Shruti Salwan, Markets Editor, ICIS

Jonathan Robins, Air Transport Reporter, Cirium

Europe’s jet fuel supply is coming under mounting pressure as the loss of key Middle Eastern export flows, falling global refinery runs and depleted regional stocks collide with rising summer travel demand.

With a sharp increase in prices already being felt, airlines are scrambling to respond.

No slack in the system

The loss of supply from the Gulf — the single largest source of internationally traded jet fuel — has created a structural imbalance at a time when global inventories were already under strain.

According to the International Energy Agency’s (IEA) latest oil market report, global jet fuel demand averaged 7.8 million barrels/day in 2025, with 2 million barrels/day traded internationally.

Gulf exporters accounted for 400,000 barrels/day, around 20% of global trade, making them the single largest supply source. The loss of these flows has created a deep structural imbalance.

The supply tightness is set to worsen as refinery runs decline, with the IEA forecasting a one million barrels/day year-on-year decline in global crude runs in 2026, translating into 200,000 barrels/day lower jet supply versus pre-conflict levels. The impact could peak in the second quarter with up to 500,000 barrels/day removed from the market.

Europe in the firing line

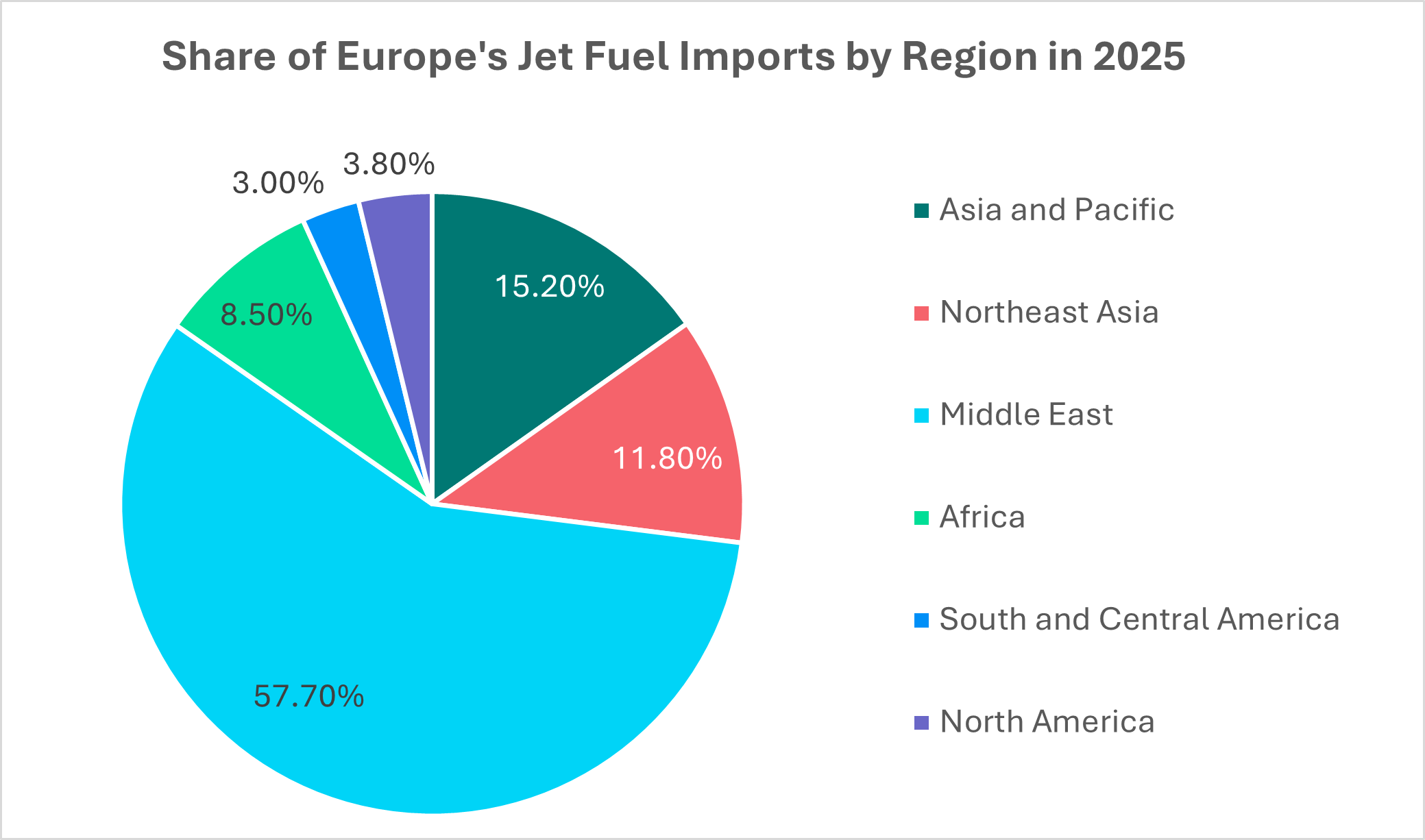

Europe remains particularly exposed as European OECD countries consumed 1.6 million barrels/day in 2025, with 500,000 barrels/day met via imports, highlighting the scale of the current supply shock.

