This recognition places the airline among a very small group of carriers that have demonstrated the ability to sustain world-leading operational performance over multiple years. Aeromexico’s achievement reflects an organization that has turned operational reliability into a meaningful and enduring strength.

While many airlines see natural swings in their performance from one year to the next, Aeromexico continues to show that consistency at the highest level requires more than intention. It demands investment in the right infrastructure, disciplined execution across thousands of daily operational moments, and leadership that makes operational performance a strategic priority even during periods of market pressure.

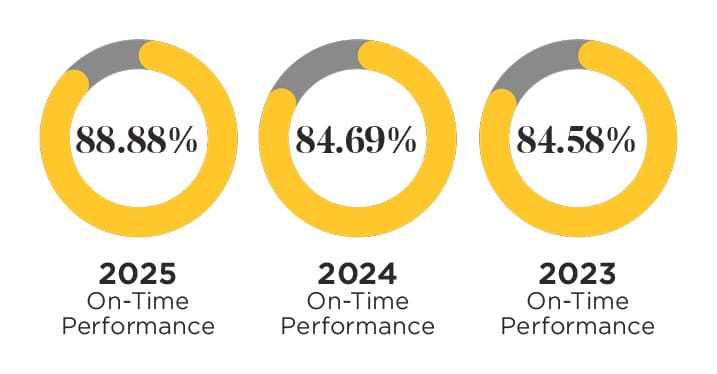

The airline entered 2025 building on its position as the world’s most on time global airline in 2024, when it delivered an 86.70% on time performance across nearly 197,000 flights. In 2025, Aeromexico has elevated its performance to 90.02 percent, with each month holding close to or above the 90% level and no extended periods of decline. February reached nearly 93% and the consistently strong results through the autumn months reinforce not a single award year but a pattern of sustained and repeatable operational excellence.

Strategic Resilience in a Challenging Year

Operational excellence was only one part of Aeromexico’s 2025 performance. The airline reported its second-best third quarter in history, generating $1.4 billion in revenue with a 31 percent adjusted EBITDA margin. These financial results were delivered despite significant external pressures, reinforcing the carrier’s premium positioning and disciplined network strategy.

A critical milestone came in November, when a federal appeals court granted a stay on the U.S. Department of Transportation’s order to unwind the Aeromexico–Delta Joint Venture. The decision preserved seamless connectivity for millions of passengers and protected strategic revenue flows that support the airline’s long-term network plans.

Building Tomorrow’s Network

Aeromexico also signaled confidence in future demand with its recent expansion announcements. The new Mexico City–Barcelona service, operating six times weekly, and the first-ever Monterrey–Paris route represent thoughtfully chosen additions to the transatlantic network. These routes are supported by codeshare partnerships, including the strengthened SkyTeam connection with SAS, which broadens one-stop access between Mexico and Scandinavia.

The significance of these decisions lies in their timing. Expanding long-haul international operations while also sustaining industry-leading on-time performance is uncommon. Executing both simultaneously suggests a mature operational foundation and measured resource planning.

Leadership That Delivers

Aeromexico also signaled confidence in future demand with its recent expansion announcements. The new Mexico City–Barcelona service, operating six times weekly, and the first-ever Monterrey–Paris route represent thoughtfully chosen additions to the transatlantic network. These routes are supported by codeshare partnerships, including the strengthened SkyTeam connection with SAS, which broadens one-stop access between Mexico and Scandinavia.

Under the strategic direction of CEO Andrés Conesa and the operational leadership of COO Santiago Diago, Aeromexico has built a culture where reliability is embedded across the organization. Front-line teams, operational planners, and leaders have worked together to create a system built on coordination, accountability, and continuous improvement.

Sustaining an on-time performance level above 85% across domestic, regional, and long-haul international operations is challenging. Achieving it across an entire year reflects an organization with strong processes, clear priorities, and a disciplined approach to service delivery.

Cirium congratulates the entire Aeromexico team on earning back-to-back Global On-Time Performance titles. The achievement highlights a commitment to operational excellence that benefits passengers, strengthens competitiveness, and sets a standard for the global airline industry.

Lydia Webb, Marketing Director – Americas & Strategic Programs, Cirium

In 2024, Virgin Atlantic reported an OTP of 74.02% and did not qualify for the top 20 ranking in the Europe region based on total flight volume. However, this year, the airline not only met the qualifications but also secured the #4 position in the region with an impressive 83.45% OTP across 26,359 flights; a 9.43 percentage points gain over last year. This accomplishment extends beyond the European context, positioning Virgin Atlantic among the leading airlines globally. It further highlights the organization’s commitment to overcoming challenges and continuously improving its operational standards.

Virgin Atlantic consistently mainted high on-time performance scores throughout 2025, registering OTPs above 80% – except January and December. The airline is committed to being a challenger and a leader in its field and have made significant investments in fleet modernization, premium experience for guests, its people, and the communities it serves.

A Year for Change

In 2025, Virgin Atlantic focused on improving its on-time performance and underwent major developments across the business. The airline formed new interline and codeshare agreement with Caribbean Airlines, expanded its network and also joined a strategic partnership with IndiGo, Delta Air Lines, and Air France-KLM to link India’s expanding economy with North America and Europe.

The airline also announced a partnership with Joby Aviation, to provide zero-emission, short-range trips between Virgin Atlantic’s hubs at Heathrow and Manchester Airport and other regional destinations.

To complete its fleet modernization initiative, Virgin Atlantic Airways secured $745 million in financing from Apollo-managed funds, leveraging its London Heathrow slots. The funds will strengthen the airline’s finances and support upgrades, including Boeing 787-9 refurbishments, new Airbus A330neo aircraft with expanded premium cabins and Retreat Suites from 2026, and fleet-wide Starlink-powered Wi-Fi. Virgin Atlantic will be the first UK airline to introduce free, streaming-quality, unlimited Wi-Fi throughout its fleet, using Starlink technology, with rollout completing in 2027.

Leading Into The Future

Virgin Atlantic’s Board has announced that Shai Weiss will step down as CEO at the end of 2025, and Corneel Koster will take over the position. Koster, who was formerly Chief Customer and Operating Officer, played a key role in overseeing operations, enhancing customer experience, guiding the airline through the pandemic, introducing the A330neo aircraft, and advancing digital transformation initiatives. Under Koster’s leadership, the airline aims to keep its commitments and achieve new standards in operational performance.

A Job Well Done

In today’s highly competitive airline industry, maintaining an on-time performance above 80% for domestic, regional, and long-haul flights is no easy task—especially if the starting point falls short of that benchmark. Virgin Atlantic has demonstrated through its accomplishments why it stands out as both a challenger and an industry leader. The airline’s dedication to improvement has not gone unnoticed. Cirium extends its congratulations to the entire Virgin Atlantic team for earning the title of Most-Improved Airline of the year—a recognition that is truly well earned. We look forward to seeing even greater achievements in the future.

In 2025, Iberia Express achieved an outstanding arrival OTP of 88.94 % across 37,119 total flights operated, a testament to its unwavering commitment to operational excellence and customer trust.

This year’s recognition is particularly significant given the challenging landscape for European aviation. Iberia Express’s performance stands out against a backdrop of notable disruptions, including a major power outage that affected air travel across the Iberian Peninsula and a global software issue impacting the Airbus A320 family—aircraft that comprise the entirety of the airline’s fleet. These events led to widespread delays and operational constraints for carriers throughout the region.

Despite these headwinds, Iberia Express maintained its hallmark punctuality. The airline’s ability to deliver reliable operations in the face of disruption reflects a strong foundation of effective planning, robust processes, and a commitment to high standards throughout its organization. Madrid-Barajas Adolfo Suárez Airport, serving as the airline’s strategic hub, plays a central role in supporting operational continuity, while close collaboration within the Iberia Group and IAG provided additional resilience and flexibility during challenging periods.

The commitment and expertise of Iberia Express’s operational teams have been instrumental in sustaining exceptional performance. From flight crews to ground staff, there can be no doubt that the dedication and professionalism of their employees have contributed to the airline’s ability to sustain high performance standards over multiple years, helping ensure passengers can rely on timely arrivals and departures even during periods of disruption.

So, as Iberia Express celebrates its third consecutive European OTP crown, it stands as a symbol of Spanish reliability and innovation. The airline’s achievements not only reflect its own strengths but also raise the bar for the entire industry. Congratulations to the Iberia Express team for their continued leadership in punctuality and for delivering exceptional value to travellers year after year.

Lydia Webb, Marketing Director – Americas & Strategic Programs, Cirium

It is a foundational element that directly influences an airline’s brand reputation, operational stability, and financial health. As the industry becomes increasingly competitive, the strategic value of maintaining high OTP has never been more significant.

For airlines, excelling in on-time performance creates a ripple effect of positive outcomes. It strengthens passenger loyalty, streamlines complex operations, provides a distinct competitive edge, and generates substantial cost savings.

Improved Passenger Loyalty and Satisfaction

The modern traveler expects reliability, and a consistent record of on-time arrivals and departures allows airlines to meet this expectation effectively. This foundation of trust directly contributes to increased customer loyalty. When passengers can rely on an airline to deliver them to their destinations as scheduled, their overall travel experience is enhanced. Each timely flight reinforces the airline’s commitment to dependable service, which is essential for establishing and retaining passenger trust. Punctuality holds particular significance for business travelers, enabling them to plan meetings and commitments with assurance. Leisure travelers also benefit from reduced stress and uncertainty associated with reliable service. Over time, such operational consistency cultivates a loyal customer base that is more likely to choose the airline in the future and endorse it to others.

Enhanced Global Brand Recognition

A strong record of on-time performance serves as an effective marketing advantage for airlines. Consistently high OTP rankings attract favorable media coverage and help build a dependable reputation, influencing how both customers and industry partners view the airline worldwide. When a brand is recognized for its punctuality, it is often seen as professional, well-organized, and attentive to customer needs, making it stand out in a competitive market. Maintaining excellent OTP not only develops a positive brand image but also signals a commitment to high standards and respect for passengers’ time. This reputation may be the deciding factor for travelers choosing between flights with similar prices. An airline known for its timeliness also tends to be associated with high quality across other elements of service, such as safety and customer support, ultimately strengthening its brand and market position.

Driving Operational Efficiency

On-time performance isn’t just about how customers view an airline—it reflects the overall efficiency of its operations. When every part of the system, from ground staff to scheduling, runs smoothly together, high punctuality is achieved. Prioritizing on-time departures and arrivals pushes airlines to refine their processes, making everything work better. Because airline networks are so interconnected, even one delay can cause problems across many flights and connections.

Optimized Aircraft Utilization and Crew Scheduling

Aircraft are among an airline’s most valuable assets, and maximizing their use is essential for profitability. Punctuality ensures that planes adhere to their intended schedules, minimizing costly time on the ground and allowing for tighter turnarounds. This optimization allows carriers to fly more segments per day with the same number of aircraft.

Similarly, on-time operations lead to more stable and predictable crew schedules. Delays can cause a cascade of crewing issues, violating mandatory rest periods and requiring last-minute substitutions. By minimizing disruptions, airlines can improve crew quality of life, reduce sick leave, and avoid the operational complexities associated with re-assigning flight crews.

Gaining a Competitive Advantage

In an industry where ticket prices and in-flight amenities are often comparable, on-time performance has emerged as a key differentiator. Airlines that outperform their rivals in this metric can leverage it to attract and retain customers, ultimately increasing their market share. On-time performance data is publicly available and widely reported, allowing for direct comparison and benchmarking among competitors. Airlines use this data to gauge their own performance against the industry and identify areas for improvement. Consistently ranking at the top of these leaderboards provides tangible proof of operational excellence, which can be highlighted in marketing campaigns to attract discerning travelers.

Realizing Significant Cost Savings

High on-time performance brings significant financial advantages. Although it takes investment in both technology and process improvements to achieve punctuality, the savings from fewer delays often far exceed these upfront costs. Flight delays are costly—extra time spent taxiing or waiting in holding patterns consumes more fuel. Sticking to schedules helps airlines cut down on this unnecessary fuel use. Operating efficiently also lowers overtime costs for ground crews, gate agents, and other staff who must stay late when flights run behind. When flights are on time, resource management becomes smoother and more cost effective. Another major expense of delays is compensating passengers; airlines might have to offer meal vouchers, hotel stays, or even cash depending on how long people are kept waiting and what regulations apply. Delays can also mean extra work for agents rebooking travelers stranded by missed connections. By keeping flights running on time, airlines can substantially lower these expenses, safeguard their revenue, and reduce negative customer service incidents linked with disruptions.

The strategic importance of on-time performance in the aviation industry cannot be overstated.

It is a critical metric that influences nearly every aspect of an airline’s business, from the passenger experience to financial results. By delivering reliable, punctual service, airlines can foster deep-seated customer loyalty and enhance their global brand reputation.

In a landscape defined by tight margins and high customer expectations, on-time performance is not just a goal—it is a fundamental component of a successful and sustainable aviation strategy.

The Platinum recognition goes to one carrier annually based on a proprietary algorithm that weighs reliability, operational precision, disruption recovery, and performance at scale. The question is straightforward: which airline demonstrates the strongest operational control and consistency when you look at the complete picture.

