Daniel Hall, Senior Valuation Consultant, Cirium Ascend Consultancy

This piece follows analysis shared within our 14 May 2025 market update webinar: available to watch on-demand.

Cirium Ascend Consultancy produces annual new delivery forecasts across the commercial, helicopter and business jet markets. In terms of new production, the helicopter and business sectors look to be entering growth mode once again, leaving supply chain woes behind us. For business jets, we believe some 8,700 new aircraft will be handed over in the following 10 years (2025-2034). This is driven by an 11% climb this year alone, driven by new types and product ramp-ups. The following analysis discusses this, and concludes with some thoughts on forecast risks.

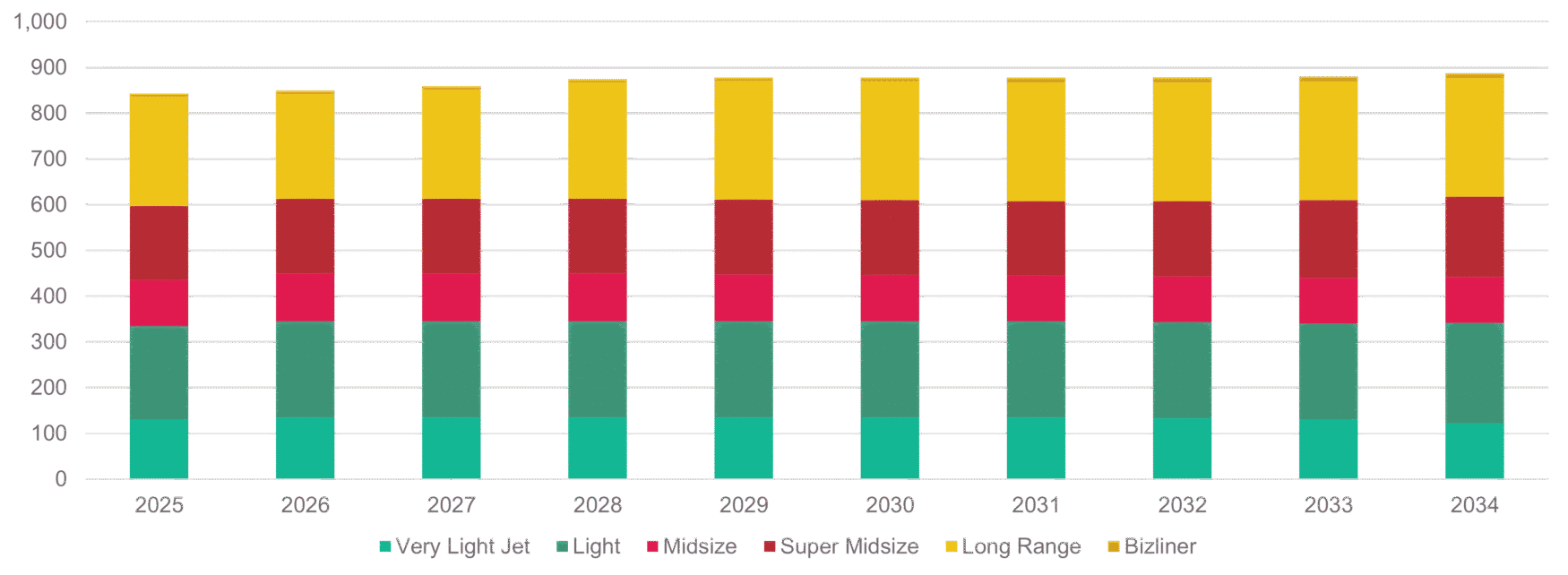

The below chart presents our annual forecast, split by market size segment/category.

Chart 1: Cirium Ascend Consultancy forecast: new business jet deliveries 2025-2034

Source: Cirium Ascend Consultancy forecast. Business turboprops not included.

Here are some key takeaways from our latest forecast.

Firstly, we expect new deliveries to increase by 11% this year. That is some growth, and we do admit that our forecast did not reach its target last year, owing to production strikes and a slow ramp-up of new products. But commentary from the OEMs suggests that supply chain issues are easing and with new product ramp-ups (such as Gulfstream’s G700 and Dassault’s Falcon 6X), and growth by Textron and Embraer, we feel confident that an 11% improvement will be achieved through 2025.

Secondly, following this growth year, we forecast a flattish annual growth of approximately 1% thereafter.

