Bookmark this page and scroll down to see the latest updates from Ascend by Cirium analysts and consultants, experts who deliver powerful analysis, commentaries and projections to airlines, aircraft build and maintenance companies, financial institutions, insurers and non-banking financiers.

Meet the Ascend by Cirium Team

August 25, 2021

Why Airbus is gearing up to re-enter the widebody factory freighter market

By Max Kingsley-Jones, Senior Consultant at Ascend by Cirium

Airbus looks finally ready to launch a full-on assault on the air-cargo sector with a portfolio of converted and factory-build freighters now crystallizing in its armory.

A factory-freighter A350 derivative looks set to debut in 2025, following the recent green light from the Airbus board. Meanwhile the A320ceo family converted-freighter market is finally getting into its stride as feedstock availability and market values are now aligning, along with demand. The A330P2F programme is also building momentum for similar reasons.

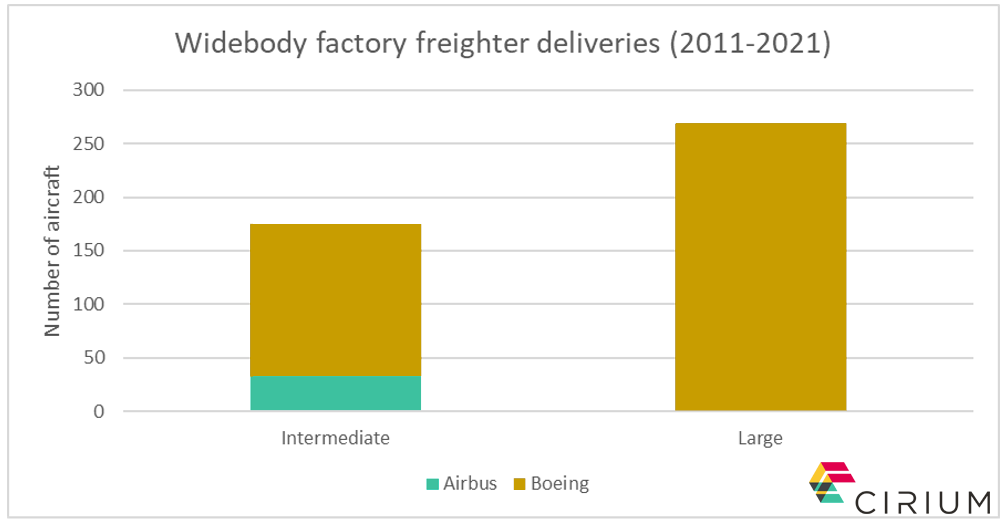

But the strategy around a factory offering in the widebody sector is the crucial one for Airbus. After relatively poor sales of the A330-200F, which entered service in 2010 but completed just 38 deliveries, Airbus knows it must establish a solid bridgehead in the widebody cargo sector with a new-build freighter to challenge Boeing’s dominance.

Over the last decade, Boeing has delivered 269 new large widebody freighters (171 777-200LRFs and 98 747-8Fs) as well as 142 767s in the intermediate class, for a total of 411 aircraft. To highlight the size of the problem for Airbus, its comparative tally for factory freighter deliveries was just 33 of those aforementioned A330-200Fs.

It has long been Toulouse’s stated intention to address this deficit, and the time is now right to do so. Airbus has the engineering resources available to create a competitive product based on the A350 platform, just as a distracted Boeing must also nail its widebody freighter succession plan. New environmental legislation around engines will force production of the current 777F and 767F to end by 2028.

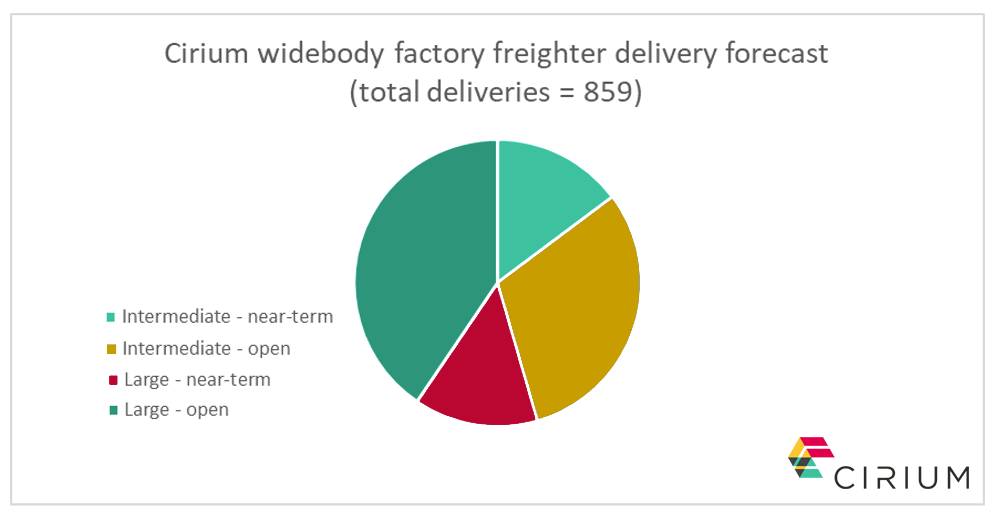

Ascend by Cirium forecasts that the long-term market for large widebody freighters over which Airbus and Boeing will compete is worth around $75 billion.

The 2020 Cirium Fleet Forecast sees a market for almost 470 new deliveries in the category over the next 20 years. Combined with the intermediate widebody category, Ascend by Cirium forecasts a total of around 860 aircraft worth over $111 billion.

While near-term demand will be met by the in-production Boeing products, we forecast there is still open market for some 600 new widebody freighter deliveries. And Airbus should be targeting at least a fifth of this market – or 120 aircraft. What Boeing decides to do – be it around the 777X, a re-engined 767 or a 787F – will be fascinating to see.

August 20, 2021

Aviation and the Tokyo 2020 Olympic Games

By Herman Tse, Aviation analyst at Ascend by Cirium

2020 was an extraordinary year with many challenges. The World’s largest global sporting event, the 2020 Summer Olympics, had to be postponed due to Covid-19. Fortunately though, the event was recently completed successfully in Japan some 364 days late. Since the Games were largely held behind closed doors, the expected economic benefits typically associated with hosting the games did not materialize. The financial hit is estimated up to US$1.4 billion in the host city. Obviously, air travel demand was not as high as originally expected. However, there were still tens of thousands of overseas athletes, officials, support staff and journalists traveling to Japan from different countries, albeit no spectators were permitted in most of the venues (limited spectators were allowed in some events held outside Tokyo). With this in mind, did the event change travel demand patterns in Japan significantly?

Typically athletes and staff were required to quarantine in hotel or the athlete village upon arrival, and then leave Japan within 48 hours of completing their events. With this arrangement, there was an upward trend in arrival seat capacity since the beginning of July.

Two peaks were observed between the opening and closing ceremony, during which the main events were held. The peak of seat capacity is remarkably similar to that seen in the Japan Golden Week earlier this year.

The trend of arrival seats tracked in Japan

International seat capacity accounted for just 13% of overall Japanese airline seat capacity on average prior to and during the Games, almost the same as June 2021. Domestic travel remains the major source of demand in Japan. Like past Olympics, some of the events were held outside the host city in the same country. It is no surprise that Tokyo Haneda (HND) and Narita (NRT) were the busiest airports as Tokyo was the host city. New Chitose (CTS) in Sapporo and Naha (OKA) in Okinawa overtook Fukuoka (FUK) and Kansai (KIX) airports and ranked third and fourth. These two cities hosted some events and even allowed spectators in the venues which attracted more locals to travel.

Top 10 busiest airports in Japan (15 July 2021-14 August 2021)

Undoubtedly, 2020 was a difficult year and 2021 remains so. Globally we have all been learning how to be creative and flexible in the increasingly complex working and domestic environment necessitated by Covid. Tokyo showed the world that it is possible to organise a large sporting event despite the restrictions necessary due to the pandemic.

The 2024 Olympics will be held in Paris, France (hopefully) under a post-pandemic scenario. Once again we should be able to see another Olympics full of spectators cheering for their athletes. The event focus will largely be in Paris and air travel demand is expected to be high. Capacity may be insufficient to cope with the demand for the event period. Airports and airlines will once again need to offer creative solutions to provide travel options for their customers (for example flight-to-train/coach connection, 2nd-tier airport connection, etc.). With some events scheduled to be held in Lille, Marseille, Bordeaux, Nantes and even in Tahiti, there will be much opportunity for airlines to schedule appropriate networks and once again benefit from the enhanced demand such global sporting events create.

August 10, 2021

Lessor Idle Inventory – Where Next?

By Rob Morris, Global Head of Consultancy at Ascend by Cirium

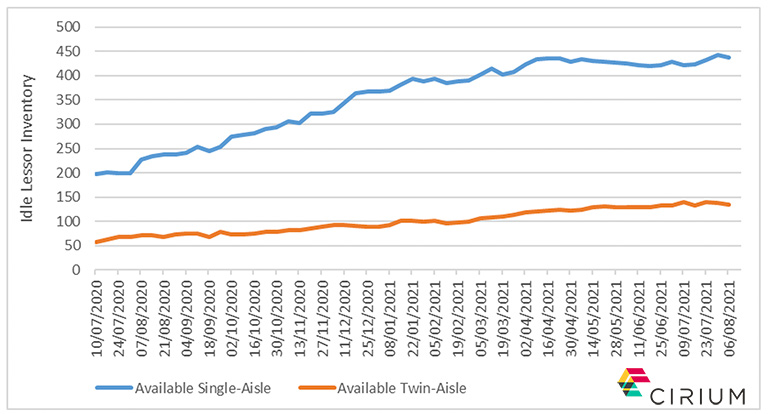

Back in the middle of 2020, in the early days of the pandemic, lessor inventory – defined as aircraft recorded in Cirium’s fleets data as returned to an operating lessor and with no future commitment identified – stood at just under 200 single-aisle and around 60 twin-aisle aircraft. Amongst that single-aisle inventory were some 91 A320 family and 46 737NG/Max family aircraft. Predominant amongst twin-aisle aircraft were 19 A330-200s and 13 777-200ERs. At the same time the data recorded a further 81 single-aisles which had future events identified – including 46 future leases – and 43 further twin-aisles.

Given the demand environment that has sustained since that time, and also the high level of leased aircraft within airline fleets, it is not surprising to see that the inventory increased weekly on an almost linear basis so that by mid-April 2021 it had more than doubled to 435 single-aisles and 123 twin-aisles, again dominated by more than 230 A320 family, 141 737NG/Max family, 31 A330-200s and 30 777s. That’s the bad news.

The better news is that the inventory in mid-April also included some 110 single-aisles which had a future gainful fate identified – 75 new leases and 35 P2F conversions. The majority of those new leases would have been contracted during the pandemic, providing ample evidence that lessors are still able to place aircraft even in the current depressed demand dynamic.

The even better news is that since mid-April the inventory appears to have stabilised and latest numbers (from 6 August) are very similar – 437 unplaced single-aisle and 134 twin-aisle – as is the mix of types and variants.

There are additionally some 63 and 36 single-aisles respectively committed to new leases and P2F conversion, so contracts are still being agreed and idle aircraft continue to be prepared for new gainful employment.

However, as we head through the 2021 Summer season (such as it is), the outlook is potentially set to become even more challenging. The fleets data includes some 400 scheduled lease expiries for the remainder of 2021. Given that Cirium’s researchers for now only include known expiries, the likely actual expiries could be as many as double that. And likewise in 2022 where for now 350 expiries are recorded, so the total again could be as high as 700.

Can new lease placements keep up, or will the idle inventory inevitably start to increase once more? Again the data can give us a steer, since it shows that historically lessors were placing around 40-60 single-aisle aircraft into new leases every month (on a rolling 12-month average basis). However, that pace of placement has fallen to around 20-30 per month today. Clearly at that new lower rate, returns will exceed placements and inventory must inevitably increase.