According to ICIS Senior Analyst Man Yiu, “Europe’s monthly deficit of jet fuel averages over 2.5 million tonnes entering into the summer.”

“Close to 60% of imports were sourced from the Middle East in 2025, majority of which comes through the Strait.”

Rising import dependence following post‑COVID refinery closures has further constrained Europe’s ability to absorb supply disruptions.

“Europe is under further pressure as it is likely to receive less volume from Asia. About 27% of imports were sourced from Asia, with India, South Korea, and China the key suppliers, all of which have cut refinery runs due to crude supply disruption and could restrict exports to prioritise local demand,” Man Yiu emphasised.

Source: ICIS Supply and Demand Database

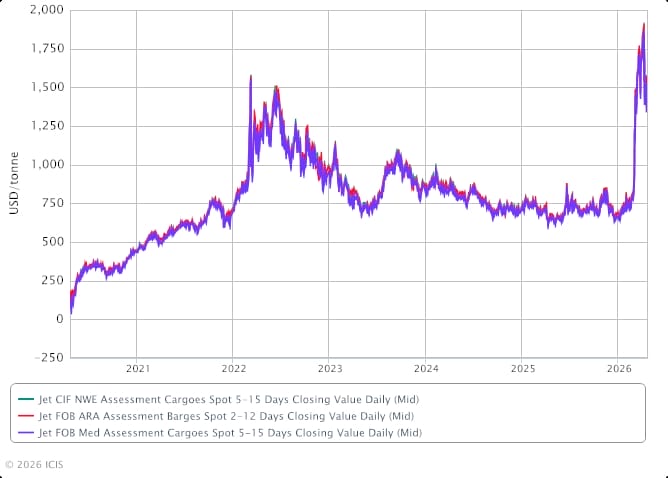

Market fundamentals have tightened rapidly as a result. European jet fuel prices more than doubled over a six‑week period from late February, with Northwest Europe cargoes reaching multi-year highs in early April as geopolitical tensions escalated.

The prompt-month jet fuel crack spread — a measure of refinery margin — soared to the highs of $120/barrel during the period, reflecting the severity of the supply squeeze facing refiners and buyers alike.

While outright prices and cracks have moderated from recent peaks, the market continues to reflect underlying supply fragility, with inventories emerging as a key pressure point.

