Cirium Ascend Consultancy is trusted by clients across the aviation industry to provide accurate, timely, and insightful aircraft appraisals. The team provides the valuations and analysis the industry relies on to understand the market outlook, evaluate risks and identify opportunities.

Discover the team’s industry reports & market commentaries. Read their latest expert analysis, viewpoints and updates on Thought Cloud.

Team Perspective

Richard Evans, Senior Consultant, Cirium Ascend Consultancy

While it is too early to predict the length or macro-level effect on the global economy of the conflict in the Middle East, we can measure the impact to-date on airline capacity, via Cirium’s Tracked Utilisation data.

At the start of 2026, Cirium Ascend Consultancy’s view was that global traffic (RPKs) and capacity (ASKs) would grow in the range of 4-6% versus 2025. This was broadly in line with the visible forward schedule, and also similar to IATA’s December 2025 Outlook, which predicted 4.9% global RPK growth.

IATA reported January 2026 traffic was up 3.8% versus 2025, on capacity up 3.5%. It has not yet reported February figures, but Cirium data shows that actual ASKs flown grew by 5.3% last month.

For March 2026, Cirium’s forward schedule, at the start of the month, indicated the airlines would expand capacity by 5.6%. This figure had already declined slightly compared to the advance March schedule at the start of the year, which showed growth of 6.8%.

Our tracked data, up to and including 22 March 2026, shows that the number of passenger flights grew by just 1.2% over the same period in 2025. Unsurprisingly, the major impact was on Middle East domiciled airlines, which have experienced a 52% decline in flights year-on-year. The region made up just 4% of tracked flights in March 2025, but it has a far larger impact in terms of ASKs, as the airlines tend to fly larger aircraft and serve longer stage lengths than in other regions. It amounts to 10% of global ASKs, based on March 2025 data.

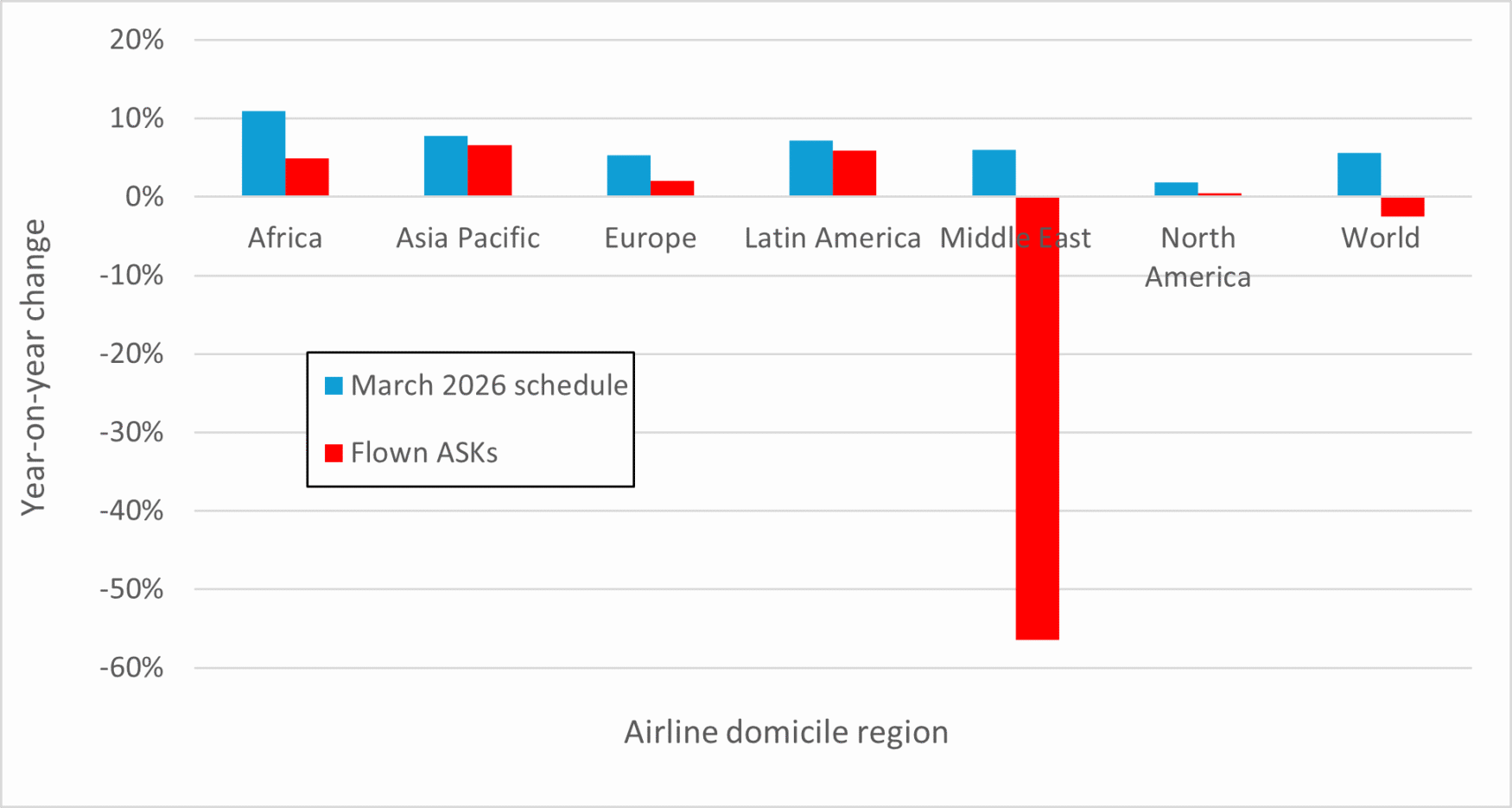

The chart below shows March 2026 flown ASKs, by airline domicile region, compared to March 2025. The 56.5% decline in Middle East airline capacity contributes to a global contraction of 2.5% in the first 22 days of the conflict.

Actual capacity flown 1-22 March 2026, versus planned schedule

Other regions are also impacted, but to a lesser degree, with many airlines cancelling flights to the Gulf states, Saudi Arabia and Israel. Comparing the forward schedule for March with the actual ASK flown provides an indication of the impact. African carriers have seen a roughly 5-6 percentage point hit, with European airlines the second most affected, with flown ASKs up 2%, versus a planned schedule increase of 5.3%. Asian carriers have experienced just a one percent impact, but this obviously varies considerably, with Indian sub-continent airlines most affected. North American airlines have seen a similar effect, with United Airlines noting that suspending its services to Riyadh and Dubai knock about 1% from its ASKs.

Looking further ahead, several airlines have announced that service suspensions to the Middle East will continue into April and May. However, the forward schedule at the time of writing has not changed dramatically. April 2026 currently shows 3.4% year-on-year growth in ASKs, compared to 5.4% immediately before the conflict started. May 2026 has fallen marginally, from 6.6% to 6.3%.

Even if passenger load-factors remain high, with strong demand in other markets stated by several airlines, the conflict has led to an eight percentage-point hit to airline capacity in March. This is before we see any measurable impact from higher jet fuel prices on demand. This level of demand/capacity disruption, if it continues for any length of time, does imply a significant effect on aircraft utilisation rates and fleet plans.