There does remain one wild card which we haven’t covered – aircraft part-outs. The inventory today includes only 32 single-aisles which are earmarked for retirement and part-out. Through 2020 and into 2021 the pace of part-out has been fundamentally lower than 2019 as demand for used material to support operation and MRO has reduced. As demand recovers, so will part-out volumes and that in itself will help to reduce the growth of (or even the absolute level of) lessor idle inventory.

In the long-term, as lease placement levels and part-out volumes both recover, inventory will reduce. But for now and through the remainder of 2021 at least, we continue to watch closely and expect the risk of further increase to outweigh the probability of inventory reduction.

August 4, 2021

Can a strong domestic market be an airline’s saviour?

By Joanna Lu, Head of Consultancy Asia at Ascend by Cirium

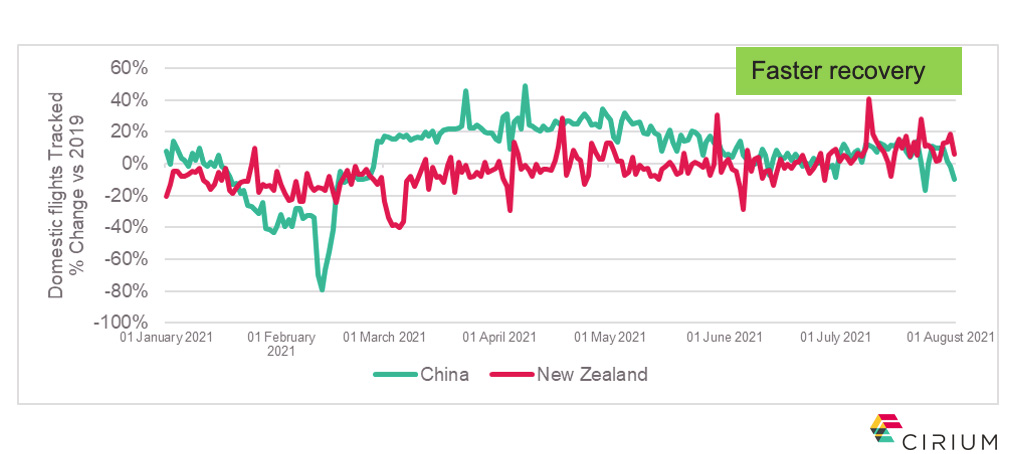

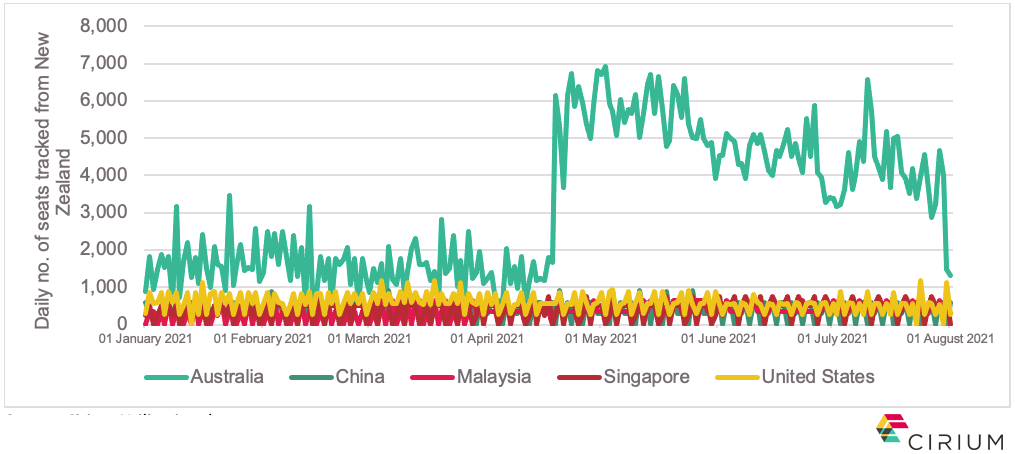

New Zealand’s government has just suspended the quarantine-free ‘travel bubble’ with Australia for the next eight weeks, as the latter battles a surge in COVID-19 infections. On 23 July, New South Wales reported a record-breaking 136 new infections. New Zealand has contained the virus effectively over the last couple of months and reported no new cases of COVID-19 on the same day. Low case rate drives expectation of recovery and increasing demand for travel. Active flight activities were the main reason why Ascend by Cirium has recognized New Zealand as one of the “faster recovery” countries, together with China, in terms of flights tracked versus 2019 in domestic markets during the last couple of months.

New Zealand’s approach to resumption of international flights has been cautious and the government made it quite clear that no assurances of a return to normal anytime soon, announced no multi-step “pathway out”, and put forward no timeline for re-opening borders even to vaccinated travellers. This contrasts with most governments around the world who often promote “return to normal” in rhetoric, although still cautious in actions in opening borders.

Local residents in New Zealand seem to advocate their government’s approach in protecting the border. In a government survey more than 90% of New Zealanders do not expect life to return to “normal” even after they are vaccinated. Australia has been the only major international market open for New Zealand since the travel bubble was launched in April. The loss of this market means that New Zealand is once again back to the situation where the domestic market remains the majority revenue source for airlines.

As the largest airline in that market, Air New Zealand announced a loss before other significant items and taxation of $185 million for the six-month period ended 31 December 2020, reflecting the considerable impact of the COVID-19 pandemic on the airline. This compares to earnings before other significant items and taxation of $198 million for the same period in 2019. During the six-month period, focus has already been made on maintaining strong performance in domestic and cargo businesses and cost discipline. However, the continuation of significant restrictions on international travel to and from New Zealand drove the significant decline in the airline’s operating revenue.

Clearly there will remain significant challenges for the airline’s financial performance, even though it is benefiting from a strong domestic market. The latest statistics show that Air New Zealand carried 787,000 domestic passengers in June 2021 at a load factor of 78.3%.

In June 2019 passenger numbers were 1,025,000 at 81.7% load factor, so only 25% or so down over pre-pandemic volumes. The airline is still guiding for a significant loss in 2021 again, as there remains a large degree of uncertainty surrounding the lifting of travel restrictions and the subsequent level of international demand, despite both this strong domestic and also international cargo performance. Like most global airlines, while international travel restrictions remain in place a strong domestic market is critical to underpin at least some element of financial performance. Flexible fleet and network strategy can drive some modicum of success in those markets until international markets can once again reopen and the new ‘normal’ returns.

August 3, 2021

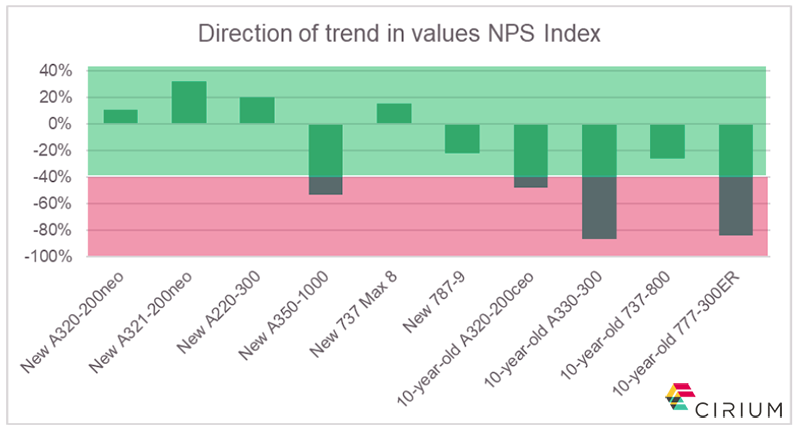

Commercial Aircraft Market Sentiment Index, July 2021

By David Griffin, Valuations Consultant, ISTAT appraiser at Ascend by Cirium

In April, Ascend by Cirium launched the Commercial Aircraft Market Sentiment Index. The Index is published monthly and tracks market sentiment and trends of values, lease rates through a survey of key market stakeholders, including lessors, banks, OEMs, part-out shops, airlines and brokers. From our target of 100 participants we are delighted to receive almost 60% participation so far.

With our success to date we are keen to broaden our sample base further so if you would like to participate in future surveys on a monthly basis where we ask three simple questions connected with commercial aircraft values and lease rates, please contact our team.

This month we return to lease rates, where we will analyse the change in market attitude since May. This is the first edition where we have prior lease rate data to benchmark against and thus we can begin to track the evolution of sentiment.

We continue to use an NPS like Index for the trend – estimated as the number of respondents replying ’too high’ or ‘trending up’ minus those replying ‘too low’ or ‘trending down’, divided by the total sample response to that question. Scores in the 40% to -40% range broadly indicate stability, those below -40% can be considered to indicate a very strong negative trend in values and those above 40% indicate a strong positive trend.

This month the market is telling us that it sees positive movements on lease rates for new technology single-aisle aircraft, although used aircraft and the A350-1000 remain under pressure for now.

However, the market also tells us that it sees increasing stability in lease rates for all types, and indeed compared to the last survey this is clearly evident and illustrated by comparison to market sentiment just two months ago.

Following prior surveys we noted that there appeared slightly more optimism for lease rates than values and now that we have begun to trend the lease rate data we see that holds true. As we enter month 17 of the COVID-19 pandemic it is reassuring to see two consecutive months with increased optimism from the market. This accords with many of the market indicators we track on a weekly basis, so it does clearly seem that better times are ahead. In that context we believe that single-aisle lease rates have bottomed out, although for twin-aisles some types still remain on watch.

To finish the survey this month we queried participants on opinion of future programs at the two major OEMs, asking both what will they develop next and what should they develop next.

Unsurprisingly the majority of respondents believe that the next program in the works at Airbus is an A350 freighter (which of course was soft launched with authority to offer being announced just a few days after we closed the survey), but interestingly it is the second least popular choice when asked what Airbus should do. A stretch of the A321neo is the most popular choice followed by a stretch of the A220 along with a developing a new single aisle aircraft. Clearly many feel that Airbus should exploit the opportunity posed by the A321neo’s current market position to further consolidate the present market share lead.

Switching to Boeing, unlike Airbus the market strongly believes that they should not focus on derivatives, rather moving to a clean sheet design either in the Middle of the Market or a smaller aircraft to replace the Max. Further upgrades to the 787 or re-engining the 767 are not seen as attractive options.

Thank you for your participation, next month’s survey which will return to market values will be issued on 11 August and if you would like to participate please contact one of the team.

July 27, 2021

By Chris Seymour, Head of Market Analysis, Ascend by Cirium

Freight conversions to hit a record high

Analysis of Cirium Fleets Analyzer data shows that 57 passenger jets were converted to freighters in the first six months of 2021. This is approaching the entire total of 70 conversions done in 2020. With additional conversion slots coming online, 2021 could see a doubling to a record 140 conversions, beating the previous high of 107 in both 2007 and 1995.

This boom in activity is being driven by a combination of factors. Underlying demand for air cargo is strong, especially in the e-commerce sector, boosted by increasing online sales, both generally and especially during COVID-19 lockdowns. Available supply of feedstock has risen, as the passenger market continues to suffer, and in line with this, values of passenger aircraft have fallen, making the total conversion package more attractive. In addition, the increase in newer generation conversion programmes such as the Airbus A321, A330 and Boeing 737-800 is allowing replacement by these more fuel, efficient types.

Announced orders for conversions have passed 160 this year, well ahead of the 102 recorded in 2020 and pushing the conversion backlog above 330.

Looking at the orders placed, there is an almost equal split between lessors and airlines. Interestingly, only 16 of the orders have come directly from the integrator/e-commerce market, although many of those converted will ultimately be operated on behalf of these companies. Lessors have a higher share of the narrowbody conversion backlog (78%) and are the key players in the growing A321 and 737-800 markets. GECAS is also launch customer for the new 777-300ER conversion programme with IAI Bedek.