The Performance Case

Qatar Airways delivered 84.42 percent on-time performance in 2025 under Cirium’s methodology, up from 82.83 percent in 2024 across roughly 198,303 flights.

That improvement matters because it came on top of an already strong base while maintaining completion factor close to 100 percent. Improving OTP when you’re already in the low 80s is harder than moving from the 70s—there’s less margin for gains, and the operational discipline required is tighter.

The scale context makes the numbers more meaningful. Qatar operates a tightly banked hub at Hamad International Airport serving over 170 destinations, running long haul and multistop journeys across multiple regions and time zones. Each connection bank multiplies operational risk because aircraft positioning, crew availability, passenger flows, and ground services all must align repeatedly throughout the day. Keeping delays and cancellations low in that environment requires precision that most network carriers struggle to maintain.

What Qatar Actually Did

The execution comes down to realistic planning and disciplined operations control. Qatar built turn times and connection windows that work in practice, not just on paper. When disruptions hit in 2025, including airspace constraints from geopolitical issues, weather volatility, and aircraft availability problems, the carrier protected key connection flows and used operational data to retime and reroute during irregular operations.

That approach kept cancellations low and gave passengers a higher probability of completing their journey as booked, even on difficult days. The completion factor numbers confirm this wasn’t theoretical; Qatar got passengers where they needed to go.

The A30 numbers tell the recovery story more clearly. Qatar Airways maintains one of the lowest A30 rates among global network carriers which means very few flights arrive more than 30 minutes late. That metric reveals operational discipline that goes beyond preventing delays; it’s about containing them when they occur. In a banked hub operation where one delay can cascade through multiple connections, keeping severe delays low requires tight control over recovery decisions such as aircraft swaps, crew repositioning, passenger reprotection, and ground coordination. Qatar’s A30 performance indicates they’re making those decisions well under pressure, consistently.

The operational focus appears to be a deliberate priority backed by investment in schedule planning, day of operations control, and analytics capabilities. You can see it in how Hamad International’s operations coordinate with the airline’s schedule, and the hub has grown over the past few years without the reliability of degradation that typically comes with expansion.

What This Signals

Looking at 2025’s operational data across global carriers, Qatar’s performance demonstrates that a large, complex network can still be run with discipline and predictability in a volatile environment. That’s not a given anymore. Many network carriers have accepted that operational variability is simply the cost of scale and complexity.

Qatar’s numbers suggest otherwise. The combination of high OTP, near-perfect completion, and performance improvement year over year at this scale indicates that operational control remains achievable when it’s treated as non-negotiable rather than a metric to track.

For the industry, that’s the real takeaway. Network complexity and operational volatility are facts, but they don’t have to determine outcomes. Qatar Airways proved that in 2025.

Cirium Ascend Consultancy is trusted by clients across the aviation industry to provide accurate, timely, and insightful aircraft appraisals. The team provides the valuations and analysis the industry relies on to understand the market outlook, evaluate risks and identify opportunities.

Max Kingsley-Jones, Head of Advisory, Cirium Ascend Consultancy

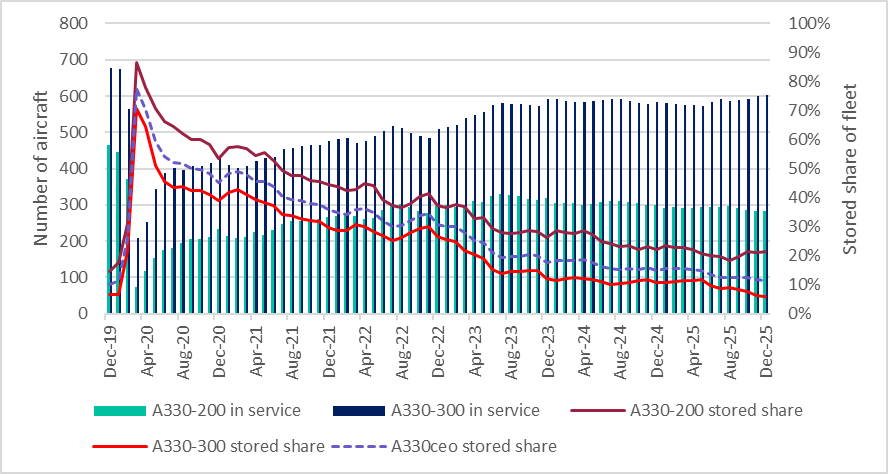

The Airbus A330ceo’s recovery momentum has continued through 2025, with the -200/300 combined in-service passenger fleet now at 88% of the total inventory. Meanwhile, the number of A330 freighters in service – including both converted aircraft and factory freighters – is close to passing the 100-aircraft mark.

The A330-300 recovery has fared particularly well, with the in-service passenger fleet having just nudged above 600 units, according to Cirium data (chart 1). This the highest it has been since the Covid crisis began and just 10% below the 680 aircraft in-service tally back in late 2019.

Just 6% of the passenger -300 fleet remains stored, compared with 21% of the -200’s, which is not enjoying the same strength of recovery as its bigger sister. The in-service -200 passenger fleet is now at around 280 aircraft, having peaked at 330 in mid-2023. The current -200 operating fleet is two-fifths behind its pre-Covid level of 460 aircraft.

Chart 1: A330 passenger fleet recovery trend

Source: Cirium Fleets Analyzer

The ongoing deficit of passenger widebodies has been driving the recovery of the passenger A330ceo market, bolstering Market Values and Lease Rates over the last couple of years. Most recently, Cirium increased Market Values for both the A330-200 and the -300 High Gross Weight variants in September 2025 by 12% on a fleet-weighted average basis.

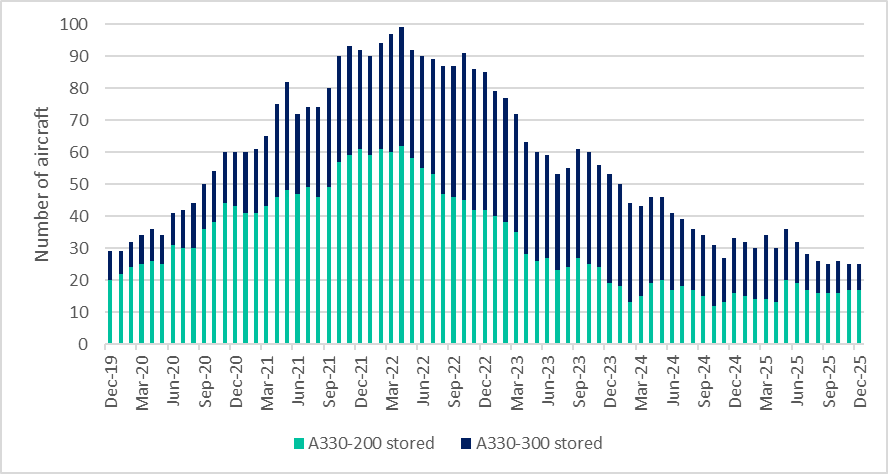

The -200/300’s combined storage inventory (115 aircraft) is now less than 12% of the passenger A330ceo’s total fleet. The 26% decline in the stored inventory through 2025 (from 155 aircraft) has been driven by several factors, including: aircraft being returned to passenger service; being converted to freighters or being parted out. Cirium has so far recorded a total of 25 A330ceo passenger retirements for 2025, including 16 -200s and nine -300s.

The number of stored passenger A330ceos managed by lessors has declined by 25% over last 12 months and now stands at just 25 aircraft (chart 2). This total includes 17 A330-200s and only eight -300s. The lessor-stored tally had peaked in Q2 2022 at around 100 aircraft, and the inventory decline is another good measure of the current health of the A330 market.

On the cargo front, Cirium data shows that the A330 full-freighter fleet has risen by a fifth over the last 12 months to 97 aircraft, including 38 -200 factory freighters and 59 EFW-converted aircraft (21 -200P2Fs and 38 -300P2Fs). Cirium recorded 13 A330 freighter conversions in 2025 and shows at least 11 more scheduled in 2026, including the first of up to 30 -300BDSFs by Israel Aerospace Industries for lessor Avolon.

Probably the biggest issue that the A330 conversion market faces is the lack of feedstock due to the strength of demand for passenger aircraft. Given Airbus and Boeing look set to face continuing issues for the next 2-3 years at least in achieving significant increases in widebody deliveries, it’s hard to see any near-term softening of the A330 passenger market – barring of course any unforeseen external factors.

LONDON (Jan. 2, 2026) – Aeromexico maintained a 90.02% on-time performance to claim the world’s most on-time global airline title for the second consecutive year, according to Cirium’s 2025 On-Time Performance Review released today.

The Mexican carrier becomes only the second airline to achieve consecutive global wins since Cirium launched the program in 2009, operating 188,859 flights across 23 countries while maintaining industry-leading schedule reliability.

Aeromexico Holds Global Lead; Regional Champions Crowned

Aeromexico secured the global airline title with 90.02% on-time performance, holding off strong competition from Saudia in second place with 86.53% and SAS with 86.09% in third. The margin between first and third place was 3.93 percentage points, reflecting rising operational standards across the industry.

Regional winners included:

North America: Delta Air Lines won for the fifth consecutive year with 80.90% on-time performance

Europe: Iberia Express (International Airlines Group) defended its title for the third consecutive year with 88.94% performance

Asia-Pacific: Philippine Airlines claimed the regional title for the first time with 83.12% on-time performance

Latin America: Copa Airlines achieved its 11th win, the most of any airline since Cirium’s program launched in 2009 with 90.75% on-time performance

Middle East and Africa: Safair topped the regional rankings with 91.06% on-time performance

Qatar Airways Wins Airline Platinum Award

Qatar Airways captured Cirium’s Platinum Award, recognizing the Doha-based carrier’s operational excellence across its global hub network. The airline achieved 84.42% on-time performance across more than 198,303 flights spanning six continents.

Virgin Atlantic Claims Inaugural ‘Most Improved’ Award

Virgin Atlantic won Cirium’s new ‘Most Improved’ award, demonstrating the largest year-over-year operational performance gain among global carriers. The UK-based airline improved its on-time performance from 74.02% in 2024 to 83.45% in 2025—a 9.44 percentage point increase year-over-year.

The new award recognizes airlines that have achieved meaningful operational scale (minimum 70% baseline performance) while delivering substantial improvements, ensuring the honor reflects genuine operational excellence, rather than recovery from poor prior performance.

Istanbul Airport won Cirium’s Airport Platinum Award, which evaluates operational complexity, passenger impact during disruptions, and growth trajectory. Last year’s Airport Platinum winner was El Dorado International Airport in Bogotá, Colombia.

Industry Context and Analysis

Jeremy Bowen, Cirium CEO, said: “Maintaining consistent on-time performance requires sophisticated network planning, operational coordination, and the ability to recover quickly when irregularities occur. These results reflect the operational discipline that defines aviation’s top performers.”

“Qatar Airways’ Platinum win is particularly significant because it demonstrates how a network carrier can maintain on-time performance across six continents while operating one of the industry’s most complex hub structures. Their 84.42% on-time rate over 198,303 flights sets a new benchmark for network carriers. Similarly, Copa’s 11th win for the Latin American category and Delta’s fifth consecutive North American win reflects sustained operational focus that separates industry leaders from competitors.”

About the On-Time Performance Review

Now in its 17th year, the Cirium On-Time Performance Review analyzes flight data from over 600 real-time sources including airlines, airports, global distribution systems, and civil aviation authorities. An independent advisory board of aviation industry veterans provides oversight and guidance.

An on-time flight arrives within 14:59 minutes of scheduled gate arrival time. Airport punctuality measures flights departing within 14:59 minutes of scheduled departure time. The Platinum Awards for both airlines and airports consider operational complexity, network scale, passenger impact during disruptions, and consistency throughout the year.

The Most Improved award, introduced in 2025, requires carriers to demonstrate at least 70% baseline on-time performance in the prior year to ensure recognition reflects operational excellence rather than recovery from poor performance.

