Cirium Ascend Consultancy is trusted by clients across the aviation industry to provide accurate, timely, and insightful aircraft appraisals. The team provides the valuations and analysis the industry relies on to understand the market outlook, evaluate risks and identify opportunities.

Discover the team’s industry reports & market commentaries. Read their latest expert analysis, viewpoints and updates on Thought Cloud.

Team Perspective

Sara Dhariwal, Lead Appraiser – Helicopter & AAM Markets , Cirium Ascend Consultancy

Last week’s Cirium Ascend Consultancy helicopter market webinar examined the key forces shaping today’s rotorcraft market, from fleet growth and replacement cycles to civil‑military production dynamics, oil pricing and delivery trends.

After more than a decade of disruption, the market is showing clear signs of maturity. Long asset lives, disciplined deliveries and an ageing global fleet are supporting stability today, while also underpinning future replacement demand.

Reflecting this shift, Sarah Johnston, In‑House Counsel at SMFL Helicopters, noted that increased stability and a growing number of market participants represent “a very positive development” for the sector. Gabriella Oliveira del Mastro, Fleet Director at PHI, similarly observed that greater stability reflects a more deliberate and mature market approach.

Steady fleet growth, shaped by longevity

Over the past decade, the global civil helicopter fleet has grown at an average rate of around 1.5% per year. Growth slowed briefly in 2020 as the pandemic disrupted deliveries, but has since recovered, with expansion closer to 2% annually in recent years. By the end of 2025, the global fleet reached approximately 24,500 helicopters, representing a net increase of just over 3,200 aircraft.

Fleet growth has been supported less by elevated deliveries and more by persistently low exit rates, with retirements and total losses averaging just over 1% per year. Longevity remains a defining feature of the market, with around 90% of helicopters delivered over the past 30 years still in operation and the average retirement age approaching 40 years. While this durability underpins asset values, it has also resulted in a steadily ageing global fleet.

Replacement demand is building — but slowly

Looking ahead, replacement rather than fleet expansion is expected to be the primary driver of helicopter demand. Cirium estimates that just over 4,000 helicopters could require replacement over the next decade — equivalent to around 70% of the current global fleet. While elevated asset longevity and OEM production constraints have delayed replacement activity, they have also helped restrict supply and support asset values.

As the market evolves, a more mature secondary ecosystem is beginning to form. del Mastro noted that the helicopter sector is starting to adopt attributes long established in fixed‑wing aviation, including structured part‑out activity and lifecycle management. Echoing this, Johnston highlighted the need for stronger and more formalised secondary‑market support, underscoring the role this will play in enhancing capital efficiency and long‑term value preservation.

Civil and military demand: competition for capacity?

A recurring question is whether rising military demand is constraining deliveries into the civil helicopter market. Civil and military variants often share production lines and supply chains, making this a valid concern given the current geopolitical environment.

Historical data suggests OEMs have generally balanced production across both segments over the long term. However, the ongoing deferral of civil replacement into the latter part of this decade risks overlapping with the next anticipated military renewal cycle in the early‑to‑mid 2030s. Should this occur, pressure on production capacity and delivery lead times could intensify.

In parallel, sustained increases in military utilisation could place additional strain on shared supply chains, particularly in parts availability and MRO capacity, with potential knock‑on effects for both civil and military operators.

Oil prices: short‑term volatility versus structural impact

Geopolitical conflict and associated oil‑price volatility have renewed concerns about a potential downturn similar to that experienced in 2014. However, there is currently little evidence to suggest that short‑term price movements alone will materially alter helicopter fleet dynamics.