There are now 13 aircraft types and series with available conversions, and two (A320 and 777-300ER) in development. Nine companies or joint ventures have supplemental type certificates (STCs) and active programmes, while two others (C3 and Sine Draco) have aircraft in conversion as they seek STCs. The largest backlogs are with Boeing, AEI, IAI Bedek, Precision and EFW.

Current conversions backlog – leading types

With the increase in backlog, the STC holders are increasing slot capacity, at their own facilities and/or at MRO third parties. Twenty different entities are involved at 25 global locations, with two more contracted to start conversions. China has become an important centre for conversions with a third of 2021 activity occurring at Gameco, STAECO, HAECO and others. About 30% of conversions are being done in North America, notably in Florida, with 16% at IAI in Tel Aviv. Other activity includes 767s in Singapore and small numbers conducted in Europe and Latin America, with recent announcements of new activity to start in Italy and Korea.

Conversions of narrowbodies make up some 60% of the backlog, led by the 737-800 with almost 120. The 757 has seen a recent renaissance with over 30 committed, but is now being overtaken by the A321. The 767s lead the widebodies and make up 25% of the whole backlog, with demand from airlines, Amazon, DHL and the China market. DHL is also a key player in the new A330 programme and has recently said it plans to order 11 more conversions.

With 2022 likely to see a further increase to around 160 conversions, some programmes are already sold out until 2023. The question is whether this higher level of supply will be maintained beyond 2022, or if it is just a short-term boom, as the long-term 20-year forecast is for an average of just under 100 conversions per year.

Learn more about Ascend by Cirium and Cirium Air Cargo solutions.

July 20, 2021

“Hot or cold” summer in Southeast Asia in 2021?

By Herman Tse, Aviation analyst at Ascend by Cirium

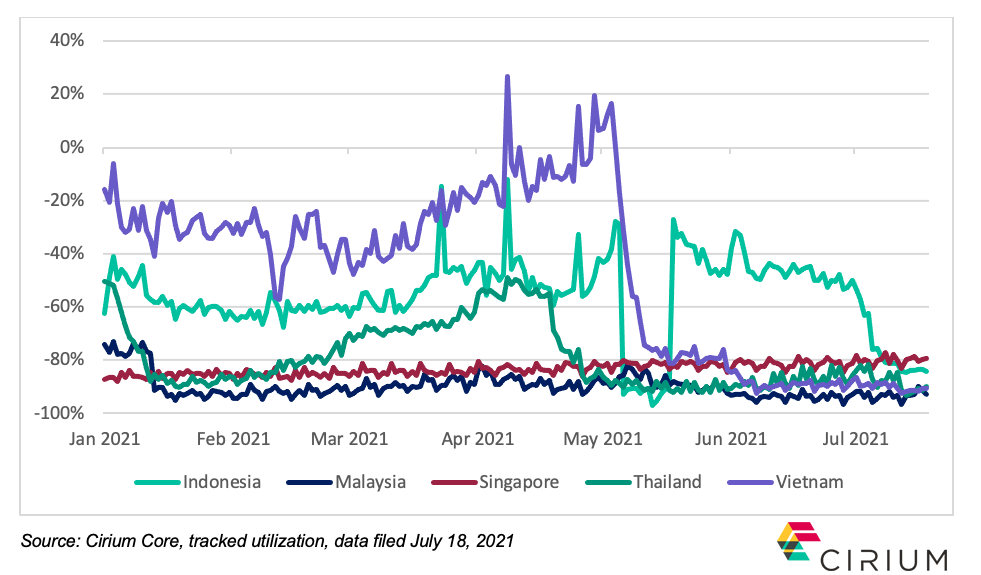

Summer is a traditional peak season for airline passenger markets, particularly in Southeast Asia. Singapore, Thailand and Vietnam are popular tourist destinations in the region.

In 2020, airlines experienced a “cold” summer due to the pandemic. Passenger demand declined significantly due to border restrictions and quarantine requirements for Covid-19 infection control measures. With COVID-19 vaccines now being distributed around the globe, can we expect a “hot” summer in Southeast Asia in 2021?

In Singapore, air travel demand has remained weak since the beginning of the pandemic, as the country lacks domestic traffic. The government has held talks with many states including, Hong Kong, Taiwan, Australia, New Zealand and Brunei as it sought bilateral travel bubbles. Unfortunately though, these either remain on hold or suspended due to the most recent outbreak in Singapore.

Thailand is another country dealing with a high number of cases in recent months. Several domestic and international routes from Bangkok have been suspended by Thai Airways until September at least to comply with the tightened movement restrictions imposed by the government. Although the ‘sand box’ of Koh Samui remains open to international tourists, the president of the Tourism Association of Koh Samui admitted that there will not be high number of international travellers in the third quarter based on the latest pandemic situation in Thailand.

Vietnam was one of the fastest recovering countries in Asia before May. Seat capacity had already returned to 2019 levels.

However, as daily confirmed cases of COVID-19 then began to increase again and peaked in July, with more than 2,000 daily cases. Seat capacity is thus unlikely to increase significantly in summer, albeit Vietnam Airlines is poised to resume operating to Australia, Japan and Thailand in July. Indonesia and Malaysia also continue to suffer from high numbers of daily confirmed cases. The airline industry continues its weak seat capacity trend.

The spread of Covid-19 can be as quick as overnight and it takes weeks or even months to control each wave of infection. Governments in Southeast Asia remain very cautious in reopening borders or lifting quarantine requirements. Consequently, passenger demand and capacity will continue to fluctuate until mass vaccination is completed within each country. Vaccination rates in most Southeast Asian countries remain low, except Singapore.

Source: Official data collated by Our World in Data, data filed July 18, 2021

Given that Asian markets are fragmented, passenger demand this summer is not expected to return to anywhere close to pre-Covid level in this peak season. Likely, It will be another “cold” summer in Southeast Asia.

July 15, 2021

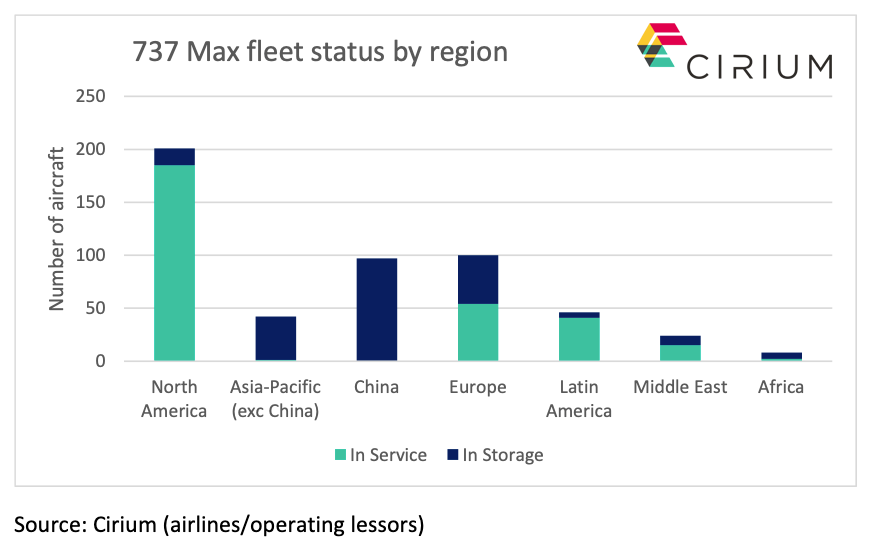

How China’s Max approval is crucial to restoring Boeing’s delivery share

By Max Kingsley-Jones, Senior Consultant at Ascend by Cirium

Deliveries of around 100 pre-built aircraft remain in limbo awaiting decision on ungrounding.

News of potential progress in returning the 737 Max to service in China is a crucial development for Boeing as it works to claw back single-aisle delivery market share and the nation’s operators account for a third of the approximately 290 pre-built aircraft awaiting delivery.

The type effectively remains grounded throughout Asia-Pacific despite approvals having progressively been secured across the Americas, Europe and the Middle East. Cirium data identifies that 58% of the global airline fleet of 518 delivered aircraft is now flying. But only one of the 139 Max aircraft with Asia-Pacific operators is in service (operated by Kazakh carrier SCAT).

Details of the expected timeline around China’s ungrounding have been scant, with Boeing officially indicating that it expects a decision before year-end. However, recent news reports suggest there may be some early progress, with Chinese officials having “signalled” their openness to recertification and Boeing potentially sending a team to China later this month.

At the time of the March 2019 grounding China had the single largest Max fleet (97 aircraft) and that total still represents around 45% of all grounded Max aircraft. And Cirium data indicates that some 101 of the 291 undelivered Max aircraft in storage that flew before August 2020 are destined for Chinese airlines (although several are thought to have been re-allocated to United Airlines).

Cirium data shows that the Asia-Pacific operators account for 52% of the pre-built undelivered Max aircraft. Other countries in the region may be awaiting China’s decision on the Max return-to-flight, although the Covid-19 crisis continues to dampen demand in the Asia-Pacific which will have limited the appetite for some operators to recommence deliveries.

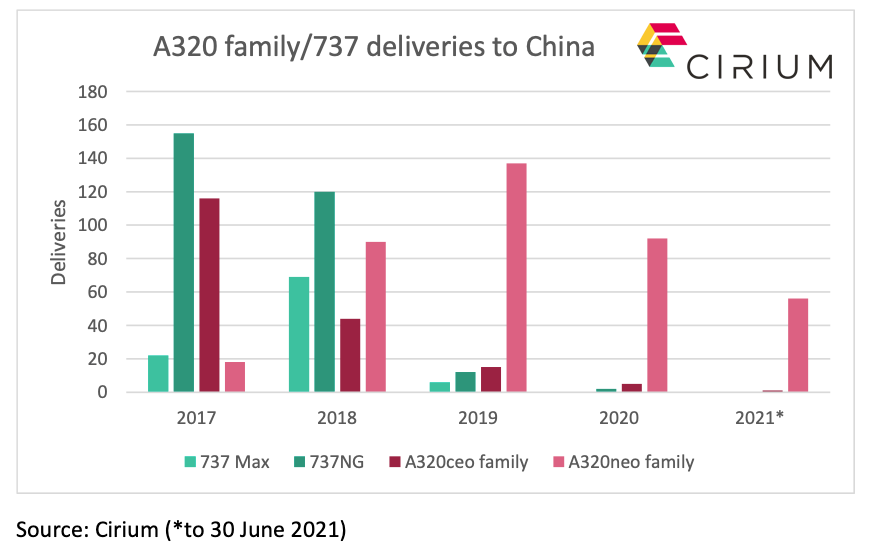

But until things change for the Max in China and the wider region, Airbus is experiencing an unobstructed path to market-share dominance in single-aisle deliveries to Asia-Pacific.

In the two years prior to the March 2019 grounding, Airbus trailed Boeing in China’s single-aisle sector, delivering 43% and 42% of all single-aisles in 2017 and 2018 respectively. Overall delivery volumes are significantly down due to Covid, but since the Max grounding, Airbus has delivered 286 A320 family aircraft to China against just 12 737s from Boeing – the final batch of Chinese 737NGs.

Airbus had a slight delivery-share advantage in the entire Asia-Pacific commercial single-aisle sector in the years immediately prior to the grounding and has had the market almost entirely to itself since. Cirium data shows it has delivered 612 A320 family aircraft to the region between 2019 and 2021 (year to date), against 30 737 Max/NGs.

Approval by China’s CAAC to unground the Max will clear the path not only for it to return to the skies but will also unblock the delivery pipeline to Boeing’s key overseas market. It cannot come soon enough for Seattle. That Boeing continues to roll out and fly new Max aircraft for Chinese customers signals that it anticipates a resolution is potentially close.