Complete 2025 Rankings

Top 10 Global Airlines

Ranking

Airline

On-Time Arrivals

Total Flights

1

(AM) Aeromexico

90.02%

188,859

2

(SV) Saudia

86.53%

202,864

3

(SK) SAS

86.09%

249,674

4

(AD) Azul

85.18%

304,625

5

(QR) Qatar Airways

84.42%

198,303

6

(IB) Iberia

83.52%

188,447

7

(LA) LATAM Airlines

82.40%

580,707

8

(AV) Avianca

81.73%

266,921

9

(TK) Turkish Airlines

81.41%

421,087

10

(DL) Delta Air Lines

80.90%

1,800,086

Top 10 North American Airlines

Ranking

Airline

On-Time Arrivals

Total Flights

1

(DL) Delta Air Lines

80.90%

1,800,086

2

(AS) Alaska Airlines

79.20%

453,031

3

(NK) Spirit Airlines

78.83%

218,265

4

(UA) United Airlines

78.77%

1,732,450

5

(WN) Southwest Airlines

77.04%

1,422,405

6

(AA) American Airlines

76.43%

2,259,576

7

(B6) JetBlue

74.66%

313,318

8

(WS) WestJet

73.58%

205,501

9

(AC) Air Canada

73.26%

383,819

10

(F9) Frontier Airlines

72.14%

208,987

Top 10 European Airlines

Ranking

Airline

On-Time Arrivals

Total Flights

1

(I2) Iberia Express

88.94%

37,119

2

(SK) SAS

86.09%

249,674

3

(OS) Austrian

83.74%

124,457

4

(IB) Iberia

83.52%

188,447

5

(VS) Virgin Atlantic

83.45%

26,359

6

(FI) Icelandair

83.23%

39,425

7

(VY) Vueling

82.20%

228,611

8

(TK) Turkish Airlines

81.41%

421,090

9

(D8, DY) Norwegian

80.96%

150,784

10

(AY) Finnair

79.67%

116,652

Top 9 Latin American Airlines

Ranking

Airline

On-Time Arrivals

Total Flights

1

(CM) Copa Airlines

90.75%

133,748

2

(AM) Aeromexico

90.02%

188,859

3

(G3) Gol

87.75%

238,182

4

(AD) Azul

85.18%

304,625

5

(LA) LATAM Airlines

82.40%

580,707

6

(H2) Sky Airline

82.39%

55,116

7

(AV) Avianca

81.73%

266,921

8

(JA) JetSmart Chile

76.91%

90,460

9

(AR) Aerolineas Argentinas

76.54%

107,490

Only 9 airlines qualified in the region

Top 10 Asia-Pacific Airlines

Ranking

Airline

On-Time Arrivals

Total Flights

1

(PR) Philippine Airlines

83.12%

116,268

2

(NZ) Air New Zealand

79.29%

171,216

3

(NH) ANA

78.88%

309,998

4

(SQ) Singapore Airlines

78.58%

121,293

5

(JL) JAL

78.25%

313,410

6

(6E) IndiGo

78.12%

802,418

7

(CX) Cathay Pacific

76.78%

119,193

8

(VA) Virgin Australia

76.54%

155,038

9

(QF) Qantas

76.51%

276,859

10

(KE) Korean Air

75.34%

133,252

Top 10 Middle East and Africa Airlines

Ranking

Airline

On-Time Arrivals

Total Flights

1

(FA) Safair

91.06%

62,805

2

(RJ) Royal Jordanian

90.73%

37,524

3

(F3) Flyadeal

86.54%

69,971

4

(SV) Saudia

86.53%

202,864

5

(4Z) Airlink

84.47%

84,361

6

(QR) Qatar Airways

84.42%

198,303

7

(WY) Oman Air

83.10%

38,828

8

(SA) South African Airways

81.26%

24,461

9

(EY) Etihad Airways

81.06%

100,620

10

(KU) Kuwait Airways

79.50%

29,977

Top 10 Large Airports

Ranking

Airport

On-Time Departures

Total Flights

1

(SCL) Santiago Arturo Merino Benitez Intl Airport

87.04%

153,326

2

(RUH) Riyadh King Khalid International Airport

86.81%

264,614

3

(MEX) Mexico City Benito Juarez International Airport

86.55%

295,737

4

(HNL) Honolulu International Airport

86.51%

156,139

5

(OSL) Oslo Gardermoen Airport

86.00%

204,882

6

(LIM) Lima Jorge Chavez International Airport

85.54%

183,137

7

(SLC) Salt Lake City International Airport

85.04%

243,848

8

(CPH) Copenhagen Airport

84.72%

236,903

9

(DOH) Doha Hamad International Airport

84.70%

251,864

10

(ARN) Stockholm Arlanda Airport

83.59%

181,238

Top 10 Medium Airports

Ranking

Airport

On-Time Departures

Total Flights

1

(PTY) Panama City Tocumen International Airport

93.34%

148,065

2

(BSB) Brasilia International Airport

88.36%

114,481

3

(JNB) Johannesburg O.R. Tambo International Airport

86.22%

189,542

4

(ITM) Osaka Itami International Airport

86.04%

136,489

5

(DMM) Dammam King Fahd International Airport

85.15%

94,768

6

(GIG) Rio de Janeiro Galeao International Airport

85.13%

115,384

7

(PDX) Portland International Airport

85.02%

159,964

8

(VCP) Viracopos-Campinas International Airport

84.55%

111,758

9

(SJC) San Jose Mineta International Airport

83.66%

99,182

10

(CNF) Belo Horizonte International Airport

83.57%

113,857

Top 10 Small Airports

Ranking

Airport

On Time Departures

Total Flights

1

(GYE) Guayaquil Jose Joaquin de Olmedo Intl Airport

91.47%

34,068

2

(SAL) El Salvador International Airport

90.28%

47,203

3

(SDU) Rio de Janeiro Santos Dumont Airport

89.67%

58,303

4

(SVG) Stavanger Airport

89.55%

38,894

5

(UIO) Quito Mariscal Sucre International Airport

89.45%

42,911

6

(CPT) Cape Town International Airport

88.72%

82,030

7

(KOA) Ellison Onizuka Kona Intl Airport at Keahole

Notes to editors *An on-time flight is defined as a flight that arrives within 15 minutes of the scheduled gate arrival. For an airport, it is defined as departing within 15 minutes of its scheduled departure.

About Cirium Cirium® is the world’s most trusted source of aviation analytics. The company delivers powerful data and cutting-edge analytics to empower a wide spectrum of industry players. It equips airlines, airports, travel enterprises, aircraft manufacturers, and financial entities with the clarity and intelligence they need to optimize their operations, make informed decisions, and accelerate revenue growth.

Cirium® is part of LexisNexis® Risk Solutions, a RELX business, which provides information-based analytics and decision tools for professional and business customers. The shares of RELX PLC are traded on the London, Amsterdam and New York Stock Exchanges using the following ticker symbols: London: REL; Amsterdam: REN; New York: RELX.

After a period of significant disruption, global travel demand has not only returned but is also setting a new trajectory. Growth is now driven by resilient structural demand, evolving passenger expectations, and ongoing supply-side pressures. For operators, the imperative is clear: data-driven strategies are essential to achieve operational efficiency, enhance future readiness, and improve the passenger journey in a rapidly shifting market.

The Cirium webinar, Future Flight: Shaping Traveler Experiences with Aviation Analytics, explored forces shaping commercial aviation as the industry approaches 2026. Drawing on insights from panelists representing various aviation sectors and the latest aviation data, the session covered the global demand outlook, operational responses to emerging pressures, and the expanding role of aviation analytics in strengthening airport resilience and enhancing the passenger experience.

The global travel outlook: a new trajectory

The outlook for global air travel has shifted as the industry moves beyond pandemic recovery. Global revenue passenger-kilometers (RPKs) have surpassed 2019 levels, reflecting strong demand. However, the industry still trails its pre-covid growth trajectory, representing about four years of lost progress.

The rapid growth seen after borders reopened has eased, and demand is being driven by fundamental market forces than by deferred travel. In this climate, commercial aviation is forging a distinctly new path.

An uneven recovery landscape

Joanna Lu from Cirium Ascend Consultancy presented 2026 Travel Market: Robust demand in a constrained operating environment

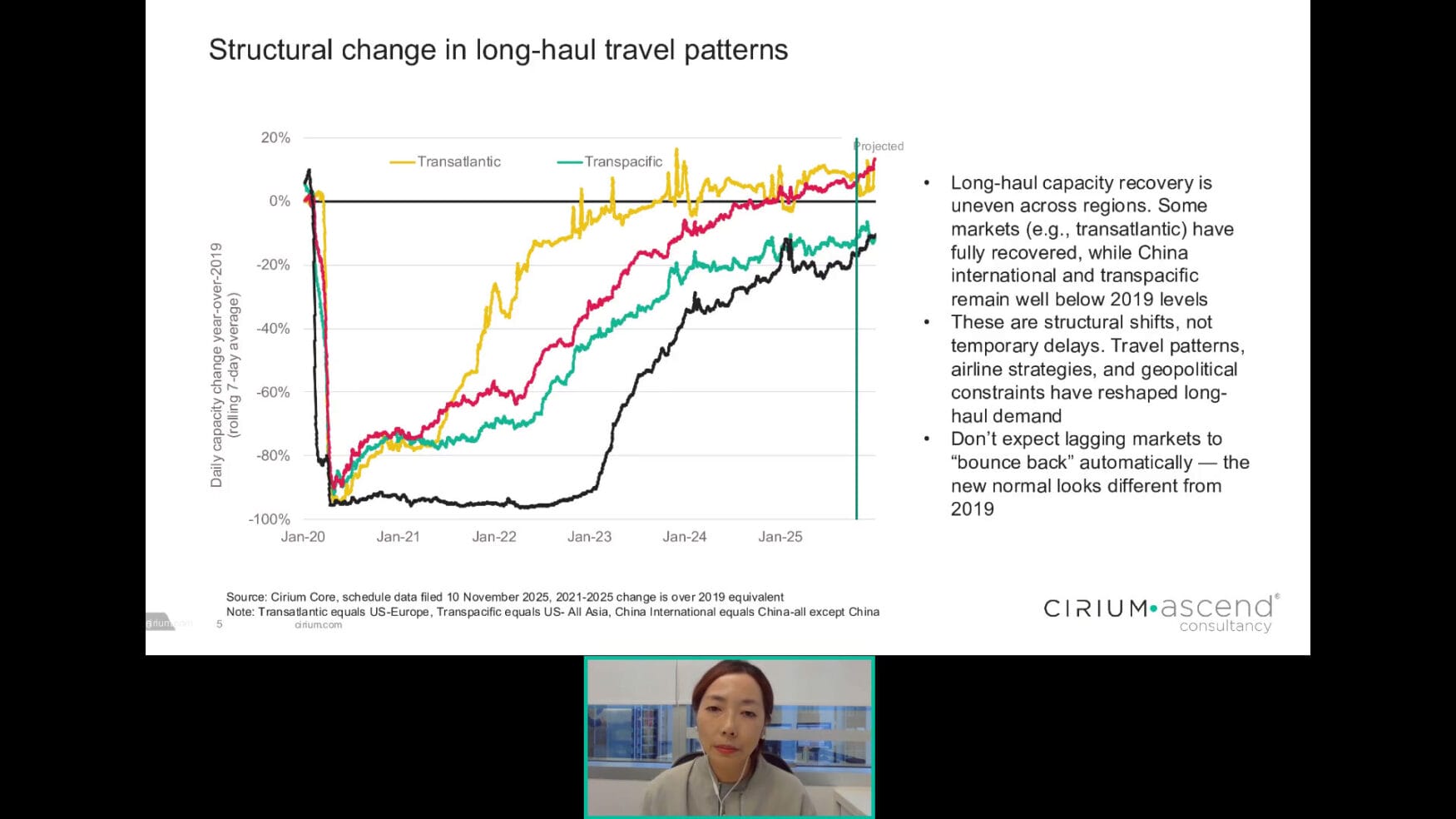

While there is a macro picture of strong growth, the patterns remain uneven between markets.

Capacity on transatlantic and Europe–Asia routes has surpassed pre-pandemic benchmarks, while in contrast, transpacific traffic and China’s international network still lag compared to 2019 levels. This divergence highlights the impact of persistent structural factors, such as strategic fleet deployment, changing traveler behavior, and ongoing geopolitical challenges.

The evolving traveler: new demands and behaviors

Demand drivers are shifting. Surveys consistently highlight a growing emphasis on unique travel experiences, even as inflation acts as a headwind for some travelers. Moreover, flexible and hybrid work patterns continue to blur the line between leisure and business trips, creating more diverse travel profiles and shifting travel seasonality.

Alongside these behavioral shifts, the rise of Asia’s expanding middle class—particularly in India and Southeast Asia—is fueling demand growth. Visiting Friends and Relatives (VFR) travel remains a key driver, offering a resilient source of underlying traffic as other segments fluctuate. Combined with the ongoing trend toward short-haul regional journeys, these factors are prompting airlines and airports to revisit network structures and tailor their offerings to better match these evolving passenger expectations.

The operational imperative: reliability in an era of growth

As network capacity expands to meet renewed demand, maintaining operational reliability continues to be a key challenge. Forecasts for the first quarter of 2026 indicate a 5% increase in capacity across Asia, equating to about 31 million additional passengers.

While this demonstrates strong market momentum, it places more pressure on infrastructure, processes, and resources that are already under strain.

Leading the panel discussion was Ellis Taylor of Cirium joined by colleague Hamsin Nashrudin, and guest speakers Anthony Cicuttini from Brisbane Airport and Nate Srinath from Inxee.

Despite network expansion continuing reliability remains a central concern. Cirium data shows that flight cancellation rates in 2025 remain above the pre-pandemic baseline of roughly 1–1.5%. Even a small uptick results in tens of thousands of additional monthly cancellations, directly affecting passenger experience and operational stability. As the sector scales up, reinforcing reliability shifts from operational concern to a strategic priority – and a key competitive advantage.

Ongoing supply chain challenges and aircraft delivery delays are set to further constrain available fleet growth, despite infrastructure investments. The recent addition of airports in markets such as Navi Mumbai and Noida adds needed capacity, but these projects must be matched with adequate aircraft resources and integrated networks to realize their full benefits.