Comparing the next five years with the previous five translates to an overall 22% growth (equating to around 800 units), but almost half of this comes from the long-range category, which we forecast to grow deliveries by 31% alone.

The light sectors are showing notably little growth over recent history. Honda’s in-development Echelon programme is a slight unknown in terms of production and market demand, but we would not expect Textron (and Embraer) to easily concede market share or units to this.

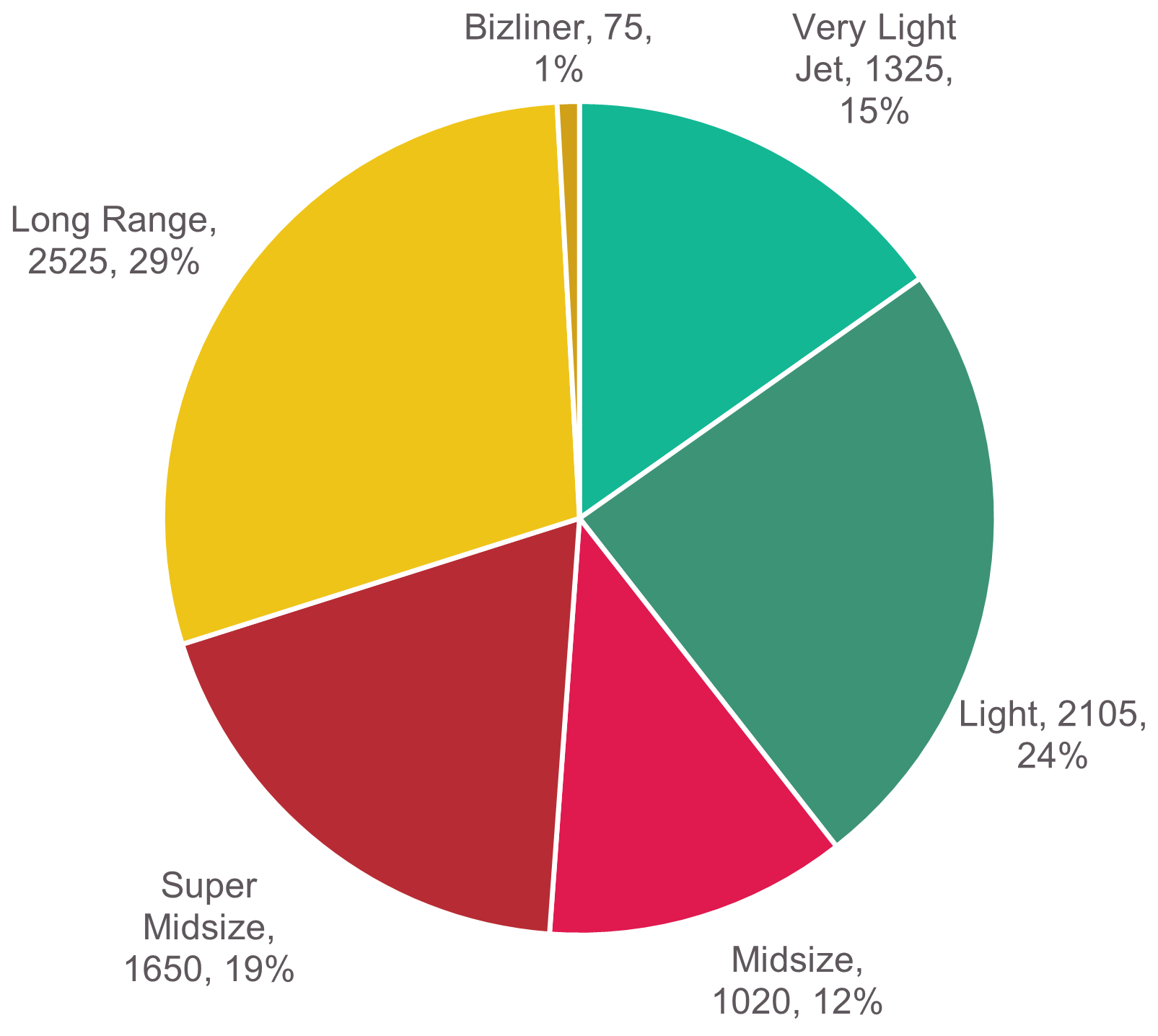

Not only is the long-range sector contributing to growth, but it also underpins our forecast by units (29%), and value, at a notable 63% share.