July 7, 2021

Are Lessors Starting to Trade Aircraft Amongst Themselves Again?

By Rob Morris, Global Head of Consultancy at Ascend by Cirium

Late last week Cirium Dashboard reported that CDB Aviation acquired three 737 Max 8s with leases attached from DAE. These specific aircraft were acquired by DAE late last year via purchase and leaseback (PLB) on delivery from American Airlines. Our Fleets data records 17 such PLBs, so DAE still retains 14 of those in addition to four Max aircraft acquired from Gol pre-grounding and another 15 which they recently ordered directly from Boeing. DAE also announced plans to sell a further nine other aircraft in 2021. But do these deals (and other similar trades we are hearing about at Ascend by Cirium) signal the start of a resurgence of lessors trading aircraft between themselves with lease attached?

The operating leasing model relies on aircraft trading, both to manage concentration in asset and credit terms, and also to drive returns above those available from pure leasing. In this context, an average of more than 650 aircraft were traded between lessors with leases attached annually in each of the five complete years between 2015 and 2019.

As illustrated, the majority were liquid single-aisle types where almost 200 acquiring parties were recorded in the database. Clearly, investor demand for such assets was strong and driving a vibrant market.

As we all know that came to a grinding halt in 2020. Less than 300 aircraft were traded last year and the majority of those were deals agreed prior to the onset of COVID-19, closing largely in the first quarter but then in dribs and drabs through the remainder of the year. Where once we were seeing an average of 50 aircraft traded with leases attached on a monthly basis, we saw an average of 22 such deals last year. To date in 2021, even allowing for some element of data lag in the database, we are down to 11 per month. So to answer my question, these deals are not so much signaling a resurgence, but perhaps a stirring of the market.

However, as the market stirs it is interesting to observe the asset mix of aircraft trading this year. More than 50% of the trades in 2021 to date have been relatively late-model (by which I mean less than 10 year-old) 737NG or A320ceo family aircraft. Clearly there is still appetite for such aircraft at the right price and with the right lease attached. The next largest portion are almost-new 737 Max or A320neo family aircraft, most often being sold by lessors to financing partners with the lessors then continuing to manage the aircraft on the new owners’ behalf.

Despite last week’s news, trading volumes do appear to remain down for now. But I am sure as the market recovers, so the trading market will also recover and we will see increasing numbers of sales with leases attached as investor appetite remains as strong as ever.

June 30, 2021

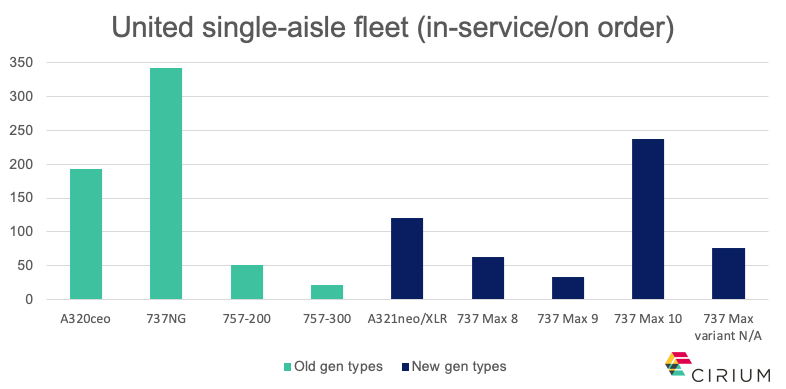

Huge United order highlights appeal of mixing single-aisle types

By Max Kingsley-Jones, Senior Consultant at Ascend by Cirium

United’s giant single-aisle order provides a crucial boost for the sales status of the 737 Max 10 but also underlines the appeal of the A321neo’s capabilities in the narrowbody arena.

The two largest new-gen single-aisles will join United’s fleet in 2023 and are key to the US carrier increasing the average gauge of its narrowbody operations by a third over the next five years while reducing its cost per available-seat-mile by 8%.

The airline has hiked its Max 10 order by 150 to at least 238 aircraft, making United by far the largest customer for the biggest 737. The deal included 50 737-8s, taking its total Max orders to 410 (including 76 where the variant has not been identified), with the 737-10 set to be the cornerstone of its future single-aisle fleet.

Boeing does not generally publish order details by variant, but Cirium data identifies a total of 581 orders for the Max 10, which makes the 204-seater the second most popular Max variant after the Max 8. Cirium data shows it has a 17% share of the Max orderbook where a variant selection has been identified.

United signed for another 70 A321neos to add to its 2019 order for 50 A321XLRs. While it is not unusual for major customers to split big fleet orders between Airbus and Boeing, there is clearly a niche that the very capable A321neo series can fulfil in United’s network despite its huge Max commitment.

United will use the slightly larger A321neo at slot-constrained airports such as Newark and San Francisco, with United CEO Scott Kirby saying its “extra seats are going to be very important” to future growth plans. The airline ordered the A321XLR in 2019 for delivery from 2024 as replacements for older aircraft on intercontinental services and to expand transatlantic routes.

Although the airline was an early customer for the Max 9, it subsequently switched 100 orders to the Max 10 and Cirium data indicates its orderbook stands at 33 aircraft, of which 30 have been delivered (although more may be taken up from the 76 unknown-variant order batch).

The Max 9, which has lower seating capacity than the Max 10 but slightly greater range, has been marginalised in the Max line-up by its new larger sister and accounts for less than 5% (168 orders) of total orders where Cirium has identified the variant.

United operates a large fleet of old-generation A320 family and 737 models (over 530 aircraft included stored), as well as some 70 757-200s and -300s. The new orders will replace some of the existing A320/737s and its 51 757-200s, but a decision is yet to be taken on a successor for its 234-seat -300s.

This latest re-equipment deal is about upscaling, but there may eventually be a need to for a smaller aircraft to replace capacity at the bottom of United’s single-aisle fleet. United has indicated that the Max 7 could be a candidate. The Airbus A220 is another possible option – and had earlier been rumoured to be part of this latest order – but Kirby said that the airline was not currently in the market for “100 to 130” seaters. Ultimately it will depend on whether the airline identifies the need for a smaller outlier in its fleet or decides to continue with its upgauging strategy.

June 29, 2021

Commercial Aircraft Market Sentiment Index, June 2021

By David Griffin, Valuations Consultant, ISTAT appraiser at Ascend by Cirium

In April Ascend by Cirium recently launched our Commercial Aircraft Market Sentiment Index. The Index is published monthly and tracks market sentiment on values, lease rates and trends through a survey of key market stakeholders, including lessors, banks, OEMs, part-out shops, airlines and brokers. From our target of 100 participants we are delighted to receive almost 60% participation so far.

We are keen to broaden our sample base further so if you would like to participate in future surveys, which we envisage will run on a monthly basis and will ask three simple questions connected with commercial aircraft values and lease rates, please contact one of our team.

Meantime, we are pleased to report the outcome of the inaugural survey.

This month we return to values, where we will analyse the change in market attitude since April. This is the first edition where we have prior data to benchmark against and thus we can begin to track the evolution of sentiment in the commercial space.

As per last month, we continue to use an NPS Index for the value trend – estimated as the number of respondents replying ’Too high’ or ‘trending up’ minus those replying ‘too low’ or ‘trending down’, divided by the total sample response to that question. Scores in the 40% to -40% range broadly indicate stability, those below -40% can be considered to indicate a very strong negative trend in values and those above 40% indicate a strong positive trend. Thus, it is clear from the analysis below that the market sees continued negative pressure on all widebody values, but some positive pressure on new technology single-aisle aircraft.

The four positive aircraft illustrated below are the same as in last month’s lease analysis.

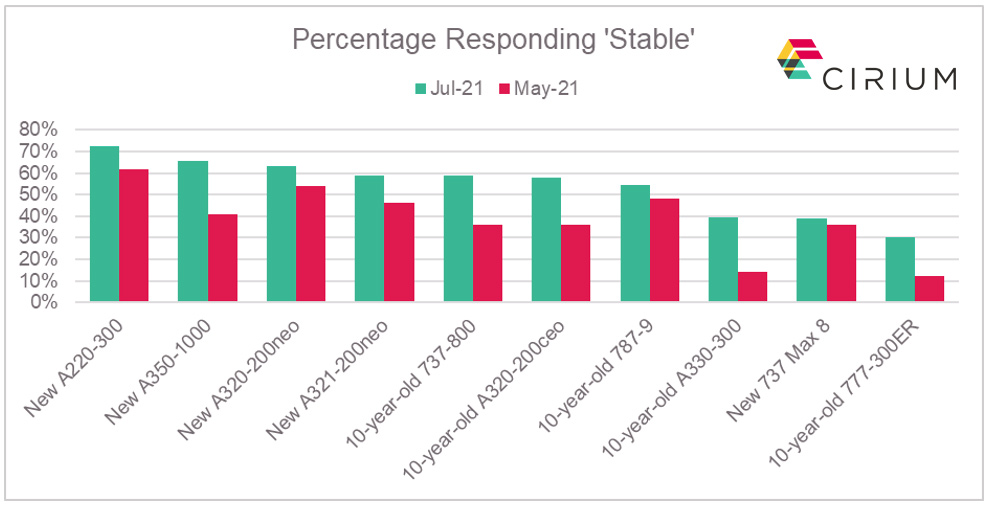

Looking at the stability measure, the percentage considering each type ‘stable’ is shown below. Contrasting the sentiment from this month versus April it is evident that there is some increased positivity in the market. This is particularly evident for used aircraft, with three of the four types seeing a substantial increase in ‘stability’. The remaining aircraft, the 737-800, only saw a slight decrease since April.

Although the twin-aisle market remains extremely constrained due to continued travel restrictions it is interesting to note that all widebody types have a stronger stability index than in April.

Following on from last month’s question covering stored aircraft, this month we focused on retirements.

Over the ten complete years 2010-2019, the Cirium fleets database records an average of 380 commercial single-aisle jet retirements (part-out / PWFU) annually. In 2020 this declined to around 280. So we asked participants what quantum of retirements they expect in 2021. The results appear less bullish than last months stored aircraft with more than 45% of respondents expecting less than 350 retirements. This seems consistent with current data where year to date we have less than 100 single-aisle aircraft parted-out.

Turning to twin-aisles, over the ten complete years 2010-2019 the Cirium fleets’ database records an average of 160 commercial twin-aisle jet retirements (part-out / PWFU) annually. In 2020 this total was still around 160. 75% of participants see an increase over 2020 and the long term average, predicting greater than 160 retirements in the year. If this prediction is to be achieved, we will need to see a significant increase in the pace, since year to date in 2021 we have recorded only 33 twin-aisle retirements / part-outs.

Thank you for your participation. Next month’s survey (which will return to market lease rates as we seek to build a trend data set) will be issued on 14 July and if you would like to participate please contact one of the team.

June 23, 2021

Boeing’s bloating 787 stockpile

By Max Kingsley-Jones, Senior Consultant at Ascend by Cirium

News that Boeing has completed delivery of a 787 after a five-week hiatus raised false hopes that the OEM was poised to resume shipments of the Dreamliner. Unfortunately, that hand-over does not yet signal a resolution to the ongoing suspension of 787 deliveries, which has dogged the programme on and off since October 2020 due to fuselage defects.

Boeing had briefly resumed 787 deliveries in April/May but voluntarily halted shipments as the Federal Aviation Administration sought more data before approving the company’s inspection regime. The single 787 delivered in June was an Everett-built -9 for Turkish Airlines which received its airworthiness certificate in 2020 before the initial suspension, but hand-over had reportedly been delayed at the airline’s request for inspections to be completed.