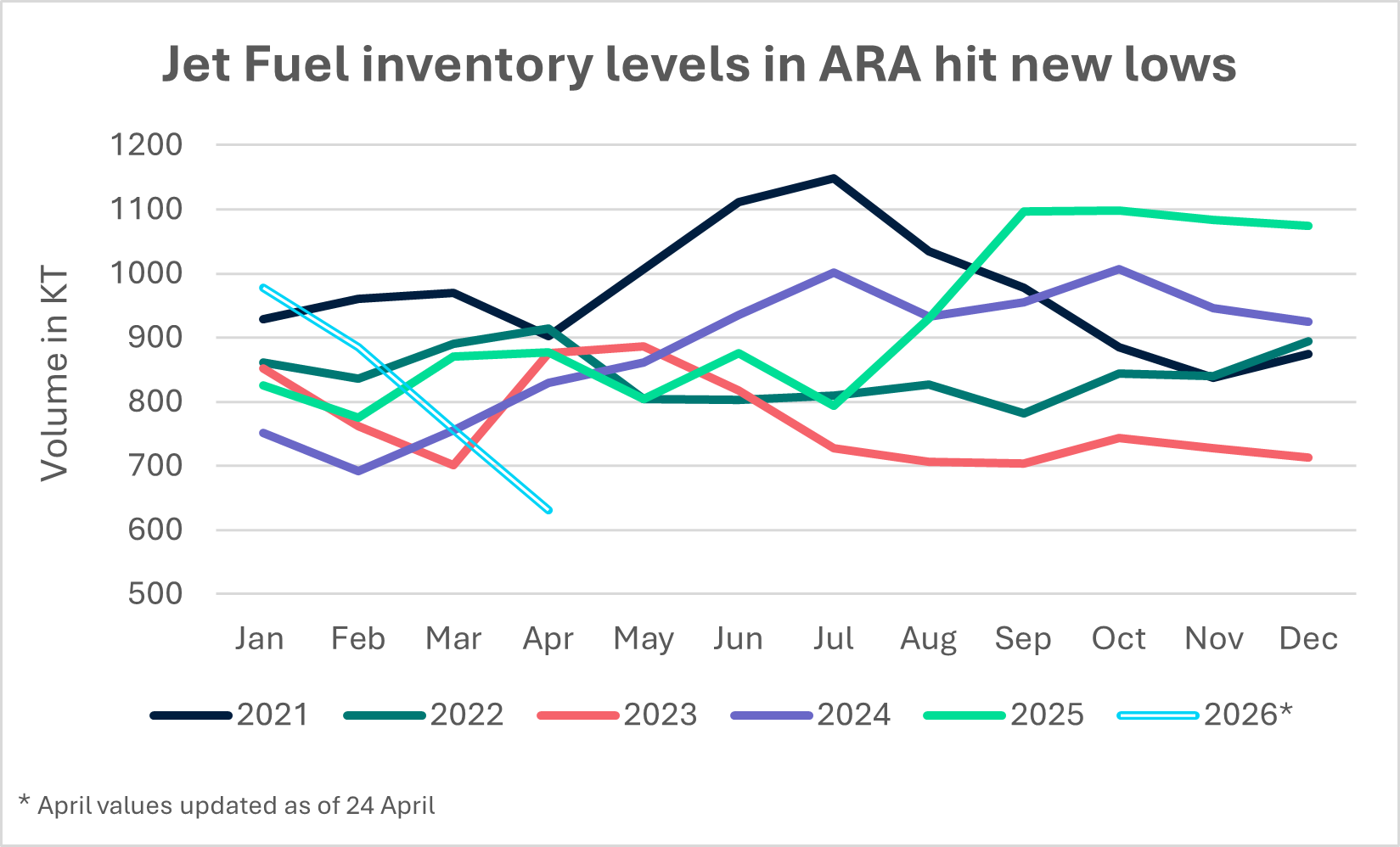

European jet fuel stocks at the major import-export Amsterdam-Rotterdam-Antwerp (ARA) hub have sunk to their lowest level since April 2020, according to Insights Global data, underscoring the speed of stock drawdowns as replacement flows struggle to keep pace.

The IEA has highlighted significant regional imbalances in jet fuel supply across Europe.

While some countries hold several months of stocks, major importers have less than 20 days of cover, with the UK — Europe’s largest jet fuel consumer and heavily import-dependent — particularly exposed due to tight inventories.

On the mainland, stocks appear sufficient for roughly 45–60 days, potentially extending supply through mid-May, but conditions are expected to tighten thereafter if flows do not normalise.

Arbitrage flows step up

Efforts to offset reduced Middle Eastern supply through arbitrage flows have intensified, supported by rising exports from the USA and Nigeria.

US jet fuel exports reached a record 442,000 barrels/day in early April, with four-week averages up 200,000 barrels/day above seasonal norms, according to US Energy Information Administration (EIA) data cited by the IEA.

Similarly, Nigeria’s jet fuel exports have increased to 66,000 barrels/day, according to market participants, although the ultimate allocation of these volumes remains unclear.

As Europe approaches the peak summer travel season, the market is increasingly dependent on attracting these additional cargoes from alternative regions. However, competition for barrels remains intense, particularly as Asian refiners — also reliant on Middle Eastern crude — face their own supply constraints.

Market dynamics suggest a bifurcated structure, with supply risks likely to re-emerge into mid-May as inventories draw down and uncertainty surrounding Middle East flows intensifies while current supply buffers begin to diminish.

Airlines rush to reduce consumption

On the demand side, early signs of adjustment are becoming more visible as airlines globally begin reducing capacity, particularly where fuel costs are unhedged or supply remains uncertain.

Germany-based airline group Lufthansa, for example, announced the permanent removal of 27 aircraft from its CityLine unit on 16 April, mostly MHIRJ CRJ models, as well as the retirement of its four-engined Airbus A340-600s. It will also ground some Boeing 747-400s from October 2026 ahead of the type’s retirement in 2027.

This in many ways mirrors the approach taken by airlines during the pandemic, when older, less efficient aircraft were pulled out of service first, enabling carriers to minimise their costs.