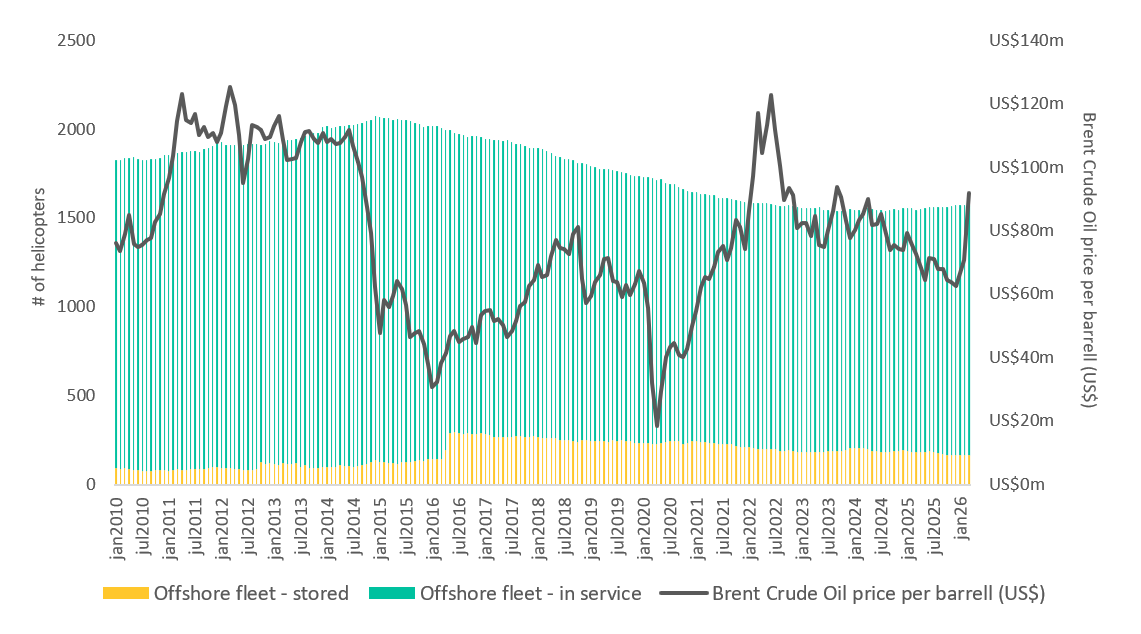

Chart 1: Offshore fleet evolution and crude oil pricing

Source: Cirium Fleets Analyzer / U.S Energy Information Administration EIA

The previous downturn was driven not by volatility, but by a prolonged period of sustained high oil prices, which encouraged aggressive fleet expansion based on assumptions of long‑term demand growth. When prices subsequently fell and remained depressed, the market was left with significant oversupply and prolonged pressure on utilisation and values. By contrast, recent pricing appears to have settled at a more sustainable level, around US$80 per barrel, historically supportive of offshore helicopter operations and a more balanced supply‑demand environment.

While broader macroeconomic risks persist — including inflationary pressures and recessionary concerns that could weigh on values and investment appetite — the key takeaway for the helicopter industry is clear: sustained structural trends matter far more than short‑term volatility.

A maturing helicopter leasing market

The helicopter leasing sector has evolved significantly since its emergence around 15 years ago. Recent consolidation has concentrated a sizeable portion of the global leased fleet among a small number of major international lessors, contributing to greater stability and a more disciplined growth profile.

Growth among established lessors has increasingly been driven by sale‑and‑leaseback transactions, rather than speculative order books, improving alignment with operator demand and reducing risk exposure. While leasing penetration remains lower than in commercial fixed‑wing aviation, there is clear scope for further expansion across multiple mission profiles, including EMS, utility, offshore energy and search‑and‑rescue operations.

Johnston described the sector as “highly dynamic and competitive”, noting that “there remains considerable headroom for additional leasing activity, both globally and across different market segments”.

del Mastro echoed this view, adding that increased competition is a positive development: “Coming from the fixed‑wing sector, where leasing choice is well established, I expect similar trends to continue developing in the rotorcraft market.”