Driving operational efficiency in aviation

Airports are responding to capacity and reliability pressures by leveraging advanced analytics and artificial intelligence (AI) to streamline operations, alongside strategic infrastructure enhancements.

The emphasis is on maximizing efficiency from existing assets, while new facilities like Navi Mumbai and Noida expand capacity. However, technology and infrastructure must advance together to achieve measurable improvements in performance.

From docking systems to intelligent hubs

A clear example of this transition is the evolution of Visual Docking Guidance Systems (VDGS). Once limited to basic stand guidance, next-generation VDGS platforms now serve as intelligent operational nodes. AI enables these systems to go beyond traditional roles by automating billing with precise arrival timestamps and reducing revenue discrepancies from manual reporting. This digital transformation helps resolve longstanding operational inefficiencies and lays a foundation for broader process innovation.

Critically, these intelligent platforms are transforming airport turnaround performance by capturing granular timestamps for each step of the process, creating robust datasets for targeted operational analysis—from chocks-on and aerobridge placement to passenger transfer, refueling, and baggage movement. Ready access to these detailed metrics empowers teams to identify bottlenecks and inefficiencies, supporting continuous improvement in processes and asset utilization.

Enhancing safety and efficiency

AI-enabled systems also play a crucial role in enhancing airside safety. The latest smart VDGS platforms can automatically identify aircraft types and verify wingtip clearance during docking, reducing collision risk and protecting operational integrity. By streamlining processes and improving reliability, these technologies strengthen the resilience of the airport environment.

Brisbane Airport: a case study in data-driven strategy

With traffic projected to reach 35 million passengers over the next decade, Brisbane Airport (BNE) uses Cirium’s FM Traffic and SRS Analyzer to conduct data-driven assessments that allow it to proactively manage its relationships with airlines, and make infrastructure investment decisions.

Using Cirium’s FM Traffic and SRS Analyser, BNE compares individual routes across an airline’s portfolio and identify opportunities for new services or increased frequency by combining real-time passenger flow with detailed schedules.

This analytical approach reshapes how BNE develops airline partnerships. Rather than relying on anecdotal feedback, the airport enables collaborative, evidence-based discussions on network performance and shared opportunities. They effectively identify key drivers and co-develop actionable strategies—whether refining capacity allocation or launching targeted joint marketing campaigns.

Building the Future of Air Travel

Successfully navigating this landscape requires adopting integrated, intelligence-led operational models. Aviation analytics now underpin decision-making across key areas—demand forecasting, network optimization, turnaround management, and safety protocols. Embedding data-driven insights into strategy and execution enables stakeholders to respond proactively to changing conditions, mitigate disruptions, and chart a path toward resilient, efficient, and effective operations.

In the evolving landscape of commercial aviation, organizations that put analytics at the core of their operations are best positioned for long-term success. The future of air travel will be defined not just by volume, but by how intelligently and efficiently each journey is enabled.

Airports and airlines that leverage real-time intelligence and predictive analytics drive operational excellence, strengthen network resilience, and consistently deliver a reliable, seamless passenger experience.

Watch the Webinar on Demand

The full webinar is now available on demand, along with the presentation deck. Watch ithere.

Cirium Ascend Consultancy is trusted by clients across the aviation industry to provide accurate, timely, and insightful aircraft appraisals. The team provides the valuations and analysis the industry relies on to understand the market outlook, evaluate risks and identify opportunities.

Sofia Zoidou, Senior Consultant, Cirium Ascend Consultancy

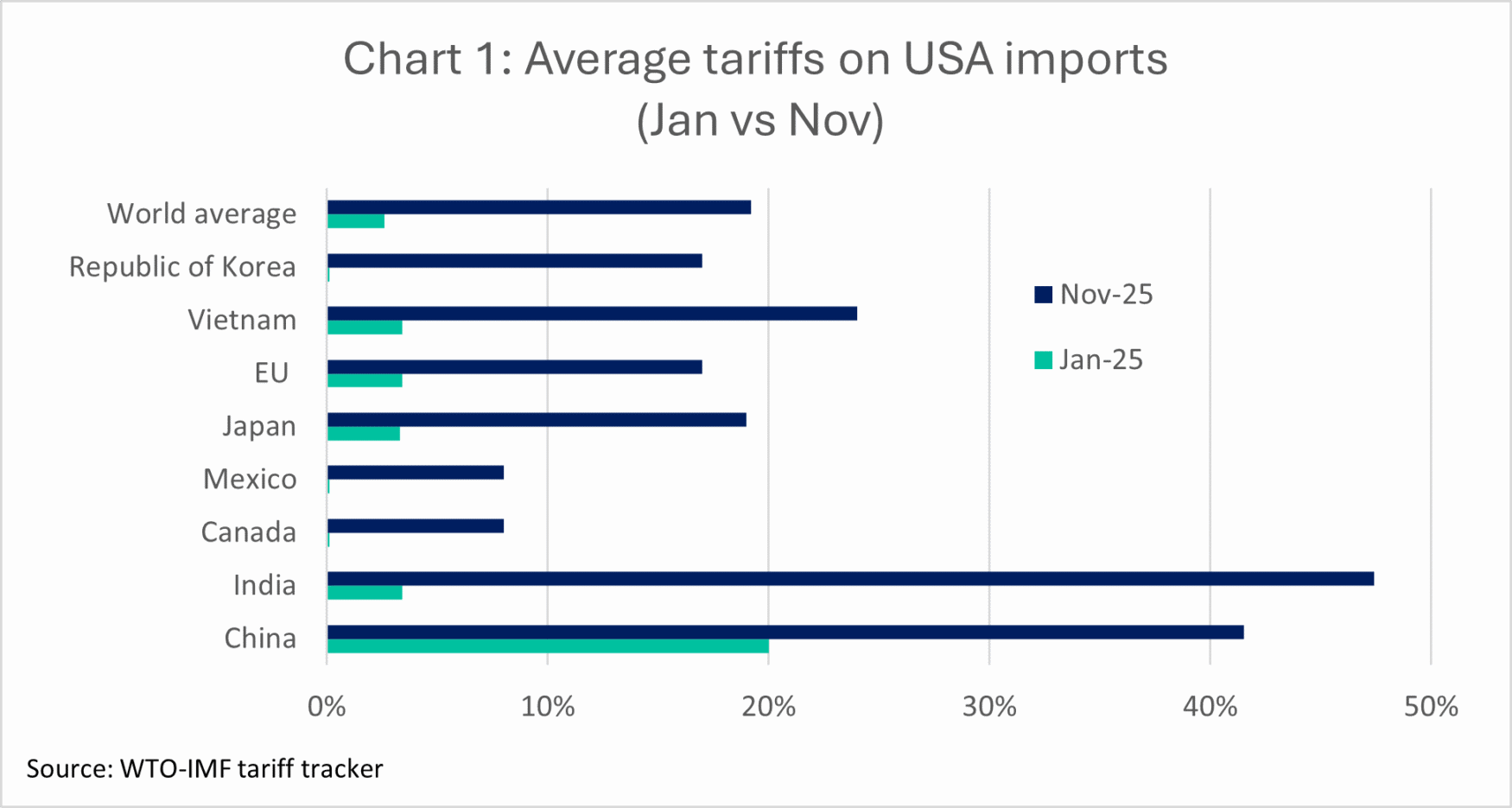

Amid the continued geopolitical conflict and a dramatic escalation of US tariffs, 2025 has been a rollercoaster for global trade.

According to the WTO-IMF tariff tracker, the average tariff rate on US global imports rose seven-fold during 2025, climbing from 2.6% in January to 19.2% in early November. As the USA escalated tariffs for imports from all its major trading partners (Chart 1), this move has affected over $2.7 trillion of trade value so far.

US tariffs on Chinese goods have currently settled at an average 41.5%, following a temporary truce via the trade deal reached in early November. This was after tariffs on China ballooned from an average 20% at the start of the year to a staggering 143% at the peak of the two nations’ trade confrontations in April.

Meanwhile, US tariffs on imports from India, the fastest growing nation in terms of real GDP according to the IMF, rose from 3.4% in January to 47.4% in November, with no trade deal yet at hand (although, reportedly, significant progress has been made in December).

The introduction of import tariffs by the world’s biggest economy as an international trade deterrent should have in theory painted a bleak picture for the world’s economic outlook. Yet, the impact has been surprisingly more subdued than originally expected – so far.

According to the US Bureau of Economic Analysis (BEA), US real GDP contracted by 0.6% in Q1 2025 before rebounding at 3.8% in Q2 (annualised figures as per BEA methodology; Q3 figures expected later in December), whilst data from the National Bureau of Statistics of China suggests the Chinese economy grew by 4% year-on-year in the first nine months of 2025, which is on par with the same period last year. Compared with previous years, this bolsters the argument of a structural GDP growth deceleration in China, as opposed to a tariff-ensuing slow-down.

Looking forward, the IMF World Economic Outlook projects the world’s real GDP will continue to grow at a rate of 3.2% in 2025 and 3.1% in 2026, i.e. largely in line with 2024 (3.3%), despite the reasonably anticipated slow-down in the USA (2% US GDP growth projected for 2025 and 2.1% forecast for 2026 vs. actual 2.8% in 2024).

On this footing, global air cargo has also held up. Cargo tonne kilometres (CTKs) were up annually by 3.3% year-to-date (Jan-Oct), according to IATA’s Global Outlook for Air Transport, just published in December. IATA now estimates the year for global air cargo will close at 3.1% growth, beating its earlier forecast of just 0.7% for 2025.

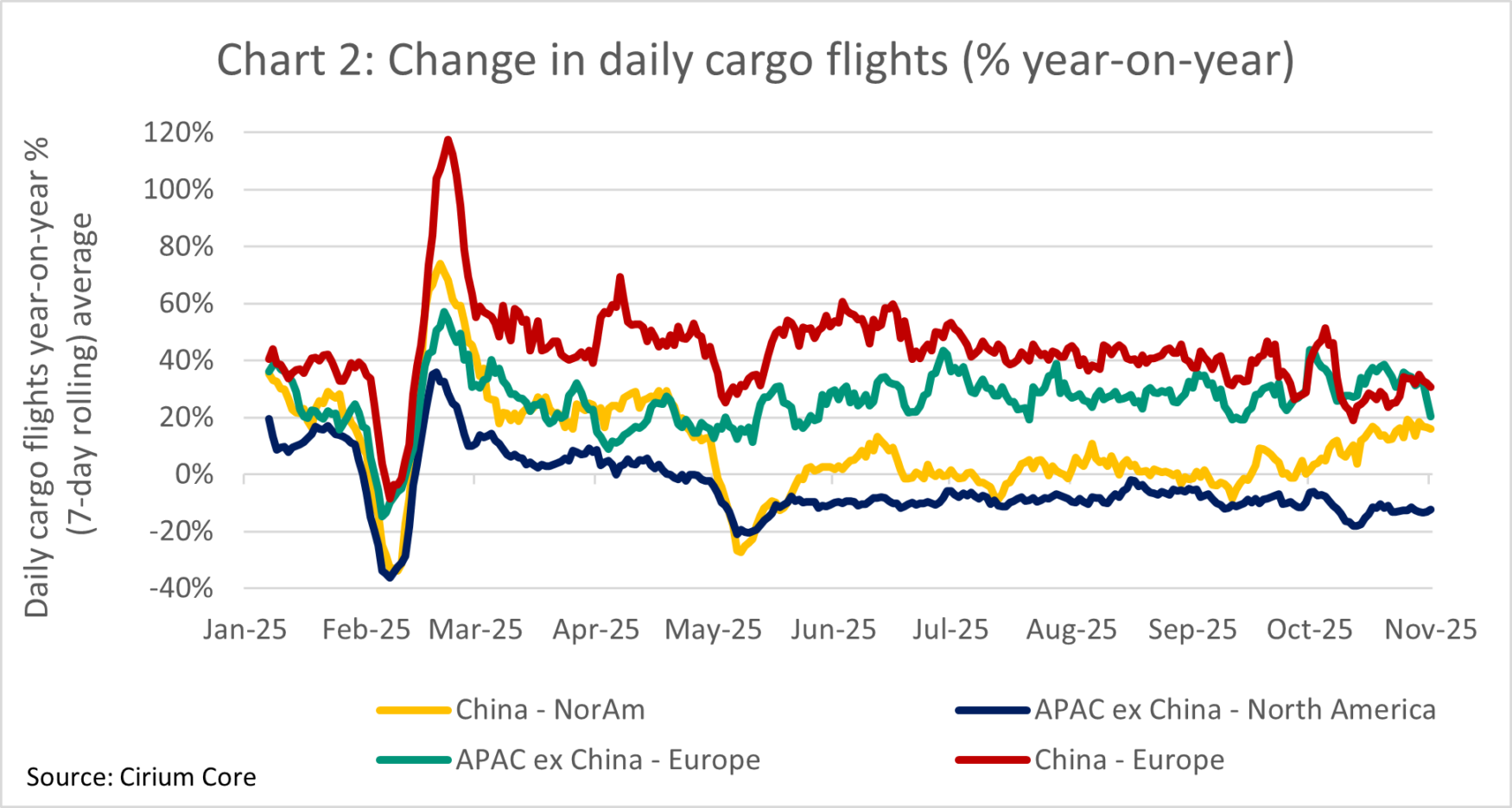

Key driver of acceleration in the air cargo market has been the expansion of the Asia-Pacific to Europe flows, with CTKs on this corridor in January-October up by 10.6% year-on-year. However, the fact that among Europe’s international routes, only those with Asia and North America (+7.1%) grew year-on-year, suggests a meaningful part of this growth may be due to exporters’ repositioning supply chains and rerouting cargo flows to circumvent tariffs.