Chart 2: Forecast split by size sector: deliveries forecast by units and share

Source: Cirium Ascend Consultancy forecast. Business Turboprops not included.

Embraer is a growth OEM of note, and our forecast has this manufacturer moving into third position by units. Gulfstream and Dassault have notable product ramp-ups. Although the G650 will see production end this year, the Savannah-based OEM will be keen to get G700s out the door (which we forecast to be delivered at a rate of 3.5 for every G800 unit produced).

But overall, towards the end of the 10-year period, it is clear that to unlock more production, we need labour to ease and new innovative products to enter the scene. Over 15% of the forecast will be driven by new or to-be-launched types. Delays to their development may shift our forecast to the right.

The chart below adds our value of deliveries to the forecast. The impact of higher priced aircraft can clearly be seen in the large segment. Together, Gulfstream, Bombardier and Dassault alone are responsible for three-quarters of new delivery backlog value, in 2025 dollars at our Full-Life Base Values. Some $25 billion of business jet aircraft are expected to be delivered this year. That is quite a large financing need even in an industry where it is said that around half of new aircraft purchases are self-financed by cash.

Chart 3: Forecast split by size sector: deliveries forecast by value and share

Source: Cirium Ascend Consultancy forecast. Values are Full-Life Base Value. Business Turboprops not included.

An Industry Facing Plateau or Structural Change?

Why do we have lower forecast growth after 2025? We can look at the lack of new aircraft development after the Falcon 10X and Honda Echelon (both due in the 2027-2029 timeframe). We may have reached a development peak in terms of range, speed and cabin size, with current technology. Arguably a step change in new engine technology is needed to pivot the industry with something new. It could be said that with conventional technology, we may only see notable annual growth by other world regions taking more deliveries, particularly those underpinned by strong high net worth individual (HNWI) growth (e.g., India, China).

Backlogs are likely to stay fairly flat through this year. The major manufacturers are currently reporting book-to-bill ratios of around 1:1 (meaning one order for each delivery). This maintains them at around two years of backlog, which we think manufacturers prefer for planning purposes. Most OEMs seem hesitant to increase production rates; of course we know some are capable of more production (based on past performance), but local labour constraints may be holding them back. Perhaps a structural change is in play, backlogs will be maintained, and we won’t move back to the days of highly competitive pricing and “white tail” risk.

Forecast Risks, and 2025 So Far

As of late May 2025, Q1 2025 new deliveries are 15% up on Q1 2024, which is impressive growth and looks supportive of our forecast projection. This has been driven by a range of factors, some discussed above (e.g., general product ramp-ups), but also by built and undelivered aircraft last year (G700 & Falcon 6X). Of interest were comments by Embraer that they are working to balance their delivery stream across the full year rather than their historically heavy weighting in Q4.

There are risks, however. Tariffs have the ability to not only disrupt demand but also supply (of parts, raw materials). Many scenarios could play out, and the tariffs themselves are ever-changing. It may have been that a front-loading of deliveries helped a bump (before impacting an international transfer of an asset), but tariffs may later cause aircraft deferrals and we could see deliveries impacted in Q2 numbers.

During the webinar, we discussed the growth of the fractional operator segment. This has undoubtedly benefitted the forecast for popular types in that segment, for instance, the Phenom 300, Citation Latitude, Challenger 3500 and Praetor series. Any curtailment of growth could impact the demand/supply balance for those models, impacting Bombardier, Cessna and Embraer. But likewise, brand loyalty is typically strong and higher-hours fractional users who want to go into full ownership are likely to stick with the same product they are used to experiencing, representing an opportunity for these OEMs.

About Cirium Ascend Consultancy’s Business Jet Delivery Forecast

- Our independent new delivery forecast is our opinion on business jet deliveries for the upcoming 20 years, broken down by manufacturer, type and size segment. We also provide the value of deliveries forecast.

- The forecast can be bespoke, and go into greater levels of detail (including historical analysis, forecast methodology, commentary by size category/competitive landscape and OEM summary).

- While the forecast above is for business jets only, we can offer services in the business turboprop marketplace.

To request your copy of the Business Jet Delivery Forecast, enquire here.

Cirium Ascend Consultancy is available for expert advisory, aircraft, helicopter and engine valuations, as well as market commentaries across various asset classes. We have a team consisting of both ISTAT-certified and ASA-accredited appraisers spread across the globe with offices in North America, Europe and Asia. We are also able to provide ASA appraisals conforming to USPAP standards.