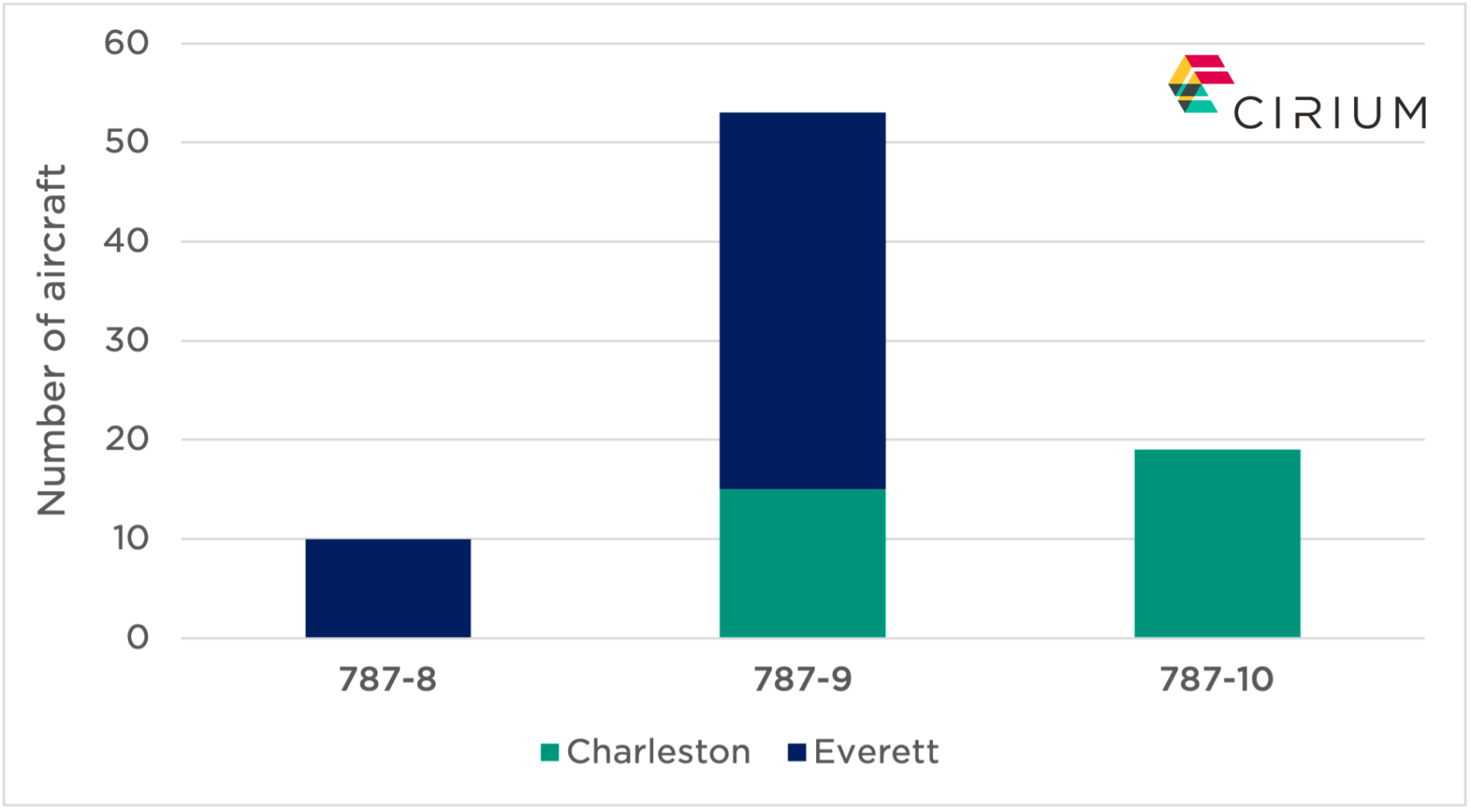

The hold-up has resulted in just 14 787 deliveries since November 2020 – two in March, nine in April, two in May and one in June. Production continues at a rate of five a month and at least three new 787s flew in May and four in June, which perhaps signals Boeing’s expectation that the issue will soon be resolved. But this is also creating a ballooning backlog of undelivered airframes. Ascend by Cirium has identified 82 787s that have been built and flown but remain to be delivered. This inventory includes 51 that flew in 2020, 27 in 2021 and four that took to the air in 2019.

Although 787 production in Everett, Washington has now ended, Cirium data identifies 48 aircraft built at the plant that have flown but remain to be delivered. The balance of 34 flown/undelivered aircraft were assembled in Charleston, South Carolina where series production is now concentrated.

The flown/undelivered inventory includes 10 787-8s, 53 -9s and 19 -10s. No examples of the latter variant have been shipped since the original stoppage in October 2020.

Boeing stated earlier this year it intends to deliver in 2021 most of the undelivered 787 inventory that has accumulated over the last year or more. So it is crucial for Boeing to quickly work through the required data for the FAA to enable the suspension to be lifted once and for all.

June 15, 2021

By Max Kingsley-Jones, Senior Consultant at Ascend by Cirium

Four-fifths of idle unplaced lessor portfolios over eight years old

Analysis of the parked fleet highlights the most prolific types with no known future event.

Amid the gradual decline in stored airliners during recent months, the share of unplaced aircraft now accounts for a fifth of the operating lessors’ idle portfolios.

Data from Cirium shows that the number of stored passenger narrowbodies and widebodies has been steadily falling from 7,800 aircraft in Q1 2021, to around 6,300 at the beginning of June. Of these, just over half (3,220 aircraft) are managed by operating lessors.

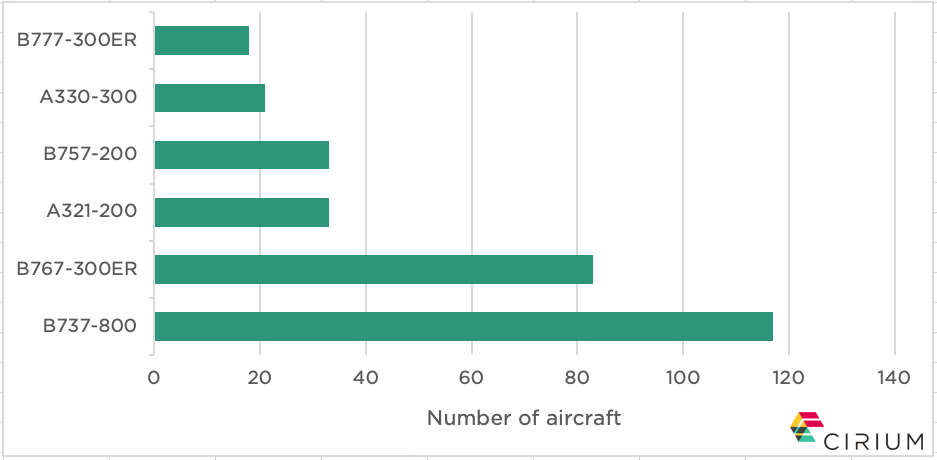

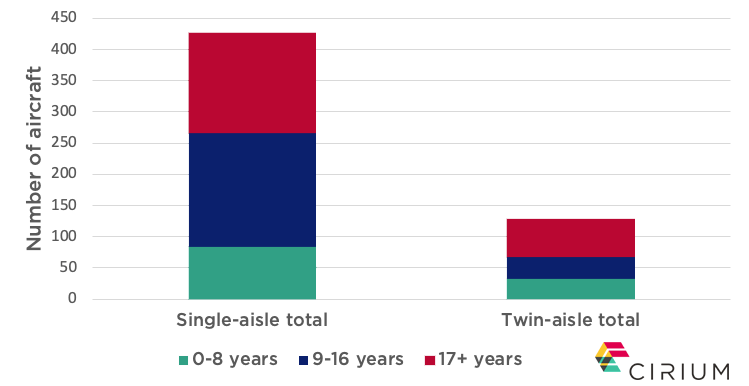

Analysis by Ascend by Cirium shows that over 550 mainline aircraft in lessor portfolios are currently idle and unplaced, with no known future lease, cargo conversion or retirement planned. Of these, around 80% (441 aircraft) are more than eight years old.

The growth in the number of lessors’ idle unplaced aircraft has slowed in recent months. But as airlines have returned aircraft to service, the share that unplaced aircraft represent of the lessors’ entire idle portfolios had risen to around 18% by June, according to Cirium data and analysis. The ratio is slightly higher for widebodies, at 19% (129 aircraft), compared with 17% (427 aircraft) for narrowbodies.

The A320ceo family is the most populous idle type in the lessors’ unplaced portfolio, with Ascend by Cirium analysis identifying 200 aircraft. The 737NG is ranked second, with 132 aircraft identified. A third of these A320ceo and 737NG aircraft are more than 16 years old.

Airbus also heads the rankings from a widebody perspective, with Ascend identifying 52 unplaced A330s (all Ceos). The majority of these (58%) are in the 9- to 16-year-old age range.

The 777-200/300 Classic has the second highest tally – 26 aircraft – with the 767 being ranked third (22 aircraft). All the 767s and all but two of the 777 Classics are over 16 years old.

With 40% (220 aircraft) of the lessors’ idle unplaced jets in the 17-years-plus age bracket, it will be interesting to see how many return as flyers in either passenger or freighter form, or are ultimately destined for part-out. And with the industry’s recovery playing out at different speeds geographically, the status of the lessors’ unplaced portfolios will remain dynamic in the near-term.

June 9, 2021

Boom – is it all just noise?

By Richard Evans, Senior Consultant at Ascend by Cirium

The big news item last week was the announcement that United Airlines had agreed to purchase 15 Boom Overture Supersonic Transport (SST) aircraft.

There are huge technical, financial, environmental and certification challenges for Boom, and it is an arguably strange decision from an airline that has recently made much of its environmental and sustainability targets.

The Overture has a limited range, quoted as 4,250nm. The definition is not exactly clear, but generally this would translate to a real-world capability to fly great circle routes of perhaps 3,750nm. Without making refuelling stops, this points to a core market of Europe to the East coast of North America. For United, this enables many routes from its Newark and Washington DC hubs to Western Europe, at least in theory.

The Cirium FM Traffic module records a total of 6.2 million business class passengers across the North Atlantic in calendar year 2019, at an average yield of $0.26/RPK. The average distance was 3,860nm, indicating that 50% would likely be on flights beyond the non-stop capability of Boom’s SST. United Airlines carried 850,000 business class passengers across the Atlantic at a very similar average range. If each Boom flight carried 60 United passengers, this equates to 13,000 flights, or 18 return flights per day.

Cirium Tracked Utilization shows the number of business class seats flown between Europe and North America in 2019. By this metric, British Airways led the way, with United the 2nd largest across the Atlantic, with 878,000 seats each way.

Thus, a simple top-down approach indicates a sizeable potential market, but it requires diversion of a substantial portion of business class seat capacity. How would United configure its twin-aisle jets? It still requires business cabins for longer flights. Would it have to operate a sub-fleet of 787s without business class?

The final huge unknown is operating cost relative to business class cabins of conventional aircraft. Fuel burn and maintenance per hour will likely be higher than for a 300-seat Boeing 787. The SST is twice as productive, but that speed itself is an issue. At Mach 1.7 the Overture cannot be scheduled for two round-trip transatlantic flights per day. Time zones mean a regular 7pm departure from New York would arrive at London at 4am. Thus the extremely high purchase price ($200 million?) will be spread over comparatively low monthly utilisation of perhaps 2,000-2,500 hours a year.

In summary, it seems extremely doubtful a new SST will enter service this decade. Instead the technological focus is likely to remain on reducing fuel burn and retaining the flexibility to deal with future business cycles and shifts in demand.

June 2, 2021

Airbus Production Rate Increases – a Strong Recovery on the Way?