In contrast, CTKs between Asia-Pacific and North America declined for the sixth consecutive month in October, leading to 1.2% expected contraction for North America in 2025, as per IATA. In addition to the tariffs, the USA’s lifting of the “de minimis exemption” for imports of small value Chinese packaged goods (worth $800 or less) in May has contributed to this decline.

Cirium’s tracked utilisation data for cargo flights confirms these trends (Chart 2; note all-cargo flights represent about half of global CTKs, the remaining captured in passenger jet belly capacity). In the first nine months of 2025, the number of cargo flights from China to Europe rose by 41% year-on-year, with flights from Europe to China also up by 52%. Total flights from the rest of Asia-Pacific to Europe also increased by a significant 23%. Whilst daily flights from China to North America have returned to growth after the summer months, flights from other Asia-Pacific destinations (excluding China) into North America remain contracted by 4% year-to-date and not yet showing signs of recovery, which in turn signifies capacity removal from the route.

Notwithstanding the resilience in the air-cargo markets amidst the uncertainty in 2025, it remains to be seen how much of the growth represents new and sustainable organic demand, and if the levels of rerouting and trade flow recalibration observed this year, offsetting some of the tariffs’ impact, will permanently hold true.

With the Euro area’s GDP growth projection at a mere 1.2% in 2025 as per the IMF, i.e., well below its average forecast of +1.6% for advanced economies, it is debatable how much European demand can propel air-cargo growth going forward.

Despite air cargo typically transporting high-value time-sensitive goods, such as pharmaceuticals and high-tech components, part of Asia to Europe cargo also comprises retail e-commerce purchases. Specifically for low-value-goods’ packages entering the EU, of which more than 90% comes from China, the estimated trade value has more than doubled to $19.1bn in the two years to 2024, having now reached $20.5bn in the first nine months of 2025, Reuters reports.

However, in view of concerns around health and safety regulation compliance, and the competitive ramifications for the European industries, from November 2026 or earlier, the European Commission plans to introduce new customs and handling fees on low-value packages – a development likely to deplete the air cargo volumes from Asia to Europe to some degree.

Moreover, the USA’s extension of the “de minimis exemption” removal to small value parcel shipments from all countries, in addition to China, since August is likely to further squeeze US air cargo volumes going forward.

Lastly, following the ceasefire in the Middle East, most major container-shipping carriers are now resuming Red Sea/Suez Canal transits, after detours added around 10 extra days on their Asia-Europe voyage, which accounts for approximately 10% of global container volumes (East to West is 30-40%). On this basis, and in view of the continuing decline of shipping freight rates, it is likely any benefit from substitution by air cargo will subside in the forthcoming months. For these reasons, and with IATA’s outlook suggesting CTK growth slowing to 2.6% year-on-year in 2026, the air cargo market’s performance is one to closely watch, as it balances between growing demand and the effects of regulatory and geopolitical developments.

London, 04 December, 2025: Cirium, the global leader in aviation analytics, has announced a major step forward in sustainable travel, as it signs a landmark deal with Perk, the intelligent platform for unified travel and spend management.

Through this agreement, Perk’s customers now benefit from Cirium’s advanced flight emissions data – delivered via EmeraldSky, Cirium’s revolutionary flight emissions tracking tool. It enhances visibility into the environmental impact of flight choices, helping businesses and travelers make smarter, sustainability-led decisions.

For the first time Cirium’s flight-specific emissions data is marking a major leap forward for Corporate travel. The solution delivers unrivalled precision in CO₂ tracking, thanks to Cirium’s fusion of comprehensive flight data, science-led methodology, and real-time analytics.

Perk, one of the world’s fastest-growing travel management platforms, is now leveraging Cirium’s forecast and flown emissions insights to provide travelers and businesses with accurate, transparent CO₂ estimates at point of search. Post travel, these insights feed into Perk’s intelligent reporting suite, supporting sustainability tracking and regulatory compliance for the 10,000 companies the platform supports worldwide. This integration strengthens Perk’s position as the go-to platform for companies aiming to reduce business travel emissions responsibly and at scale.

Jeremy Bowen, Cirium CEO, said: “Accurate flight emissions data is essential to monitor the travel industry’s path to reach sustainability goals, and Cirium is proud to be the trusted source behind one of the most widely used corporate travel platforms. This partnership with Perk reflects the growing demand for credible, science-based data for the flight portion of the travel experience, and thanks to EmeraldSky, Cirium can now provide this to customers across the world who prioritize sustainability when booking flights and choosing their routing.”

Jean-Christophe Taunay-Bucalo, Perk President and Chief Operating Officer, said: “We’re thrilled to partner with Cirium to bring trusted, high-quality flight emissions data into Perk. CO₂ tracking is essential, but for most teams it’s been a manual, time-consuming task. By combining Cirium’s trusted data with Perk’s intelligent platform, businesses can eliminate that repetitive manual work and move beyond estimates to automated, reliable insights that support compliance and meaningful reductions.”

This builds on Cirium’s long-standing relationship with Perk, and follows the Group’s 2025 acquisition of AmTrav, an existing Cirium customer, which focuses on the US market.

Launched in 2024, Cirium’s EmeraldSky is an innovative platform, powered by a revolutionary methodology. It analyzes each flight’s specific aircraft type and configurations, combined with real-time operational data and flight conditions, ensuring unparalleled accuracy and reliability in emission tracking. As businesses face increasing pressure to reduce emissions, Cirium offers a future-proof solution for carbon accountability – empowering companies to meet internal targets while providing travelers with transparency and choice.

EmeraldSky seamlessly integrates Cirium’s comprehensive data, advanced analytics, and data science techniques to achieve unmatched precision in measuring both forecast and flown CO₂ flight emissions.

Unlike traditional carbon calculators that depend on broad estimates and generic assumptions – such as using great circle distance instead of actual flown flight paths, and ignoring variables like wind speed, direction, and actual airframe and engine maintenance records – EmeraldSky provides emissions results based on the seat in a specific class of service and sets a new standard in aircraft emissions measurement.

To learn more about Cirium’s comprehensive aviation analytics and detailed insights, visit www.cirium.com.

About Cirium Cirium® is the world’s most trusted source of aviation analytics. The company delivers powerful data and cutting-edge analytics to empower a wide spectrum of industry players. It equips airlines, airports, travel enterprises, aircraft manufacturers, and financial entities with the clarity and intelligence they need to optimize their operations, make informed decisions, and accelerate revenue growth.

Cirium® is part of LexisNexis® Risk Solutions, a RELX business, which provides information-based analytics and decision tools for professional and business customers. The shares of RELX PLC are traded on the London, Amsterdam and New York Stock Exchanges using the following ticker symbols: London: REL; Amsterdam: REN; New York: RELX.

About Perk Perk (formerly TravelPerk) is the intelligent platform for travel and spend management, built to eliminate the hidden, manual tasks that drain productivity and morale – Perk calls these ‘Shadow Work’. By automating travel bookings, expenses and invoice processing, the platform gives teams back time to focus on real work, with real impact. Trusted by more than 10,000 companies worldwide – including Wise, On Running, Breitling and Fabletics – Perk is tackling the 7 hours of lost productivity per employee each week, a $1.7 trillion problem revealed in The Cost of Shadow Work report. Founded in 2015, the global company combines innovation, control, and simplicity to transform how businesses work today and in the future. Perk’s mission is to power real work by removing the invisible tasks that slow teams down.

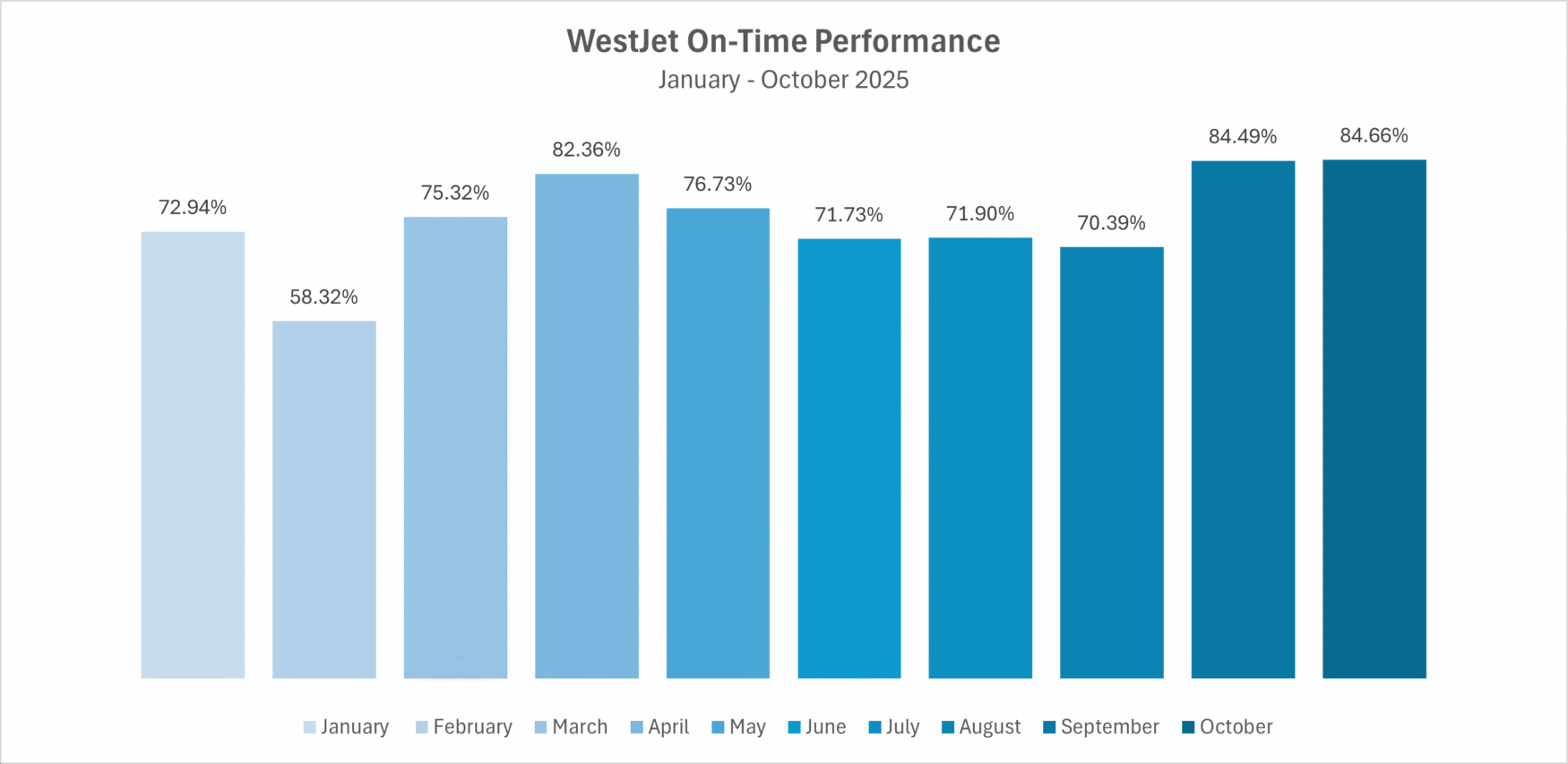

I’ll be honest—when I saw WestJet’s October numbers come across my desk, I had one thought: Good grief, this is fantastic. 84.66% on-time performance. Number one in North America. Not just good—the best.

Here’s what makes that achievement so impressive: just over a year ago, WestJet was posting around 71% on-time arrivals across nearly 192,000 flights. That put them near the bottom of major North American carriers—a tough place to be when your customers, your employees, and your investors are all watching the same scorecards.

Every month, I review on-time performance results with our committee and board. We see incremental improvements, seasonal dips, weather recoveries—the usual rhythm of airline operations. But October 2025 wasn’t usual. This was different. We all felt it was a big deal, and I don’t think most people truly understand what it takes to post these kinds of numbers.

What Most People Don’t See

When passengers see an 84% on-time rate, they might think: “Pretty good odds I won’t be delayed.” And they’re right—but they’re missing the real story.

What that number actually represents is thousands of people doing hundreds of things right, repeatedly, under pressure. It’s gate agents, dispatchers, maintenance crews, pilots, and operations centers all executing with precision. It’s schedules built with discipline. It’s recovery plans that actually work when things go sideways.

You don’t get to 84.66% OTP by hoping for good weather. You get there through relentless operational focus and a culture that treats reliability as non-negotiable.

Leadership That Gives Credit Where It’s Due

I’ve met a lot of airline CEOs over the years. Some are brilliant strategists. Others are financial experts. A few are operations specialists.

