the fleet increasing from entry into service 2015, to approximately 200 aircraft by Q4 2025 with storage levels remaining minimal. This indicates that new deliveries are largely being absorbed into active operations. As of Q4 2025, 59 aircraft were deployed in EMS roles across 19 operators worldwide, showing that the type has also established a presence within key mission segment.

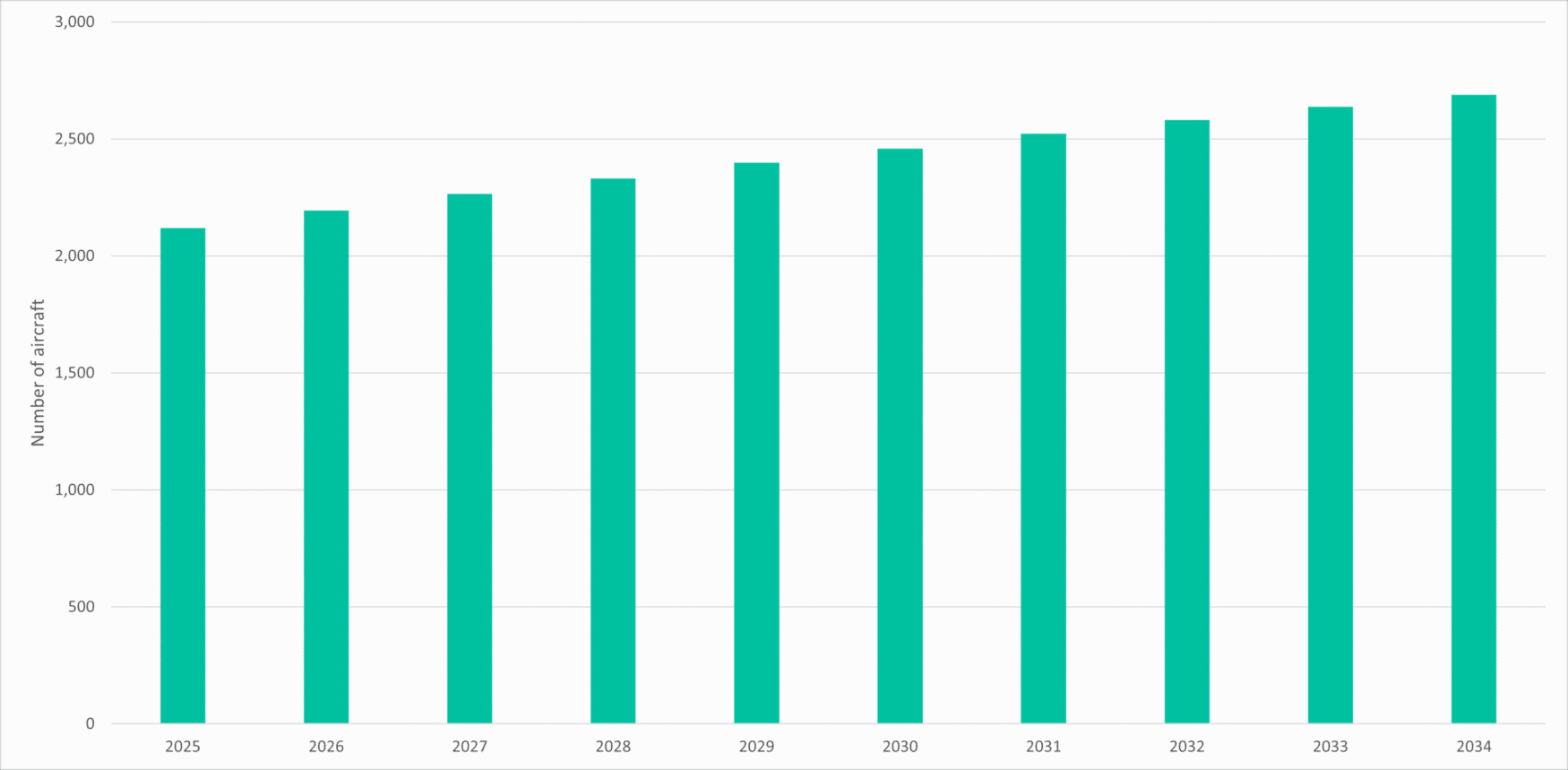

Chart 3 shows that intermediate twin helicopters are expected to increase their share of total fleet over time. When considered alongside historical fleet development, this indicates that the segment’s growth is both established and expected to continue over the forecast period to 2034.

Chart 3: Forecast intermediate-twin helicopter fleet to 2034

Source: 2025 Helicopter Fleet Forecast

The expansion of intermediate twins over time reflects broader changes in how operators are selecting aircraft. In Europe in particular, intermediate twins have become increasingly prevalent in EMS operations following regulatory changes which amongst other things include the requirement of improved safety performance in the event of an engine failure. This has contributed to a shift from smaller platforms towards aircraft capable of meeting these requirements, supporting increased adoption of types such as the H145. As a result, replacements and upgrade activity have seen types such as the AW109 and H135 moving into secondary markets, particularly outside Europe, where requirements and mission profiles differ.

From a value perspective, fleet scale and utilisation across multiple operators are key indicators of market depth. The H145 benefits from a larger installed base established operator network, supporting consistent levels of market activity and stable storage trends. The AW169, has demonstrated consistent fleet growth since entry into service and increasing deployment across multiple mission profiles, including EMS (28%), law enforcement (24%) and corporate use (20%). This diversification supports demand across different end markets and contributes to overall market stability.

Leasing activity provides additional support to the segment. The 2025 Helicopter Fleet Forecast indicates that leasing activity has increasingly expanded into intermediate twin helicopters, with the segment accounting for approximately 15% of lessor focus in recent years. This reflects growing confidence in the long-term demand profile. The missions supported by the H145/EC145 and AW169 are often long-term contracts, backed by governments providing favourable credit. Such structures provide predictable revenue streams and contribute to lower perceived asset risk, supporting value retention.

Looking ahead, the increase in market share over the past decade suggests that intermediate twins are becoming an important part of the fleet mix. This is supported by their ability to operate across a range of missions while maintaining a cost profile that is lower than larger aircraft categories. At the same time, continued fleet growth, low storage levels and expanding leasing activity indicate that demand remains aligned with supply.

Overall, the intermediate twin helicopter segment is supported by sustained fleet growth, increasing the share of total market value and continued expansion across core mission profiles. Aircraft such as the Leonardo AW169 and Airbus Helicopters H145/EC145 illustrate how fleet development, regulatory influences and market depth contribute to value behaviour. As the segment continues to mature, its increasing share of total market value combined with consistent fleet expansion and low storage levels, suggest that intermediate twins are likely to remain a core focus for both operators and lessors, supporting continued liquidity and stable value performance over the medium term.