By Rob Morris, Global Head of Consultancy at Ascend by Cirium

Late last week Airbus announced plans to increase monthly A320-family production rate to 64 by the second quarter of 2023. The OEM is presently building at Rate 40 and expects to increase to Rate 45 by the end of this year. Airbus is also reported to have asked suppliers to enable Rate 70 by early 2024 and also consider a scenario for Rate 75 by 2025. With these numbers it is possible that Airbus will deliver some 480-520 new A320-family aircraft annually through 2023, before increasing to some 800-850 in the 2024-2025 timeframe. Is the market ready for these aircraft and what is driving the potential increase?

To address the second question first, Airbus currently report a firm order backlog in excess of 5,600 aircraft for the A320-family. At today’s Rate that would equate to more than 12-years’ worth of production. Even allowing for some softness, it would take a huge number of cancellations to normalise the backlog closer to a 5-year level. Hence, contracted demand is a clear justification for increasing Rate.

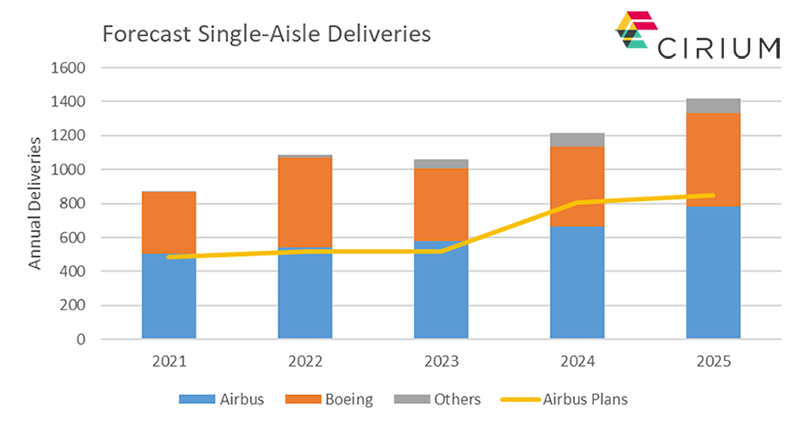

But will demand justify the increase? Our most recently published Cirium Fleet Forecast, completed in late 2020, uses our base-case demand-recovery scenario, together with productivity and retirement assumptions based upon detailed analysis of the current market, to estimate new single-aisle aircraft deliveries through 2025. Those forecast deliveries are illustrated below.

Over the next five years the forecast projects delivery of just over 3,000 Airbus single-aisle aircraft, albeit note that this does include around 400 A220s. Airbus’s own Rate projections drive an estimate of some 3,200 or so aircraft. So accounting for those A220s, the Airbus Rate projections are only some 20% above our own base case forecast. Given that the forecasts themselves are highly sensitive to the regional and global demand recovery projections, it could only require a marginally accelerated demand recovery, or perhaps fewer parked aircraft to return to service or a slower recovery of aircraft utilization, to build greater new aircraft demand than our base case projects.

At face value then, the Airbus Rate plans may appear optimistic. Perhaps Airbus is more motivated by its ability to raise the delivery market-share bar as its competitor remains in recovery mode from its single-aisle production crisis and evaluates rate increases of its own, rather than building to demand? But with so many variables at play right now it could only require some relatively small changes here and there for the demand to become a reality and the plan to be a demand lead and logical move.

May 25, 2021

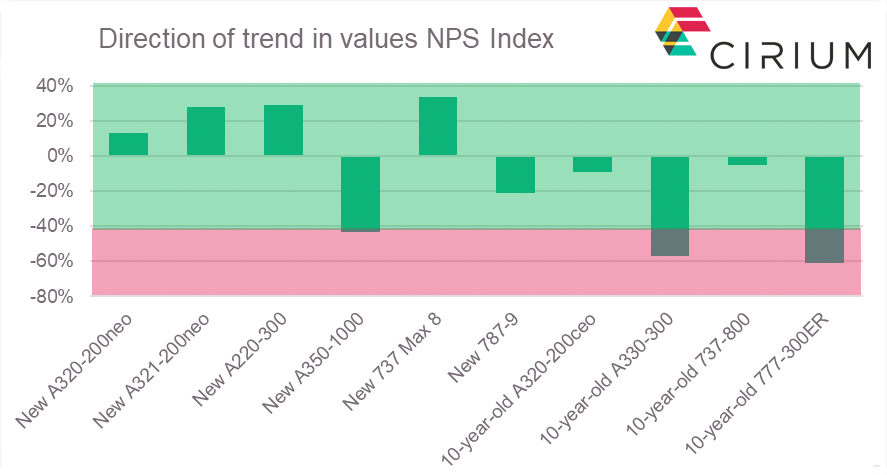

By David Griffin, Valuations Consultant, ISTAT appraiser at Ascend by Cirium

Commercial Aircraft Market Sentiment Index, May 2021

Following the successful launch of the Ascend by Cirium Market Sentiment Index in April, this month we focus on lease rates.

The number of participants increased slightly this month and if you would like to participate in future surveys, please contact one of our team.

As per last month, we continue to use an NPS Index for the lease trend – estimated as the number of respondents replying ‘trending up’ minus those replying ‘trending down’, divided by the total sample response. Scores in the 40% to -40% range broadly indicate stability, those below -40% can be considered to indicate a very strong negative trend in lease rates and those above 40% indicate a strong positive trend. Thus, it is clear from the analysis below that the market sees continued negative pressure on all widebody lease rates, but positive pressure on new technology single-aisle aircraft.

The same NPS logic for our Current Market Lease Rates indicates that we have one type where the survey suggests our CMLR is too high, eight where our opinion can be considered ‘about right’ and one where our opinion is ‘too low’.

Looking at the stability measure, the percentage considering the type ‘stable’ is shown above. As with the value stability index, new-generation types are considered to be the most stable (aside from the A350-1000) but what is most interesting is that participants see lease rates for a 10-year-old 737-800 being more stable than for a new 737 Max 8.

Contrasting the NPS Index for values and lease rates (from this and last month’s surveys) above we see remarkable similarity. However, on average there is slightly more optimism for lease rates rather than values.

Potentially, the slightly greater optimism for lease rates could be seen as a leading indicator. While we certainly are not calling the bottom for lease rates, and neither is the market, there is a modicum of hope for new technology narrow body aircraft.

Finally we surveyed participants on one of the most important elements of the supply side – stored aircraft. At the end of 2019, Cirium fleet data recorded 1,466 passenger single-aisle aircraft in storage. By the end of 2020, the parked inventory had increased to 5,156 single-aisle aircraft in storage. So we asked participants where they expect stored inventories to be at the end of 2021. The results appear quite bullish, with 77% voting for less than 4,000 single-aisle aircraft in storage at year end and a significant 34% voting for less than 3,000.

It will be interesting to see where this metric does land in December. Our own Ascend by Cirium recovery scenario 4, our current baseline, projects over 4,400 single-aisles will still be in storage at year end. If we are wrong and the 34% are right, then we will need to see almost 1,500 single-aisles either returned to service or parted-out in the next six months. That in turn will require a fundamental recovery in passenger demand which for now remains frustrated by continued travel restrictions. As the situation remains dynamic we continue to monitor and may revise our scenarios later in the year as more data becomes available.

Next month’s survey (which will return to the original aircraft values as we seek to build a trend data set) will be issued on 9 June and if you would like to participate please contact one of the team.

May 19, 2021

By Max Kingsley-Jones, Senior Consultant at Ascend by Cirium

787 passes 1,000 deliveries

Boeing has recently delivered the 1,000th 787, less than 10 years after the first aircraft was handed over. This makes it the fastest widebody production run to pass that significant milestone.

That Boeing seems to have underplayed the achievement probably speaks to the production woes the programme has been suffering since the final quarter of last year, which saw a four-month hiatus in deliveries. The quality problems, combined with a general slowdown in shipments last year amid the COVID-19 crisis, significantly affected 787 delivery numbers.

Indeed, 787 line-number 1000 – a 787-10 for Singapore Airlines (SIA) – flew over a year ago – on 3 April 2020 – and as these words were written was yet to be delivered to customer Singapore Airlines. This aircraft’s status is denoted with the titles “1000th 787”, and it is probably no coincidence that SIA also took the 1,000th 747, in 1993.

The 747 was the first widebody to pass 1,000 deliveries, reaching that marker after 25 years of production. Five widebody types can now boast four-digit production numbers, the others being the 767 (1,214 deliveries), A330 (1,514 deliveries), 747 (1,561 deliveries) and 777 (1,661 deliveries). The latter was the previous fastest widebody to 1,000 units, passing the 1k-mark after 18 years of production, in 2012.

Cirium data shows that the 1,000th 787 delivery was made on 21 April, a 787-9 to China Southern Airlines as B-20EH on lease from Air Lease.

The achievement comes as Boeing closes the line at Everett, Washington, and concentrates all final assembly at its Charleston, South Carolina plant which came online in the second year of production. Cirium data shows that to date, production has been split roughly 60/40 in favour of Everett. The final Washington deliveries are expected this year as Boeing clears the significant production backlog that has built up at both plants amid inspections to address a “skin-flatness” issue.

Of the 1,003 deliveries completed by the end of April, the -9 variant accounts for over half (565 shipments). It is also the most popular variant on backlog, representing two-thirds of the 486 unfilled orders. Boeing’s big task now is to clear the vast inventory of undelivered Dreamliners. Just 11 787s were handed over in the first four months of 2021, against a Cirium forecast of more than 80 for the full year. With some 79 aircraft recorded in Cirium’s fleet data in the production cycle – that is with a first-flight date recorded – the challenge is significant.

May 19, 2021

Price Reset?

By Rob Morris, Global Head of Consultancy at Ascend by Cirium

Cirium’s recently updated fleet data reveals that Avolon placed orders for 14 Airbus A320neo family aircraft on April 28, 2021. Perhaps not significant news in itself, until we delve deeper to discover that Avolon also cancelled orders for 16 A320neo aircraft on exactly the same date. This followed a similar pattern in March, when the lessor placed eight new A320neo orders while cancelling a similar number.

Why would an operating lessor want to cancel an order, only to immediately replace it with an identically sized new order (albeit with a slightly different variant mix)? A potential answer may lie in contract structures, and most specifically in the impact of escalation on likely delivery pricing.

Digging a little more into these specific cancellations reveals that Avolon placed the original orders in 2014. Clearly we are not privy to Avolon’s contract pricing, but for the purposes of this discussion let’s assume the order was made at our extant Market Value (which was $46.0 million). As is typical with aircraft purchase contracts, the delivery price would likely be subject to escalation based upon an agreed formula. Again, we are not privy to the specific formula but it will almost certainly be based upon industry standard labour and commodities indices. Researching these, we can estimate that escalation has been running around 2.0% per annum since 2014. Hence each A320neo ordered in 2014 at that $46.0 million value, would be delivering today for around $52.8 million.

That’s a difference of some $6.6 million between today’s value and the potential escalated price. Although we don’t know when these aircraft will ultimately be delivered, the escalation clock will actually increase that value delta with time (by 2025 it will be $7.2 million). Thus, it is clear that a pricing reset is required to correct price to something closer to Market Value. Hence this apparently odd move to cancel and re-order can be fully rationalised. Even if Avolon has had to forfeit its deposit on the original order, then the loss of a few hundred thousand dollars per aircraft seems palatable in the overall context of the price reset.

One final reason why this reset is required is the rent the aircraft can earn. Back in 2014 our extant Market Lease Rate (MLR) for a new A320neo was $400,000 per month. Today that same MLR is $310,000 per month. This is an almost 25% reduction in the earning potential for the aircraft, providing another clear reason why Avolon needs to see a price reset. Avolon is unlikely to be the only operating lessor facing this challenge in its new aircraft order backlog, so we might expect to see similar moves from others.