Alexis von Hoensbroech, who became WestJet’s CEO in February 2022, is something different—and refreshingly so. When I met him at a conference, what struck me wasn’t just his impressive background (a physics PhD from the Max Planck Institute, years at Boston Consulting Group, sixteen-plus years in senior roles at Lufthansa Group including CEO and CFO of Austrian Airlines). It was how genuinely warm and personable he was—surprisingly so for a CEO with those credentials.

More importantly, when he talks about WestJet’s operational progress, he consistently gives credit to the teams doing the work. That kind of humility from a leader with his accomplishments says a lot about how he’s building the airline’s culture.

His approach appears to focus on two principles: shared accountability across the operation, and schedule discipline as the foundation of everything else. Those aren’t just words at WestJet—they’re visible in the month-over-month data.

Alexis von Hoensbroech CEO, WestJet

Building the Foundation

WestJet’s network today spans major hubs in Calgary, Toronto Pearson, and Vancouver, with extensive transborder and leisure flying. That’s a complex operation—the kind that exposes any weakness in your processes.

The airline is also midway through significant fleet modernization. In 2025, WestJet announced an order for 67 Boeing aircraft—60 737-10 MAX jets and 7 787-9 Dreamliners, with deliveries through 2034. Modern fleets don’t guarantee operational excellence, but they certainly help create the conditions for it.

September’s numbers already showed momentum—roughly 84.5% OTP, putting WestJet among the month’s top performers. October confirmed it wasn’t a fluke.

Why This Matters

Airlines around the world take on-time performance seriously, and they should. It affects brand reputation, investor confidence, and employee morale. When I see results like WestJet’s, it makes me proud that Cirium’s data plays a role in helping airlines benchmark and improve.

But more than that, I genuinely want to see the industry succeed. Every carrier doing well lifts the entire sector. And when an airline posts numbers like this—especially after climbing from a challenging baseline—it proves something important:

You can fix an airline. It takes clear leadership, operational discipline, fleet investment, and teams committed to execution. It doesn’t happen quickly, and it doesn’t happen by chance. But it can be done.

What Comes Next

The coming months will tell us whether October represents WestJet’s new normal or an early chapter in a longer story. Either way, this moment matters.

It’s proof that when airlines focus on the fundamentals—schedule integrity, operational coordination, and accountability at every level—the results show up in the data. And when those results are sustained, everything changes: customer trust rebuilds, brand strength returns, and business resilience grows.

Congratulations to Alexis and the entire WestJet team. October 2025 will be remembered as the month you reached the top of North American on-time performance.

And from where I sit, that’s fantastic news for everyone.

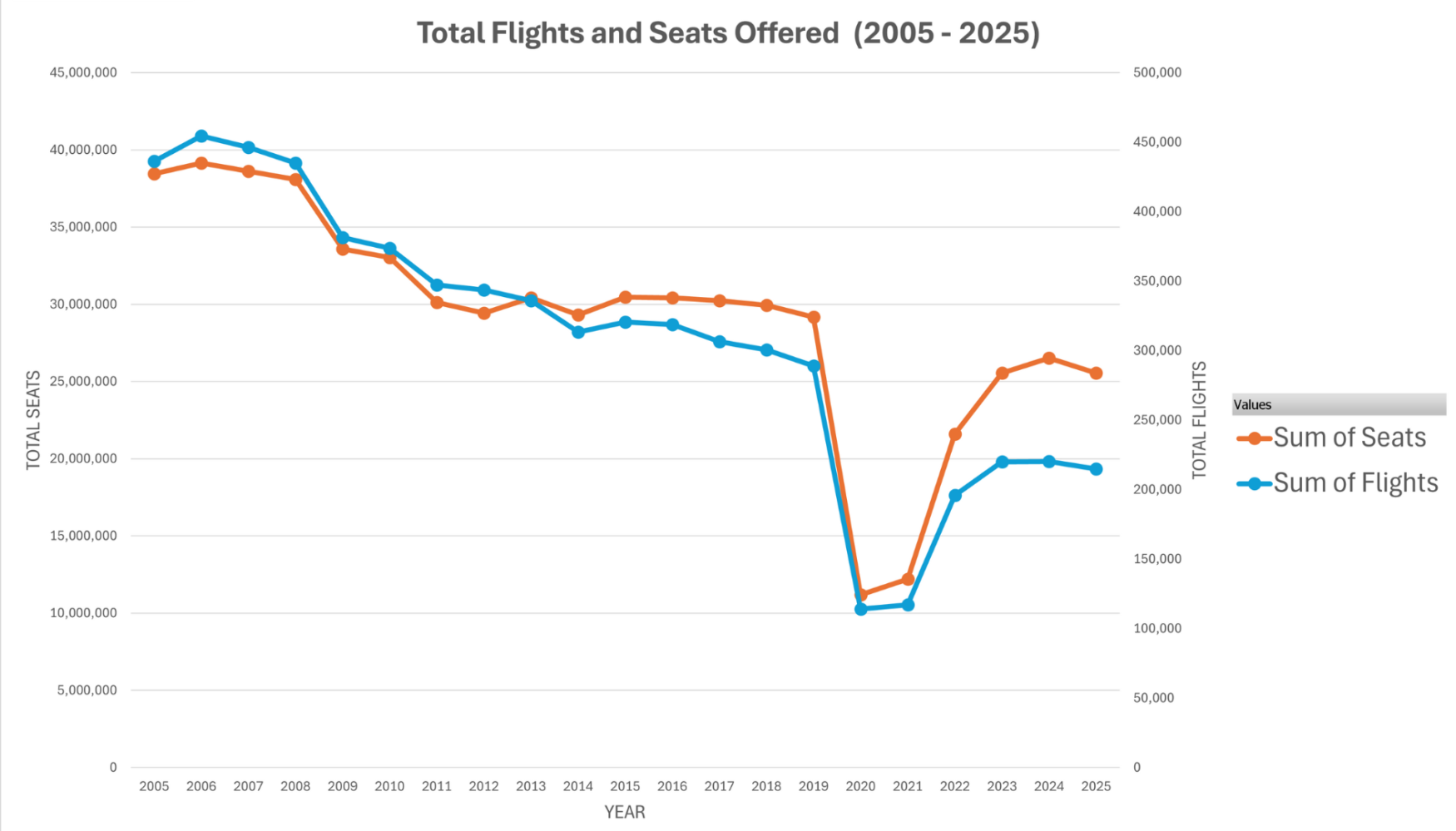

Data from aviation analytics firm Cirium reveals that the number of domestic UK flights has more than halved over the past 20 years, with 214,796 flights scheduled throughout 2025, compared to a peak in 2006 of 454,375 flights.

This equates to almost 240,000 fewer flights scheduled in 2025 than 2006, amounting to an average daily reduction of 657 flights across the UK.

A combination of higher Air Passenger Duty tax, shifting environmental concerns and the ability for airlines to make greater profits from short-haul services beyond the UK have contributed to the decline.

The reduction in domestic flights has impacted regional airports with several UK hubs closing their commercial operations over the past 20 years, including Doncaster Sheffield in 2022, Blackpool in 2014 and Plymouth in 2011.

The demise of Flybe, once the UK’s largest domestic operator, during the pandemic in 2020 will also have affected the number of available flights. However, the decline was already prevalent prior to Flybe entering administration and a number of routes previously operated by the carrier have since been taken over by other airlines.

2025 will see 74,125 fewer flights compared to pre-pandemic levels.

The number of available seats has significantly decreased during the past 20 years, dropping 35% from 39.1 million in 2006 to 25.5 million seats in 2025. This represents a drop of 37,000 fewer passengers flying on internal flights each day within the UK.

More recently, flights have decreased since 2024, with almost a million fewer seats available for domestic UK travel this year.

The general reduction of internal flights across the UK is driven by a change in customer demand and shifting strategy among airlines which have dropped domestic services following the doubling of Air Passenger Duty rates in 2007.

Jeremy Bowen, Cirium CEO, said: “This reduction over the past two decades shows a staggering change in the way we travel throughout the UK. Passengers are looking at more sustainable and affordable ways to travel domestically, so airlines have responded by reducing their internal services and prioritising more popular destinations including Spain, France and Italy.”

This substantial change in the way people travel throughout the UK coincides with a rise in rail travel, according to the Office of Rail and Road’s (ORR) Passenger rail usage statistics. The ORR has seen a 50% increase in rail travel from 1.15 billion passengers in 2005/6 to almost 1.73 billion in 2024/5.

See the full dataset below, and further sustainability analysis is available using Cirium’s EmeraldSky tool:

About Cirium Cirium® is the world’s most trusted source of aviation analytics. The company delivers powerful data and cutting-edge analytics to empower a wide spectrum of industry players. It equips airlines, airports, travel enterprises, aircraft manufacturers, and financial entities with the clarity and intelligence they need to optimize their operations, make informed decisions, and accelerate revenue growth.

Cirium® is part of LexisNexis® Risk Solutions, a RELX business, which provides information-based analytics and decision tools for professional and business customers. The shares of RELX PLC are traded on the London, Amsterdam and New York Stock Exchanges using the following ticker symbols: London: REL; Amsterdam: REN; New York: RELX.

Cirium Ascend Consultancy is trusted by clients across the aviation industry to provide accurate, timely, and insightful aircraft appraisals. The team provides the valuations and analysis the industry relies on to understand the market outlook, evaluate risks and identify opportunities.

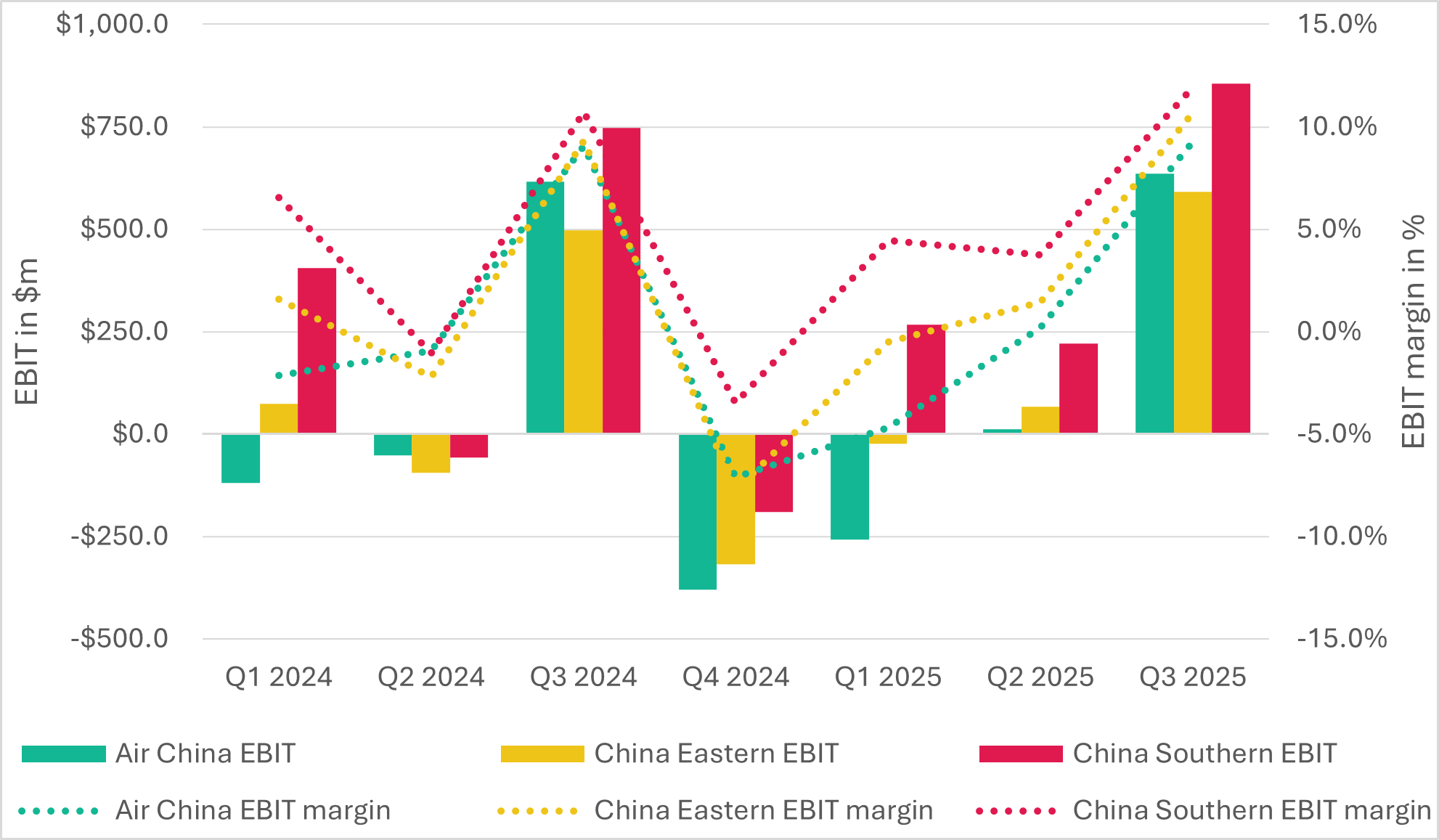

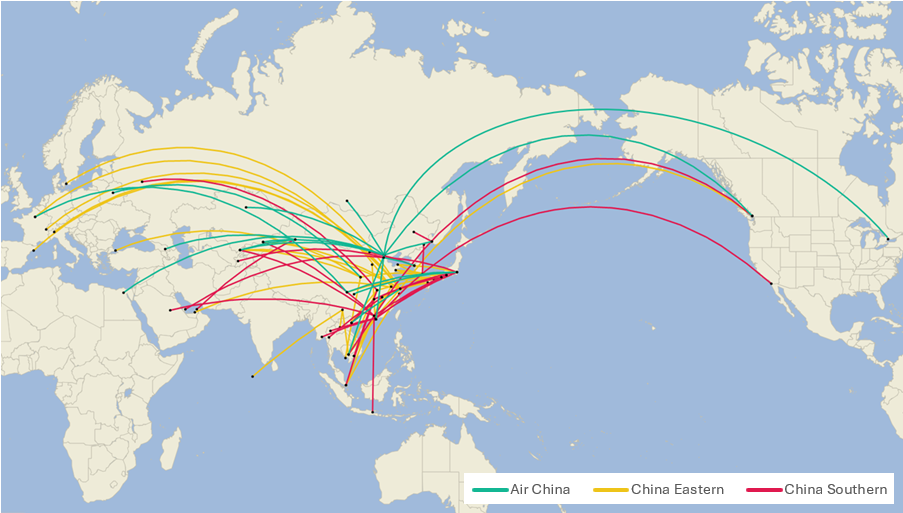

Following the release of their 2025 third-quarter financial reports, China’s “big three” airline groups (Air China, China Eastern and China Southern) have delivered a robust post-pandemic performance.

