Cirium Ascend Consultancy is trusted by clients across the aviation industry to provide accurate, timely, and insightful aircraft appraisals. The team provides the valuations and analysis the industry relies on to understand the market outlook, evaluate risks and identify opportunities.

Discover the team’s industry reports & market commentaries. Read their latest expert analysis, viewpoints and updates on Thought Cloud.

Team Perspective

Richard Evans, Senior Consultant, Cirium Ascend Consultancy

Three weeks ago, Cirium’s forward schedule data for April 2026 showed a 3.4% year-on-year growth in ASKs, compared to 5.4% immediately before the conflict started. For May 2026, planned capacity had fallen marginally, from 6.6% to 6.3%.

Since then, airlines have continued to adjust their near-term schedules, as a direct result of airspace and airport disruption in the Middle East, as well as due to the cost impact of a doubling in jet fuel prices. The latest schedule data now shows that April 2026 ASKs are down by 2.0% year-on-year, in-line with the March 2026 actual flown capacity. May 2026 capacity has now been cut by around three percentage points, to stand at 3.4% growth over May 2025.

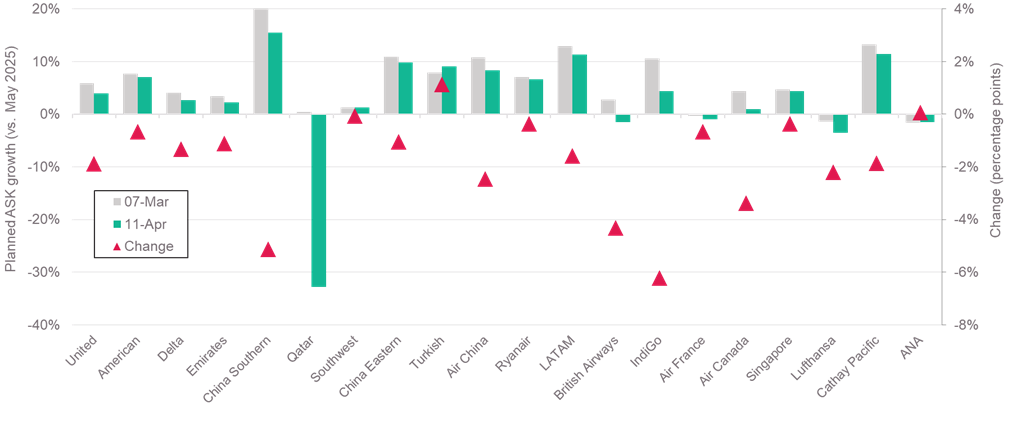

The chart below shows the latest May 2026 capacity plans of the 20 largest airlines, in terms of ASKs. With one exception, Turkish Airlines, all the airlines have cut their May schedule. Most have made reductions of 0-5 percentage points, consistent with the global change of 3%. There is a noticeable contrast between Qatar, with schedule now down 33% versus May 2025, and Emirates, who still plan a 2.4% year-on-year growth.

All regions have seen schedule cuts, with major airlines in North America, Europe and Asia Pacific reacting to a similar degree. The two purely short-haul carriers in this sample, Southwest and Ryanair appear to have been impacted less, making cuts of less than 1% at present.

It appears extremely likely that more reductions are ahead. Delta guided to flat year-on-year capacity in Q2 2026, against its current plan of 2.7% growth and Ryanair hinted it might trim schedules by 5-10% if jet fuel prices remain at their current levels.

Planned capacity for May 2026 – largest airlines

Source: Cirium schedules data, Cirium Ascend Consultancy analysis

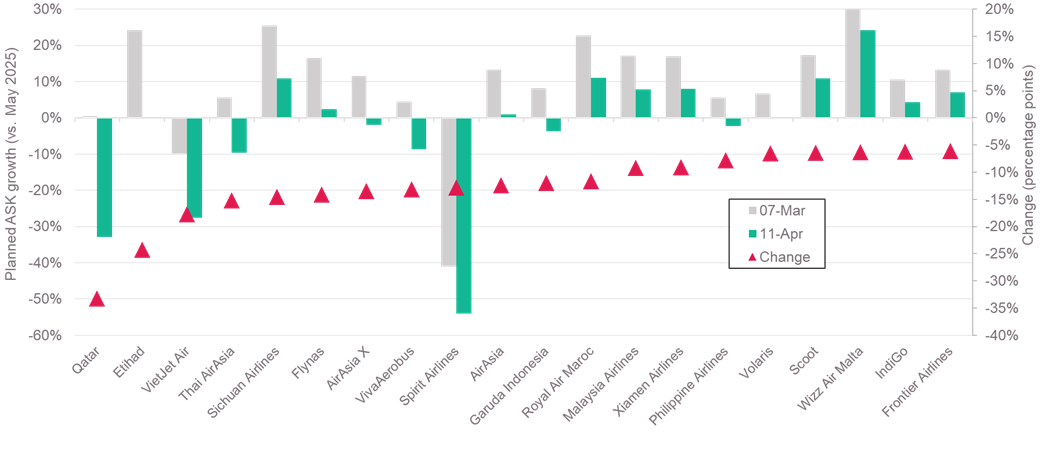

Turning to the 100 largest carriers, those with the biggest reductions in planned capacity unsurprisingly have several from the Middle East at the top of the list. However, there are airlines from a wide variety of countries represented in the data. Southeast Asian carriers appear to have been greatly impacted, consistent with media reports of fuel supply shortages in Vietnam and Philippines. Airlines from Malaysia and Indonesia have also cut planned schedules by around 10-15%. Some smaller Chinese airlines are also included, such as Sichuan Airlines and Xiamen Airlines.

Some of these airlines were planning on very large capacity expansions, and their latest schedules still imply year-on-year growth of 5% or more. Nevertheless, the list appears to show particular impact for some of the LCC carriers in Asia and the Americas.

Planned capacity for May 2026 – biggest schedule reductions

Source: Cirium schedules data, Cirium Ascend Consultancy analysis, Top 100 airlines by Jan 2025 ASKs

With the Iran conflict not fully resolved, it is clear that 2026 will experience a significant slowing of traffic and capacity, compared to Cirium Ascend Consultancy’s initial prediction of 4-6% growth over 2025. The impact will clearly be both deeper and more prolonged the longer the conflict continues and the longer jet fuel prices remain at their current levels, with second-order economic effects and risks increasing.

We have constructed some initial scenarios to estimate the global impact on the aviation market, which have been shared in more detail to our Commercial Aviation Monitor clients, and at industry events. These are based on modelling month-by-month capacity profiles for each airline domicile region, in the same way we considered the impact and recovery from Covid-19. The scenarios produce a range of outcomes, with 2026 global capacity change ranging from a decline of 2-3% to growth of 1-3%.

The more severe scenarios will require airlines to take additional action. Older, less fuel-efficient aircraft are the most likely to see utilisation cuts or parking. Airlines will seek to preserve cash in such circumstances, implying maintenance deferrals and fewer lease extensions. New aircraft deliveries appear less vulnerable, given the obvious fuel savings they deliver, but airframers themselves may face additional supply chain issues. Cirium will cover all these issues and more over the coming months.