Lufthansa later went further, announcing on 21 April that it would drop 20,000 services over the summer with the ambition of saving around 40,000 tonnes of fuel. That’s despite its reassurances that it expects a “largely stable” fuel supply for the summer and is “pursuing a range of measures to this end”, such as hedging and physical purchases. It is however worth noting that for years, Lufthansa has complained about the difficulties of doing business in Germany and its desire to cut routes. Higher fuel prices could therefore present an ideal moment to do this.

Meanwhile, US major carrier United Airlines has revealed plans to cut capacity by 5% in the second and third quarters of 2026 to mitigate fuel bills that now account for over 20% of its operating expenses. Chief executive Scott Kirby has warned that elevated jet fuel prices could cost it $11 billion extra over the course of the year.

Yet United’s approach also highlights that — even in locations where shortages are not expected, such as the USA — it is the cost implications that are key. To that end, the carrier’s finance chief Michael Leskinen said during a 22 April results call that with the price of jet fuel rising “much more than the price of Brent”, he expected to see a “rationing function” in aviation as carriers pull back capacity. United alone spent $340 million more on fuel in the first quarter, which accounted for the vast bulk of a corresponding decline in profitability.

Specifically, airlines are prioritising cuts on routes where passenger demand is too weak to absorb higher fuel charges and where margins are so thin that the connections do not make sense.

KLM, operating in a market that is traditionally seen as price-sensitive, announced that it would operate 80 fewer flights in May 2026 to and from its Amsterdam Schiphol hub, specifically targeting high-frequency routes such as London and Dusseldorf where multiple daily flights can be consolidated.

Meanwhile, Australia’s Qantas reduced its planned fourth-quarter domestic capacity by 5 percentage points, redeploying those aircraft to high-yield international routes like Paris and Rome to maximise revenue.

Other, smaller players may see a more severe impact from surging fuel prices. Norse Atlantic, a low-cost long-haul carrier which launched amid the pandemic, and which crucially does not hedge its fuel, said on 15 April that it would restructure its operations and raise $110 million from shareholders in a bid to ride out elevated kerosene prices. Its stock price immediately halved on the news, with scant recovery since.

Unsurprisingly, the Middle East has been at the centre of capacity reductions globally. Air traffic manager Eurocontrol notes that in the week of 6-12 April, flows from Europe to the region were down 54% on last year, although overall capacity in Europe continued expanding as airlines ramped up into the peak season. The number of flights rose 2% week on week but remained slightly below 2025 levels, although this also reflected the impact of a pilot strike at Lufthansa.

A drop in the jet fuel ocean?

Despite such adjustments, there is a broad consensus among participants in the jet fuel market that demand-side responses have not yet reached the scale required to offset the structural supply shortfall.

Traders note that while reduced flight activity does lead to a marginal decline in jet fuel demand, the impact remains relatively limited in scale and timing.

Airline consumption tends to adjust gradually rather than abruptly, meaning demand-side softness has not been enough to materially rebalance the market.

At the same time, ongoing disruptions in supply chains, combined with particularly reduced or redirected refinery and trade flows, have removed a more significant volume of barrels from the system.

This imbalance between only modest demand erosion and more pronounced supply constraints has left overall fundamentals skewed tight, with the market continuing to rely heavily on constrained inventories and volatile import flows rather than meaningful demand relief.

This is despite the signals showing that strategic cuts to capacity are more than just a few isolated airlines marking cosmetic changes, but a global shift. Cirium data indicates that airline capacity for May 2026 has fallen by around 3 percentage points, with 19 of the world’s 20 largest airlines cutting flights. The longer the crisis goes on, the more cuts should be expected.

Gaps in the market

At the same time, some airlines are also spotting opportunities that could even increase their jet fuel use.

With the suitability of the Middle East as a transfer hub now called into question, European airline groups IAG, Air France-KLM, and Lufthansa Group have rapidly ramped up their direct services to Asia, often using equipment that would have been operated to the Gulf. India has proved particularly popular, with all three groups adding significant capacity to the country.

Speaking in March, Casten Spohr, Lufthansa Group’s chief executive, said that extra flights placed into Asian routes had been “filled within days” by customers that would have transferred through the Middle East. Over the longer term, he expects his airlines’ reputations as “pillars of stability” to serve as a tailwind, given that passengers tend to respond to geopolitical upheaval by choosing established brands flying to destinations perceived as low-risk. Given this, “we can certainly attract more customers and make more profits,” he said.

ICIS is a global provider of independent commodity intelligence for the chemicals and energy markets. Cirium is the world’s most trusted source of aviation analytics, providing data and analytics to the air transport industry. ICIS and Cirium are both part of LexisNexis® Risk Solutions, a RELX business.