All three carriers posted modest revenue growth and continued year-on-year improvements in operating profit, led by China Eastern, which recorded a 19.4% increase in operating income and a 32.5% rise in net profit compared with Q3 2024.

On the leverage and liquidity side, all three airlines reported a decline in their net debt/EBIT ratios compared with the same quarter last year, coupled with an improved liquidity profile, except for Air China, which recorded massive debt repayments that outpaced the growth of cash flow generated from operating activities.

Boosted by an exceptional Q3 performance and improving Q2 results, China’s “big three” delivered their first profitable nine-month’s financial result since the onset of the pandemic. This milestone was met with a positive market reaction, reflected in rising share prices.

Chart 1: Chinese ‘big three’ airlines quarterly EBIT and EBIT margin (post 2024)

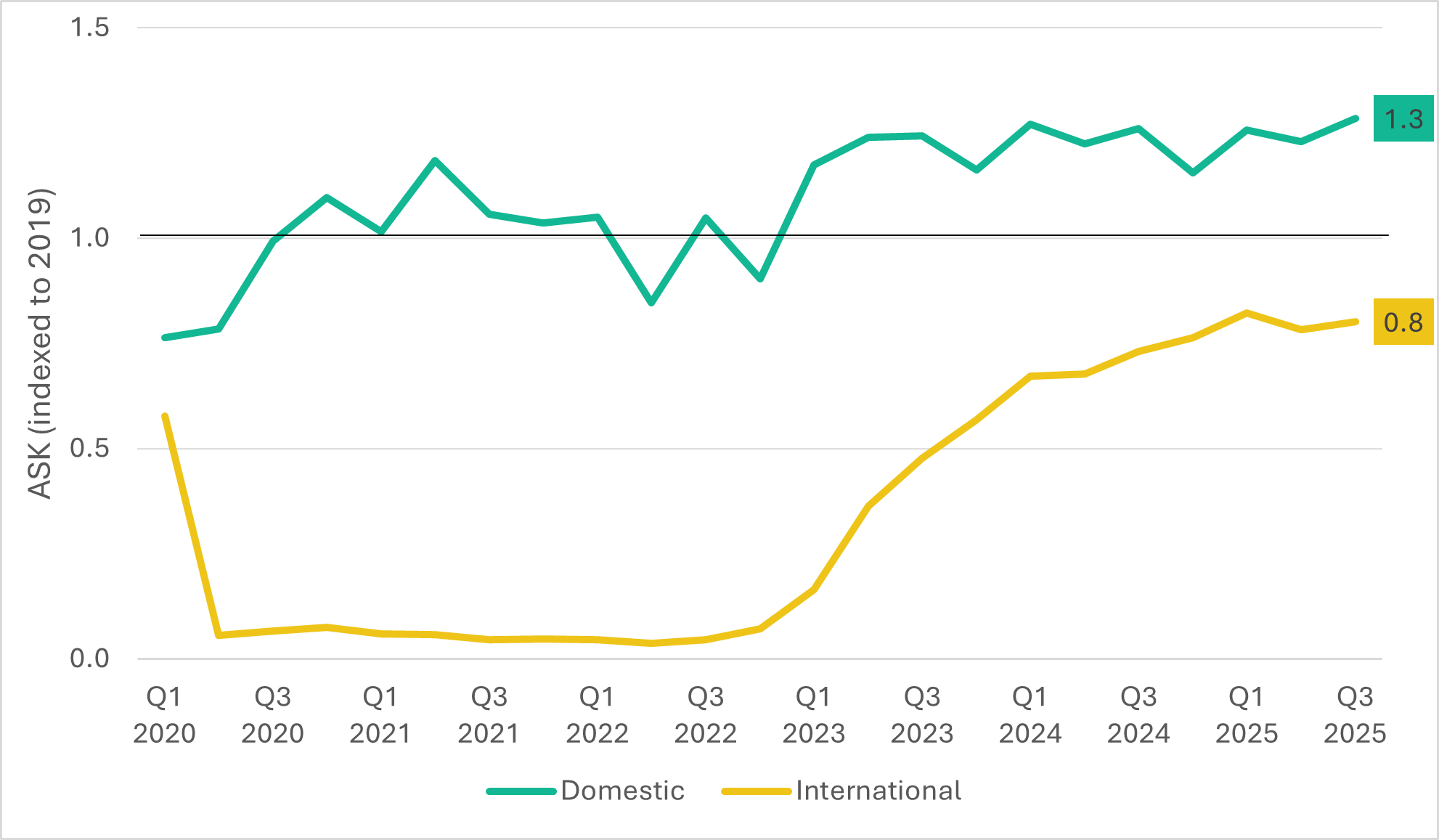

According to Cirium schedules data, although Chinese domestic market capacity shortly surpassed 2019 levels during Q3 2020 and Q1 2022, it consistently exceeded pre-pandemic levels starting in 2023. While the international market segment remains 20% below pre-pandemic levels at present, it has shown a moderate recovery trend since 2023. Supported by favourable travel and visa policies and an economy further emerging from the impact of the pandemic, both inbound and outbound passenger volumes have begun to climb.

Chart 2: Chinese market air traffic capacity recovery (ASK, indexed to 2019)

Source: Cirium schedules data Note: As of Nov 2025, Bi-directional traffic

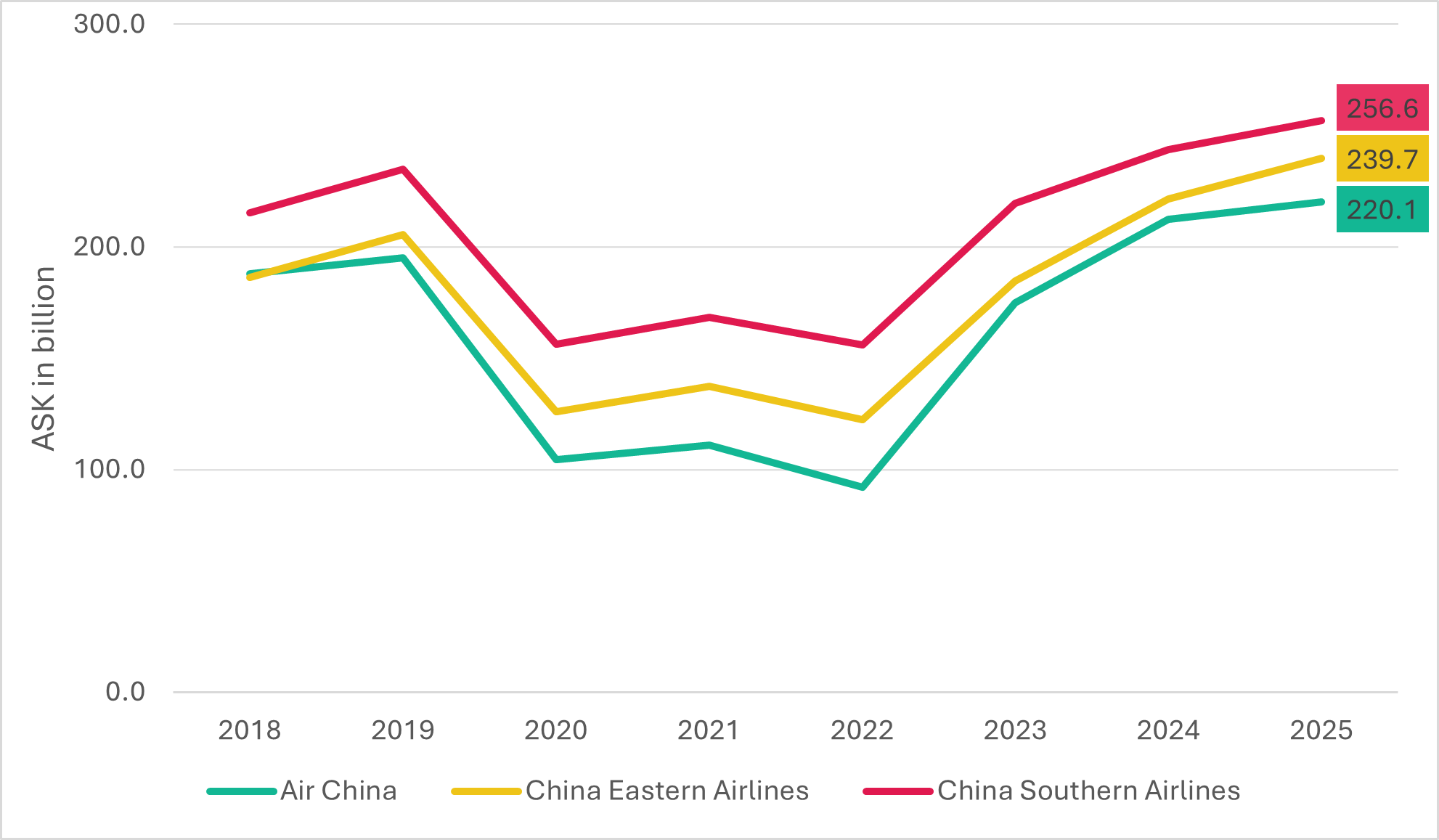

Benefitting from the large Chinese domestic market scale, Chinese airlines experienced an efficient capacity recovery during the post-pandemic period. Cirium’s schedules data shows that the capacity of the “big three” have largely outperformed their pre-pandemic capacity benchmarks, with ASKs exceeding 2019 levels as of 2023.

Chart 3: Chinese ‘big three’ airlines capacity (post-2018)

Source: Cirium schedules data Note: Bi-directional traffic as of Nov 2025; excludes each group’s subsidiaries

With their eyes on the big recovery potential of the international market and government policy support, all three major carriers have accelerated the restoration and expansion of international routes, with China Eastern standing out as a notable example.

According to Cirium schedules data, during Q3 2025, China Eastern added a net 17 international routes on top of the 170 routes operated in Q3 2024, primarily focussing on European and South Asian market segments. Air China and China Southern also recorded net increases of 12 and 15 international routes in Q3 2025, compared with Q3 2024 respectively. China Eastern disclosed plans to continue increasing the flight frequencies on several routes connecting key cities in South Asia (Singapore, Kuala Lumpur and Bangkok) during Q4 2025 and further expanding its international routes in the first half of 2026. Meanwhile, China Southern announced its focus on boosting capacity on routes connecting Australia in 2026.

Chart 4: New international routes launched by ‘big three’ in Q3 2025 vs Q3 2024

Source: Cirium schedules data

In addition to sustained growth in air travel demand and the successful strategy of expanding international market segments, wider profit margins were largely driven by precise cost-control measures implemented by the carriers, along with benefits from stable jet fuel prices and the appreciation of the yuan against the US dollar during the first three quarters of 2025. However, these factors represent short-term advantages and may not persist in the longer term. Continued depreciation or volatility of the yuan against the US dollar would heighten operational uncertainty, given that Chinese airlines’ primary currency exposure is to the US dollar.

However, one issue became particularly concerning in 2025. Although traffic grew strongly in the first half of 2025, airlines saw only a modest improvement in passenger yields, largely due to intense market competition, commonly described as “involution”. This term refers to competition becoming excessively intense without creating additional value, resulting in diminishing returns for all market participants. In the aviation market, this refers to situations where Chinese carriers engage in aggressive fare undercutting to gain market share, often driving prices below sustainable levels.