May 5, 2021

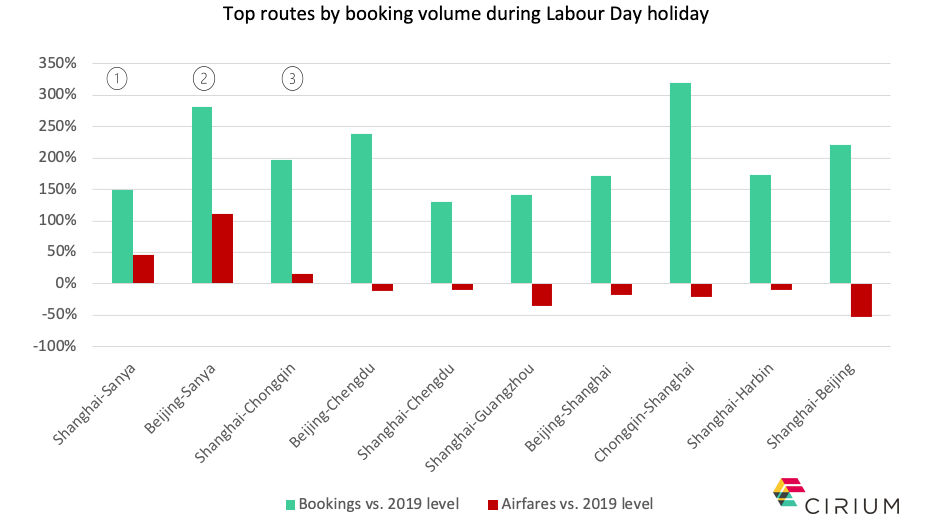

Hope and Fear: Observation on market and airline operation during 2021 Chinese Labour Day holiday

By Joanna Lu, Head of Consultancy Asia at Ascend by Cirium

This year’s Chinese Labour Day holiday is the first long break the country has seen in a largely COVID-19 free condition for a while. Therefore, it is expected to unleash a pent-up demand for travel after the partial lockdowns necessary through the Lunar New Year, due to multiple coronavirus outbreaks. Consequently, likely demand is estimated to amount to some 200-265 million journeys domestically via ground, rail and air during the five-day holiday, pretty much back to pre-COVID-19 levels.

Although a majority of trips will be via ground and rail transportation, air travel bookings surged significantly for flights between April 30 and May 6, 2021. Seat bookings were up 23% compared with the same period in 2019, according to estimates from Trip.com. Economy-class airfares for trips over the Labour Day holiday have risen 11% compared with 2019 levels. This compares with the average 23% drop versus 2019 levels in Economy-class airfares, observed during the last six months.

At the specific route level, the top routes by booking volume suggest demand for air travel is largely arising from high per capita income cities including Shanghai, Beijing and Chongqin. Bookings on these top routes increased between 100% and 300% compared to the same period in 2019.

However, air fares on these routes are still generally lower compared to 2019 level, except for the top three ranked city pairs (Shanghai-Sanya, Beijing-Sanya and Shanghai-Chongqin). Interestingly the city pairs of top searching and top booking are somewhat different, which indicates a new travel booking pattern, with passengers now booking flights on a much shorter time horizon and with a more flexible itinerary choice. This leaves airlines with a significant capacity planning challenge, as they seek to match their supply to volatile demand.

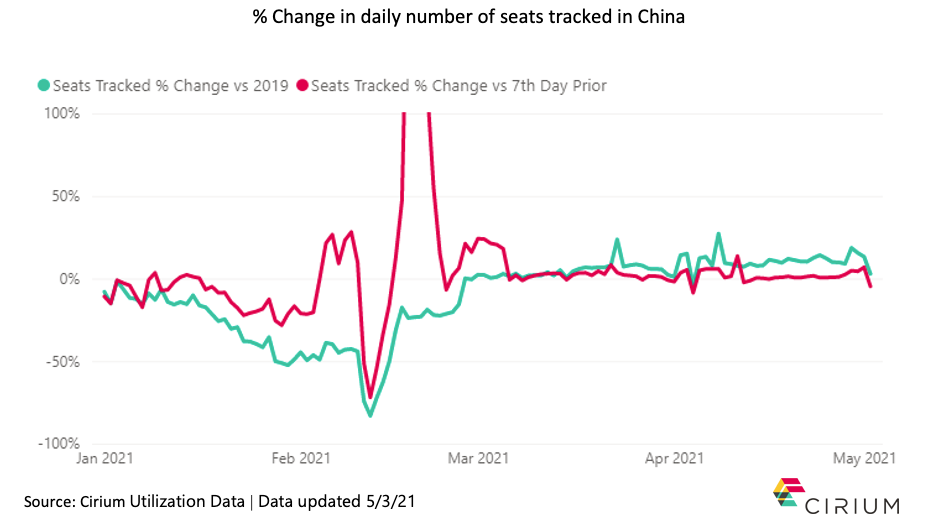

From an operational perspective, Cirium’s data shows 3,165 aircraft tracked in China on May 1 (the day of peak of demand during 2021 Chinese Labour Day holiday), compared to 2,939 in 2019, thus representing 7.7% growth.

Tracked flights and tracked seats has grown at a higher rate, at 11.7% and 13.2% respectively, Each of these metrics is also 5.4% and 6.8% higher compared to the previous week.

This indicates that Chinese airlines are using larger aircraft and flying more flights over the holiday period in response to the increase passenger demand.

Indeed, our data shows that on May 1, 2021 there were 14.4% more twin-aisle aircraft tracked compared to the previous week and 2.3% more single-aisle aircraft. There were also 23.6% more flights operated by twin-aisle aircraft and 4.1% more flights run by single-aisle aircraft.

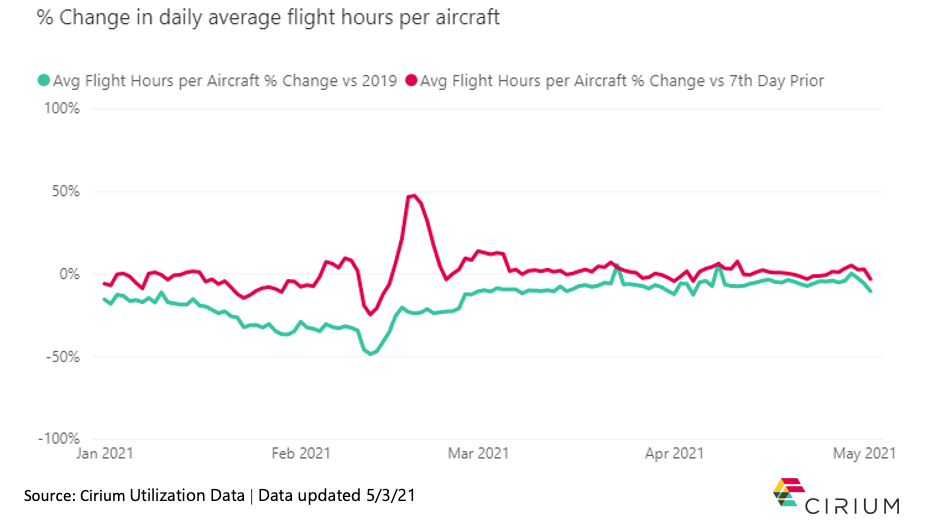

While it is plausable that more aircraft are in service during the holiday period compared to 2019, the average daily flight hours per aircraft was only 8.4, some which was 6.0% down compared to 2019 (8.9 hours). The global coronavirus situation remains serious and Chinese airlines’ international passenger traffic still remains negligible, while border restrictions and quarantine rules remain in place. So for airlines a key challenge will be keeping aircraft utilization high once the peak holiday season ends.

May 4, 2021

First reports from Ascend by Cirium Market Sentiment Index

Ascend by Cirium recently launched our Commercial Aircraft Market Sentiment Index. The Index will be published monthly and will track market sentiment on values, lease rates and trends through a survey of key market stakeholders, including lessors, banks, OEMs, part-out shops, airlines and brokers. The first issue of the survey closed on 26 April and from our initial target of 100 participants we were delighted to receive almost 60% participation.

We are keen to broaden our sample base further so if you would like to participate in future surveys, which we envisage will run on a monthly basis and will ask three simple questions connected with commercial aircraft values and lease rates, please contact one of our team. Meantime, we are pleased to report the outcome of the inaugural survey.

This month we asked participants their perception of our Current Market Values (CMV) and the trend in values for ten key aircraft types. Our simple NPS Index for the value trend – estimated as the respondents replying trending up minus those replying trending down, divided by the total sample response – is illustrated below. Scores in the 40% to -40% range broadly indicates stability, whilst those below -40% indicate a strong majority towards continued decline in value trends.

Thus, it is clear that the market sees continued negative value pressure on most widebody values and used narrowbodies, but stability in newer narrowbodies.

The same NPS logic for our actual values suggests that we have one type where the survey suggests our CMV is too high, eight where our opinion is ‘about right’ and one where our opinion is too low. We will use this detail to further direct our research efforts as we strive to ensure our values are the most appropriately calibrated available in the market today.

Our final question will always be a little more general and this time we asked that frequent question; when respondents think global passenger traffic will return to 2019 levels. The results appear quite bullish, with 47% voting for 2023 and a lower 32% for 2024. Our own Ascend by Cirium scenarios project August 2024 in the baseline and May 2023 in the upside, so the market seems to be in line with our own thinking, which was defined in September 2020 but which seems to be tracking well to reported traffic volumes. IATA’s most recent scenarios seem to be projecting early 2024. Clearly time will tell, but the majority certainly believe that by 2024 we will be well on track to recovery.

Next month we will survey on Current Market Lease Rates and trends. If you would like to participate in next month and subsequent surveys, please contact one of our team.

April 27, 2021

A look at how the latest 737 MAX grounding has halted delivery momentum

By Max Kingsley-Jones, Senior Consultant at Ascend by Cirium

The discovery of an electrical issue in early April that grounded over 100 Boeing 737 MAX aircraft has also brought deliveries to a grinding halt just five months after shipments resumed.

Boeing had been delivering aircraft from the stockpile of around 450 aircraft it has accumulated since March 2019, and directly from the assembly line in Renton, Washington. Between December 2020 when deliveries had resumed, and early April when the grounding was ordered, Boeing completed 89 Max deliveries – an average of around 21 a month.

Boeing halted Max deliveries on 7 April after just four aircraft had been delivered since the start of the month, as details emerged of the electrical grounding and bonding issue. This resulted from a design change that was introduced on the Max shortly before the March 2019 fleet grounding, and will be subject to a Federal Aviation Administration airworthiness directive.

One of the conditions stipulated following the November 2020 ungrounding was that each MAX delivery must be overseen by an FAA inspector. This factor may have contributed to Boeing’s delivery rate being tempered: In the four months since deliveries resumed, Boeing generally achieved a maximum of two per day (with three achieved occasionally). So far in 2021, Boeing has delivered 62 of the approximately 360 MAX aircraft Ascend by Cirium estimated Boeing would ship this year, prior to the latest grounding.

The FAA has disclosed that the electrical issue affects 737 Max 8/9s built between early 2019 and April 2021 with line numbers between 7399 and 8082. Boeing says that 106 delivered Max aircraft are affected (including 18 delivered prior to the 2019 grounding). But the line-number range indicates over 600 aircraft are potentially affected (the 737 Max shares its line number sequence with the 737NG, and Cirium Fleets Analyzer shows at least 50 line numbers in the sequence are commercial or military NGs).

Ryanair has been an immediate casualty of the new grounding, as it was poised to finally take delivery of its first MAX 8-200s two years after they were first due. The airline’s chief Michael O’Leary said last month that he expected deliveries would begin in April, with 16 aircraft arriving by the end of May – but none have yet left Boeing.

All MAX shipments are in limbo as Boeing and the FAA work to authorize and mandate a remedy. Once the modification is defined, airlines have indicated that they hope and expect repair work can be completed “in a matter of weeks”.

Connect with Ascend by Cirium.