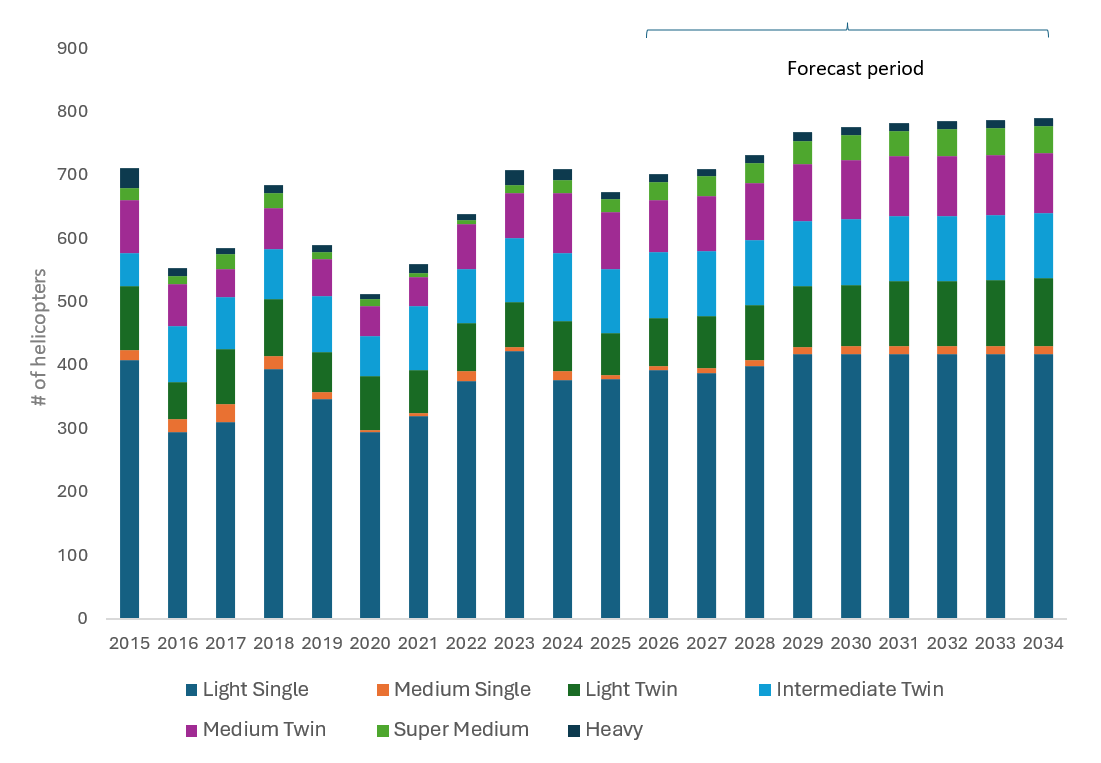

Deliveries and the outlook for the next decade

Following delivery volumes of around 700 aircraft per year in 2023 and 2024, 2025 saw a modest decline, in line with expectations. Over the next decade, Cirium anticipates a gradual recovery, with average fleet growth of approximately 1.4% per year, equating to around 7,500 deliveries. Importantly for investors, more than half of these aircraft are expected to serve replacement demand, representing an addressable market of roughly US$50 billion on a full‑life value basis.

Chart 2: Cirium Helicopter 10-year Fleet Delivery forecast 2025

Source: Cirium 2025 Helicopter Fleet Forecast

While extended lead times and ongoing supply‑chain constraints continue to limit near‑term deliveries, they have also reinforced supply discipline and supported asset values. From an operator and investor perspective, predictability and capital efficiency remain key priorities. del Mastro noted, “greater predictability on when aircraft can enter service is critical, alongside improved capital efficiency over the life of the aircraft and better access to competitive lease and debt financing”. She added that more predictable certification, STC processes and OEM production schedules would further enhance lifecycle optionality and returns.

New technology: complementary rather than disruptive

Emerging technologies — including autonomous helicopters, drones and eVTOL platforms — continue to attract attention. While progress is being made, their near‑term impact on the traditional helicopter market is expected to be complementary rather than disruptive.

Initial applications are likely in cargo, logistics and unmanned operations, where certification and operational barriers are lower. More complex missions will take longer to materialise, particularly where energy density, safety and regulation remain limiting factors.

A resilient market, well set up for gradual change

The helicopter sector today is defined by stability and resilience rather than rapid expansion. Long asset lives, disciplined production, diversified missions and a more mature leasing ecosystem have reduced volatility and helped stabilise values.

While supply‑chain constraints and geopolitical uncertainty remain, the overarching outlook is one of measured growth, delayed but unavoidable replacement demand, and gradual evolution rather than disruption. For operators, investors and OEMs alike, predictability, transparency and disciplined planning will be critical as we move into the next decade.

Watch the webinar on-demand

To access the presentation and watch Sara, Gabriela and Sarah’s full discussion, register to watch.