Industry experts have also recognised this issue and have begun addressing it through regulatory measures. In 2025, regulators summoned several Chinese airlines for closed-door meetings to address concerns over excessively low ticket prices. Authorities mandated that fares must not drop below CNY200 ($28) and announced continuous price monitoring, warning that any airline selling below this threshold would face penalties. The rationale for the minimum fare is that the marginal cost per seat on many routes exceeds this amount, aligning with the authorities’ objective of preventing predatory pricing below costs.

In August 2025, the China Air Transport Association (CATA) officially released the “Self-Discipline Convention on Air Passenger Transport” (Convention), aimed at standardising the domestic air passenger market. The Convention emphasises that online travel platforms and ticketing agents must strictly adhere to airlines’ published fares, usage conditions, and refund/change policies, and prohibits unauthorised bundled sales or surcharges.

The fourth quarter is typically weaker in the Chinese market than the first three quarters due to the absence of public holidays. This contrasts with the US and European markets, where Thanksgiving, Christmas and New Year continue to drive visiting friends and relatives (VFR) travel demand. Even so, Q4 traffic is expected to see year-on-year growth, supported by strong booking momentum and robust air travel recorded during October’s Golden Week.

The positive financial performance over the first nine months is a strong indicator of aviation market recovery and could further boost confidence in the financial outlook for Chinese airlines. International routes remain a critical driver of airline profitability, with load factors on high-yield segments playing a major role in earnings flexibility. In the first half of next year, Chinese carriers are expected to capitalise on increased capacity and supportive policies to boost yields and widen profit margins, potentially reducing losses or even returning to profitability. If strong load factors carry through to summer, combined with gradual fare yields’ recovery and stable costs, Chinese airlines could achieve a meaningful recovery in 2026.

Cirium Ascend Consultancy is trusted by clients across the aviation industry to provide accurate, timely, and insightful aircraft appraisals. The team provides the valuations and analysis the industry relies on to understand the market outlook, evaluate risks and identify opportunities.

Sara Dhariwal, Senior Aviation Analyst, Lead Appraiser – Helicopters & AAM, Cirium Ascend Consultancy

Emergency Medical Services (EMS) helicopters have become a critical component of healthcare in many high-income countries. They enable patients in life-threatening conditions to reach hospital within the “golden hour”, often much faster by air than by road. In some markets, they are also used for inter-hospital transfers when specialised care is required.

The EMS helicopter sector is highly dependent on funding, which can come from public or private sources. Operating models vary widely and include:

Government-funded services at national or local level.

Privately-owned hospitals, particularly in the United States.

Charity-funded operations, common in the United Kingdom.

Publicly funded, non-profit organisations.

Insurance and roadside assistance organisations, such as those in Germany.

Aircraft may be operated directly by these organisations or outsourced to commercial operators under contract.

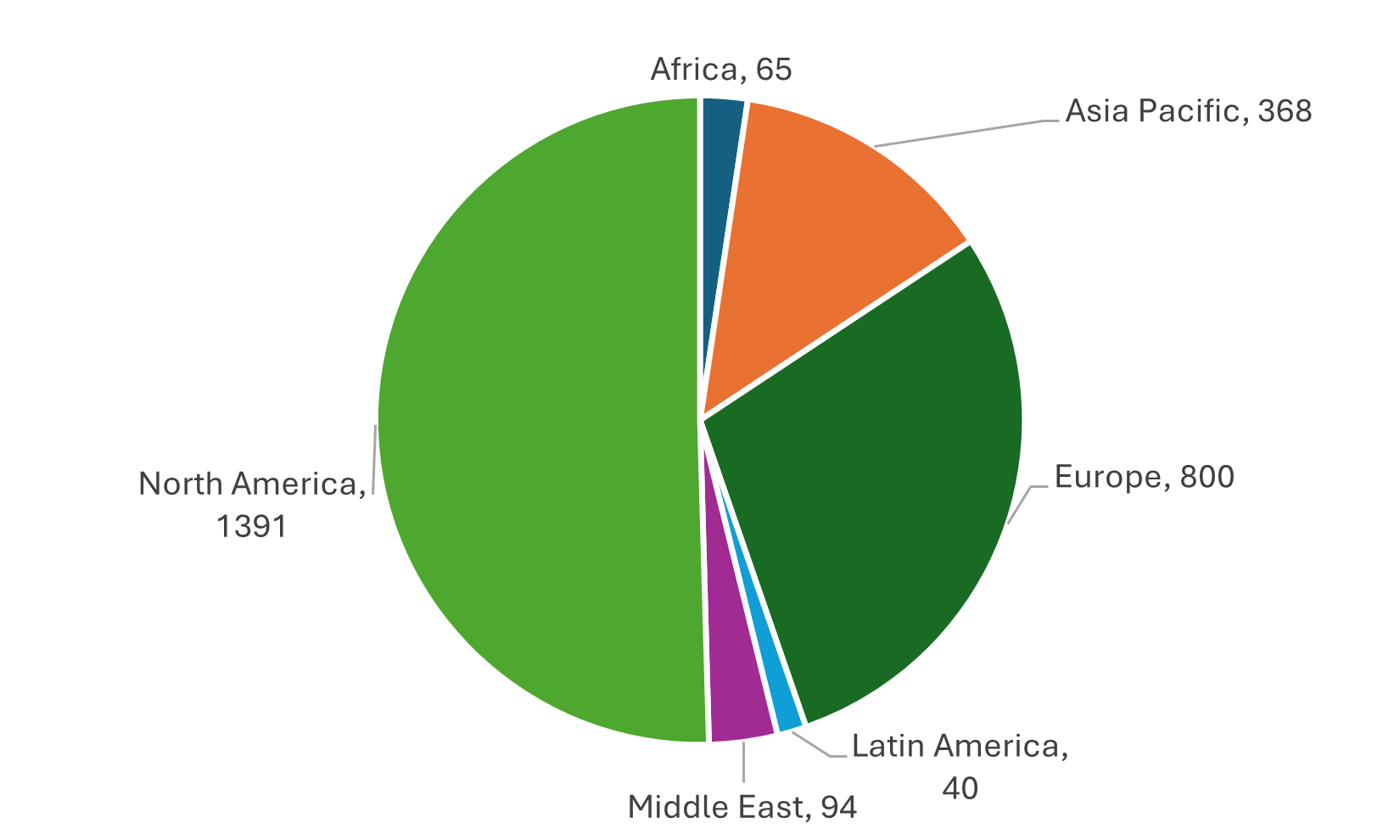

The largest EMS helicopter fleet operates in North America, with nearly 1,400 aircraft configured for emergency missions—accounting for around 50% of the global total. Europe ranks second, operating approximately 800 helicopters, which represents close to 30% of the worldwide fleet.

Source: Cirium Core

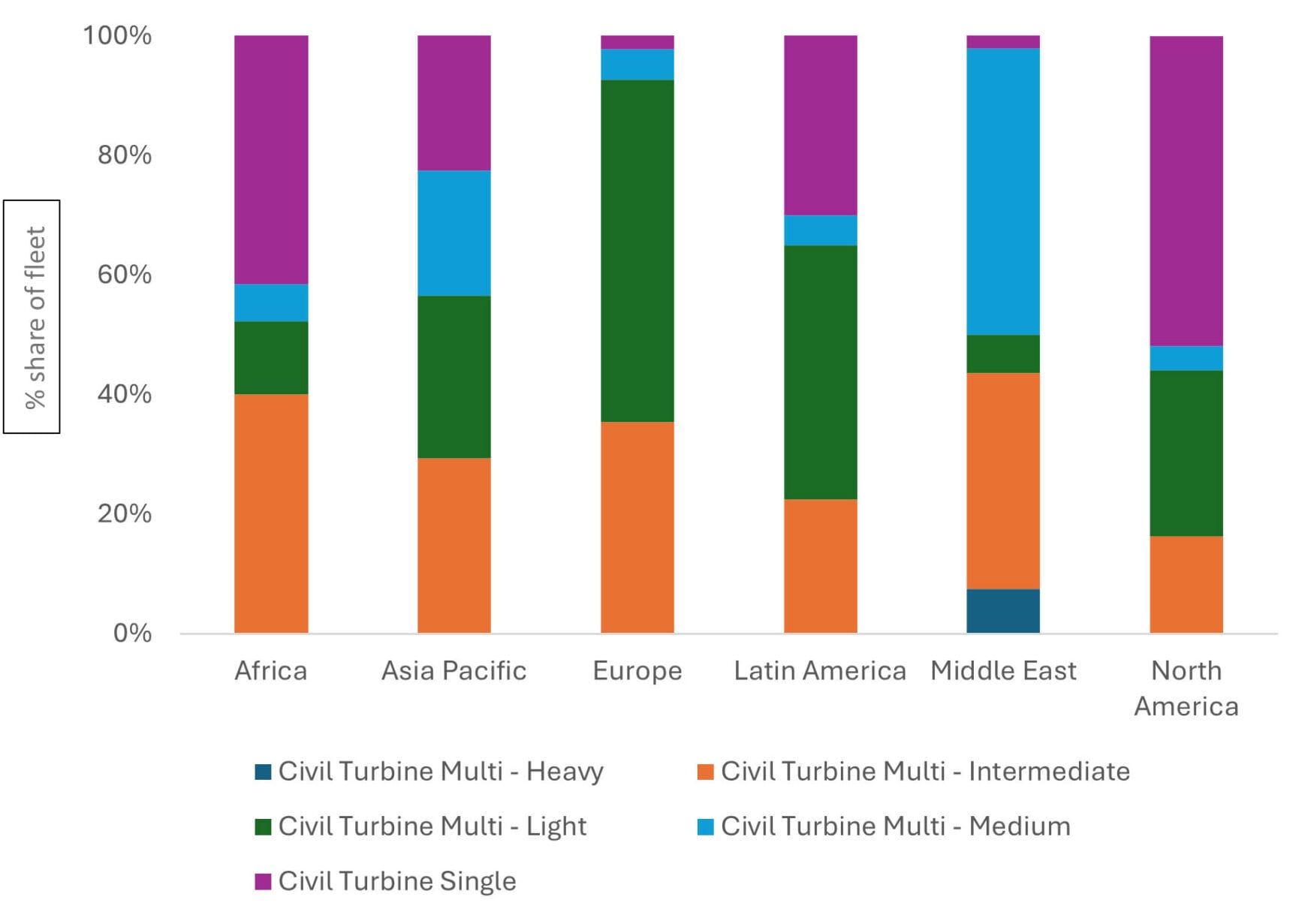

Fleet composition differs significantly between these regions. In North America, single-turbine helicopters make up just over half of the fleet. In contrast, Europe rarely uses single-engine aircraft for EMS, with these representing only about 3% of its total fleet. This disparity stems largely from the single-engine-out rule introduced as part of EASA safety regulations in the early 2000s. This rule required that helicopters operating in certain conditions (e.g., over densely populated areas or at night) must be able to continue safe flight and landing after an engine failure—something single-engine helicopters cannot guarantee.

There has also been a shift in operational philosophy. Rather than viewing helicopters solely as transport vehicles for moving patients from accident scenes to hospitals, Europe increasingly embraces the concept of delivering advanced emergency care onboard—similar to an ambulance. Consequently, cabin size has become a critical factor, driving a transition towards larger, medium twin-engine models, which now dominate the European EMS fleet.

Source: Cirium Core

Over the past decade, the EMS fleet has grown steadily at around 2.5% per year. This expansion has been partly enabled by lessors—of the approximately 560 helicopters added since 2015, 45% were leased aircraft. The leased share of the total EMS fleet is now at 14%, increased from 3% a decade ago.

The rise in leased fleet share within the EMS sector was likely driven by lessors seeking to diversify portfolios that had previously been heavily exposed to the volatility of the oil and gas market. Another contributing factor is the growing demand for larger, more complex helicopter configurations, which become significantly more accessible through leasing arrangements.

EMS contracts are generally more stable and long-term than those in the offshore sector—and for good reason. EMS helicopters require highly specialised configurations, often tailored for compatibility with hospital equipment. A seamless ‘plug-and-play’ capability upon patient arrival is critical for continuity of emergency care. Consequently, transferring a leased helicopter between operators typically involves costly interior modifications. Longer contract terms help ensure a return on investment for lessors, making stability essential in this segment.

Outlook

Looking ahead, the EMS helicopter market seem to be entering a phase of consolidation rather than rapid expansion. With growth moderating to just over 1.5% annually according to Cirium Fleet Analyzer and driven primarily by Asia, the industry’s focus will shift from fleet enlargement to asset optimisation.

Approximately 30% of the existing fleet—largely concentrated in Europe and North America—will require replacement, underscoring the importance of lifecycle planning and cost efficiency. Cirium are expecting new deliveries to focus on twin engine types rather than single engine. New types like the H140 and the R88 are likely to stimulate demand.

For lessors, whose share of deliveries has plateaued, competitive advantage will increasingly depend on innovative leasing models and value-added services rather than scale.

In short, success over the next decade is likely to focus on operational resilience and strategic positioning in a market where replacement, not growth, defines the opportunity.

Attending European Rotors in Cologne, Germany? Sara will be taking part in the HEMS panel, Tuesday, 18th November at 15:15.