April 21, 2021

By Chris Wills, Head of consultancy operations, senior ISTAT appraiser at Ascend by Cirium

Airline leasing versus owned aircraft trends

Following recent airline comments in the market regarding owning versus leasing aircraft, coupled with the single and twin aisle passenger jet fleets finally exceeding 50% market share, it is worth a quick look at the debate in more detail.

While there was a divergence in thoughts over leased versus owned fleets, one common area agreed upon was that Sale and Lease Back of new aircraft is worthwhile for all parties with airlines immediately benefitting from the capital inflow such deals facilitate. The data supports this. Cirium Fleets Analyzer shows that 66% of single and twin aisle commercial jets less than 3 years old are on operating leases.

The question of owning or leasing is of course specific to each operator, but a look at the age profile indicates the trend.

The case for leasing is skewed to newer assets, where capital cost and the associated risk is of greatest importance.

Chris Wills, Head of consultancy operations, senior ISTAT appraiser at Ascend by Cirium

Cirium Fleets Analyzer highlights this: of the fleet 0-9 years in age on average 58% is operating leased, 10-19 years 48%, while 20-29 years just 24% of the fleet is on operating lease. Looking at the 0-20 age fleet (88% of the total) 54% is on operating lease.

There are a number of examples of airlines operating a model with preference for ownership of older aircraft. Offsetting capital or leasing costs dramatically changes the equation and focus shifts to variable operating costs (including fuel burn) and reliability, both of which can be managed with the right business competencies.

With the current market conditions airlines with a focus on older aircraft and a relatively stable financial position can take advantage of the buyers’ market for aircraft, particular unencumbered aircraft or those approaching end of lease. In some cases, values are already around part out. While clearly there is a massive need for lessors that is set to grow, perhaps we could see a larger shift of the fleet to airline owned for mid-life assets, considering the numbers involved (over 7,600 aircraft 10-20 years old) it could account for a lot of individual assets.

Connect with Ascend by Cirium.

April 14, 2021

The Implications of Airline Reorganizations for Operating Lessors

By Rob Morris, Global Head of Consultancy at Ascend by Cirium

The recent news that LATAM is rejecting seven Airbus A350s it leases from AerCap, as part of its US Chapter 11 restructuring, is a potential blow to the lessor and amply illustrates the risk that bankruptcy reorganizations pose to operating lessors.

These specific A350s were all acquired by AerCap from LATAM via purchase and leaseback on delivery from Airbus, between September 2016 and December 2019. The Cirium Core fleets data indicates that the leases were typically scheduled for a 12-year term. Although we are not party to any details of the specific leases, if these aircraft entered those leases at our extant Current Market Lease Rates, then the rents would have been between $1.07 million and $1.1 million per month. We thus estimate that at the start of 2020 AerCap would expect to be collecting just over $7.6 million per month from LATAM for these aircraft.

If the documents submitted to the bankruptcy court are correct then these aircraft will be returned to the lessor in three batches between this month and early June 2021. At that point the lessor will lose the $7.6 million rent – we have no indication of receivables since the onset of COVID-19 so this may already have been the case anyway – and be faced with the significant challenge of placing these seven A350s in a very difficult marketing environment. Even if they are able to place these aircraft relatively quickly at our Current Market Lease Rates, which now stand between $580,000 and $700,000 per month, then the aggregate rents will be some 40% lower per month at around $4.6 million.

In the context of AerCap’s average monthly basic lease rents collected for FY2020 – reported at around $314 million in their Q4 2020 earnings release – the monthly delta of $3 million may not seem significant. But the net cash income loss over the contemplated life of the lease is potentially significant. Based on the rents discussed above they would indeed likely exceed $300 million over the life of the originally contemplated 12-year leases.

AerCap are surely not alone in this predicament. Most operating lessors are likely to be facing similar challenges with other airlines and aircraft types on a weekly basis at present. Whilst there are signs of optimism in demand recovery, it seems likely that lessors will be bearing the cost of airline reorganizations for some time to come.

April 7, 2021

2021 – End of the road for a number of business aircraft types

By Daniel Hall, Senior valuations consultant, ISTAT appraiser, ASA senior appraiser, Ascend by Cirium

In a market downturn, product streamlining is commonplace, as is announcing new models or upgrades as the market starts to rebound. The below commentary discusses three different types which saw production announcements in Q1 2021. All of these models were built in the same location – Wichita, Kansas.

Bombardier will end production of the iconic Learjet; over 3,000 have been built since 1964 and more than 2,000 remain in service today. Annual deliveries had been below 20 for some time, and the Learjet is now a casualty as the manufacturer further streamlines itself for efficiency. During the pandemic Lear 45 and 60 values have actually performed quite well but the Lear 70/75 has continued to rapidly depreciate.

Textron’s Beechcraft announced the end of the King Air C90GTx. The clue was with announcements of new KA 260 & 360 (replacing 250 & 350i). Since the early 1960s almost 3,000 of over 25 variants of the KA90 have been built with around 2,200 in service today. Deliveries numbered around 50 annually pre-2008, but have been sub-15 annually for six years now. The KA90 has actually exhibited really strong value retention and we expect the future outlook to remain bright.

The OEM’s Cessna brand announced the end of the Citation Sovereign+. This had been expected following full certification of the Latitude and Longitude. Those aircraft were clean sheets with superior cabins, and while the Sovereign could compete on a midsize segment price among other aircraft which didn’t offer a true transcontinental range, Embraer’s Praetor 500 has commenced deliveries and offers that. Historically competing with the Hawker 125 / 800 series, 450 were delivered since 2004. More recently, new deliveries had fallen to below 10 per year.

Although the pandemic has forced the cessation of these aircraft types, OEM product support is expected to continue, which will sustain the products’ life and value cycles.

MARCH 31, 2021

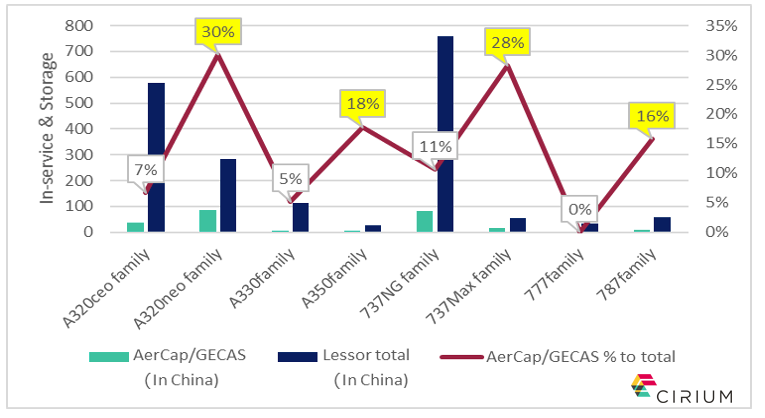

A look at the fleet of the world’s new “largest” lessor in China, and its implication for Chinese lessors

By Yuanfei Zhao (Scott), Aviation Analyst at Ascend by Cirium

In recent years, there have been voices in the industry talking about the shift of market power between domestic Chinese lessors and foreign lessors, both of whom compete in the relatively large Chinese leasing market. While the Chinese owned lessors clearly manage the majority of the leased fleet in the domestic market today, some qualitative elements should also be considered when making such a comparison.

The portfolio composition of the world’s new “largest” lessor (the planned AerCap/GECAS merged entity) shows that the proportion of each of the most popular single-aisle and twin-aisle passenger jets managed by the largest lessor against the total lessor managed fleet in China.

While there are currently close to 70 domestic and foreign lessors actively managing fleet in China, it is noteworthy that the proportion of new generation narrow-body and wide-body fleet managed just by the AerCap/GECAS combination in the Chinese market is so high.

This reflects the fact that the world’s leading lessor is weighting more strategic focus on the high-end market in the world’s fastest growing aviation market. This strategy leverages its buying power and favourable slot positions at the OEMs. On the other hand, this also reflects the forward-looking nature of the top tier lessors who tend to plan and invest in premium assets.

The implication here for those Chinese lessors who do not yet have any orders for new aircraft types is that the current downturn provides the opportunity for them to proactively seek purchase and leaseback deals with airlines for new types, or seek to work with OEMs to provide finance for new deliveries where the existing financier has fallen away. Once the market has fully recovered and once again returned to long-term growth in the latter part of this decade, the barriers for acquiring new types could be even higher, so now is the time for action.

MARCH 23, 2021

It’s the hour for by-the-hour

By Thomas Kaplan, Valuations Consultant at Ascend by Cirium

US Bankruptcy courts have been busy this week as we learned of court approvals for amended lease agreements between BBAM & Aeromexico and GECAS & Avianca. These lease agreements are to be based on “by-the-hour” (PBH) payments, rather than a fixed monthly lease rate. PBH agreements have become very common now for new leases, lease extensions and lease restructurings, but what does it mean for lessor revenue?

The Aeromexico restructured lease was for 13 year old 737-800 MSN 34954 which has not flown since last April, per Cirum Tracked Utilization data. It is not known if there is a minimum monthly payment due, but if the utilization stays this low, the lessor won’t be getting much revenue and far below our Market Lease Rate (MLR) opinion of $138k. Prior to Covid, the aircraft was flying over 300 hours per month which, in the unlikely event that utilization returns to those levels soon, the PBH could be more profitable than a 138k lease rate.

The Avianca leases are for 2010-build A320s, MSNs 4487 and 4599. While these sat idle for most of the time since March 2020, they started seeing utilization in October last year and in February 2021 MSN 4487 even notched over 100 hours. Our MLR for these is $140k per month, so even if we assume a high PBH rate of $1,000/Flight Hour, lessors revenue would still be ~30% below the fixed rate.

Why are lessors agreeing to PBH if it means a large cut in revenue? The difficult remarketing environment means that lessors have few alternatives in the short term. Should they take out their aircraft from the defaulting airline, where and when would they place it? And what costs would they have to incur in terms of storage, insurance, reconfiguration etc? And how much would they forego in terms of end of lease compensation with the original lessee? So long as demand for new leases remains low we’d expect these PBH type deals to continue.

MARCH 18, 2021

Scaling the wall of cash

By Michael Graham, Valuations Manager at Ascend by Cirium

Pandemic? What pandemic? Since the start of 2021, one could be forgiven for thinking that international bond markets have been completely ignoring the tumult caused by COVID-19, such is their desire to invest in commercial aviation. For example, at the end of February, EasyJet successfully raised €1.2billion worth of seven-year bonds at a yield of just 1.875% in an offer that was significantly oversubscribed, with almost €6bn worth of demand. In January, Castlelake enjoyed even healthier demand for its $595million CLAS 2021-1 ABS offering, which was up to 12.3 times oversubscribed. In January alone, lessors raised a combined sum of almost $15billion either through bond issuances or ABSs.

While this can be seen a vote of confidence in the sector, the sheer demand exhibited by the market also testifies to the significant ‘wall of cash’ currently chasing after a limited number of suitable opportunities.

As yields on government bonds fell to virtually zero in 2020, many investors have found themselves moving towards comparatively riskier corporate issuances to generate income. It is perhaps unsurprising therefore that airlines, lessors and OEMs have taken advantage of this recent market appetite, in order to bolster cash reserves and refinance existing debt, lest the recovery in passenger numbers become more protracted than anticipated, or if bond investors become more nervous.

Indeed, in the past couple of weeks, there have been signs of turbulence within fixed income markets, with US 10 Year Treasury Yields rising to their highest level since January 2020, thanks to a hawkish US Federal Reserve, as well as the US Government’s $1.9 trillion stimulus plan, the by-product of which could be higher inflation. If central banks were to respond by raising interest rates, this would push up the cost of capital for all sectors, including aviation. A further sign, if one were needed, that the recovery from COVID-19 could be far from smooth.

Connect with Ascend by Cirium.

MARCH 10, 2021

Will Boeing 737-800 Values Have to Reduce Further?

by Rob Morris, Global Head of Consultancy at Ascend by Cirium